NATGAS: Atlantic LNG Could See Quarter of Production Offline for Month

Atlantic LNG in Trinidad and Tobago shut Train 3 today Feb. 13 after a crack in its flaring system w...

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

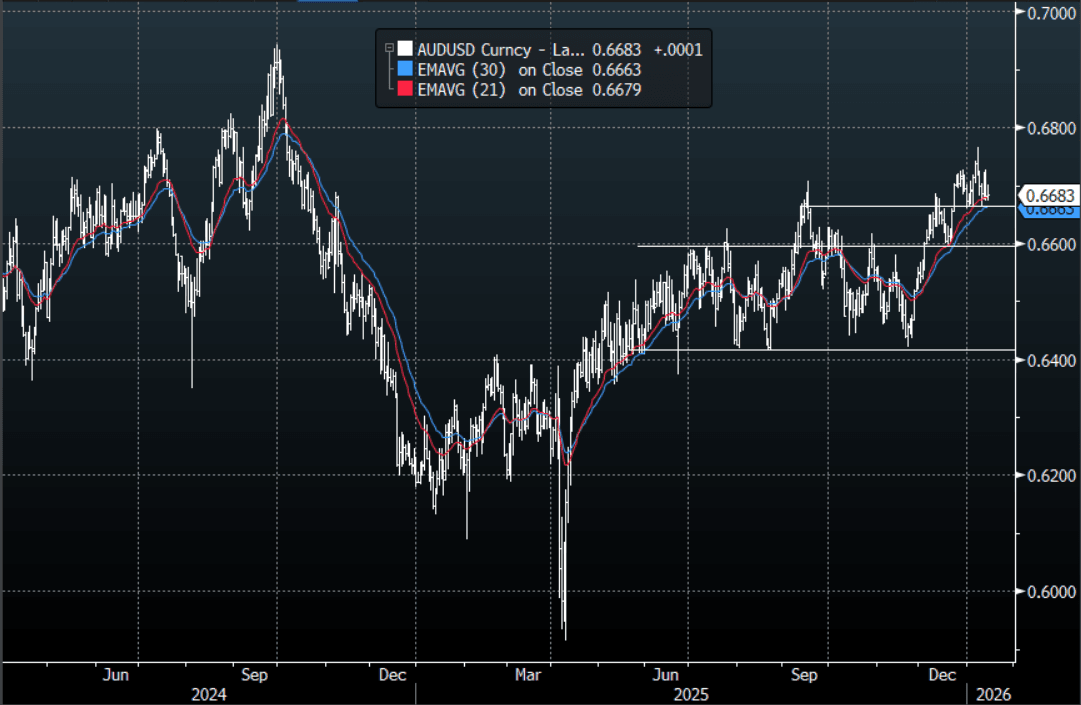

AUD: AUD/USD - Struggles To Reclaim 0.6700

The AUD/USD had a range overnight of 0.6673-0.6702, Asia is trading around {AUDUSD Curncy}. The AUD could not get back above 0.6700 and is treading water for the moment, stocks have ended down, but metals continue their meteoric rise. The Supreme court did not rule on the tariffs, pushing the potential decision out at least to next week. The AUD price action has been constructive but its failure to extend higher would be a little concerning. Technically while the AUD remains above 0.6600 dips should continue to find support. In the Asian session, the risk is for another test of the 0.6650 area which has been so supportive in recent weeks. In the short-term watch for sellers back toward the 0.6700-0.6720 area looking for a retest of the 0.6650 support, should this break we could see a deeper pullback as the AUD could play catch up.

- Bloomberg - “(Bloomberg) -- US Treasury Secretary Scott Bessent lauded Australia’s “commitment to a strong, action-oriented partnership to create long-term secure critical minerals supply chains” during a meeting with Australia’s Treasurer Jim Chalmers.”

- Options : Closest significant option expiries for NY cut, based on DTCC data: none. Upcoming Close Strikes : 0.6600(AUD1.98b Jan16), 0.6640(AUD1.24b Jan16), 0.6800(AUD2.51b Jan16) - BBG

- The AUD/USD Average True Range for the last 10 Trading days: 41 Points

- Data/Event: Consumer Inflation Expectation

Fig 1: AUD/USD spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

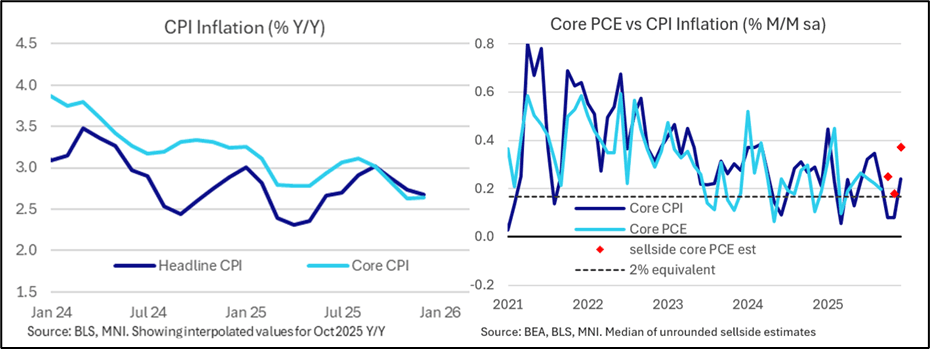

US INFLATION: MNI US Inflation Insight: Almost Normal

We've just published our latest US Inflation Insight - Download Full Report Here

- December’s CPI data was softer than expected in most respects, with relatively limited “payback” from the unusually soft (and heavily distorted) October/November report.

- Stronger-than-expected food prices and energy readings kept headline (0.31% M/M) from "missing" more vs MNI's unrounded consensus (0.37% M/M) than did core which came in at 0.24% M/M (0.35% unrounded consensus).

- Headline Y/Y inflation printed its lowest since June and core CPI Y/Y inflation at joint lows since early 2021. There was relatively little change in Y/Ys for core goods and services compared to last month's surprisingly low November print, though food inflation firmed.

- Within the core categories, the big surprise was that there was zero inflation in core goods prices despite anticipation that there would be "payback" in particular for unusually low holiday sales-related goods prices in November (along with continued expectations of tariff passthrough).

- Core services and overall supercore were also on the soft side though directionally most of the major categories were in order. That included a pickup in housing inflation that was slightly more than had been expected, and while travel-related services jumped as fully anticipated, they wasn't quite as strong as consensus had thought.

- Subsequently-released (and delayed) producer price data for October and November pushed up core PCE forecasts for Q4 – and there will be a positive spread for core PCE over its CPI counterpart - but the FOMC’s December projection of 3.0% Y/Y still looks to have downside risks.

- There were plenty of oddities in this CPI report, with several categories registering multi-year/all-time highs and others lows without much explanation, reinforcing the notion that the “noise” from the October/November collection period continues to reverberate.

- By the same token, it will reinforce conviction among FOMC participants that it could be a little longer before there is a cleaner read on underlying inflation dynamics.

- Overall while inflation may not have picked up as strongly toward the end of the year as feared following the imposition of tariffs, Fed officials have signalled that they will be waiting to see data early in the New Year for any signs that businesses are finally setting prices higher to offset input inflation pressure. But most are cautiously optimistic that inflation should come down over the course of the year.

- In the meantime, the data did nothing to alter expectations for a January Fed hold, with more focus at this point on the labor market. FOMC meeting-dated OIS shows just under 1bp of easing for this month, 6.5bp through March, 11bp through April, 24bp through June, 32bp through July and 53bp through year-end.

AUDUSD TECHS: Monitoring Support

- RES 4: 0.6872 38.2% retracement of the 2021 - 2025 L/T downtrend

- RES 3: 0.6858 1.000 proj of the Nov 21 - Dec 10 - 18 price swing

- RES 2: 0.6795 0.764 proj of the Nov 21 - Dec 10 - 18 price swing

- RES 1: 0.6767 High Jan 7 and the bull trigger

- PRICE: 0.6683 @ 16:16 GMT Jan 14

- SUP 1: 0.6664 Low Jan 9

- SUP 2: 0.6632 50-day EMA

- SUP 3: 0.6593 Low Dec 18

- SUP 4: 0.6553 Low Dec 3

Recent weakness in AUDUSD still appears corrective and has allowed an overbought condition to unwind. Initial firm support around the 20-day EMA, at 0.6681, has been pierced. A clear break of it would expose support at the 50-day EMA, at 0.6632. The area between the two EMAs still represents a key support zone. For bulls, a resumption of the uptrend would open 0.6795 next, a Fibonacci projection.