MNI MARKETS ANALYSIS: VAT Plans Raise Focus on Japanese Fiscal

Feb-13 17:39By: Moritz Arold and 1 more...

Japan+ 2

DOWNLOAD FULL PDF REPORT HERE

Executive Summary:

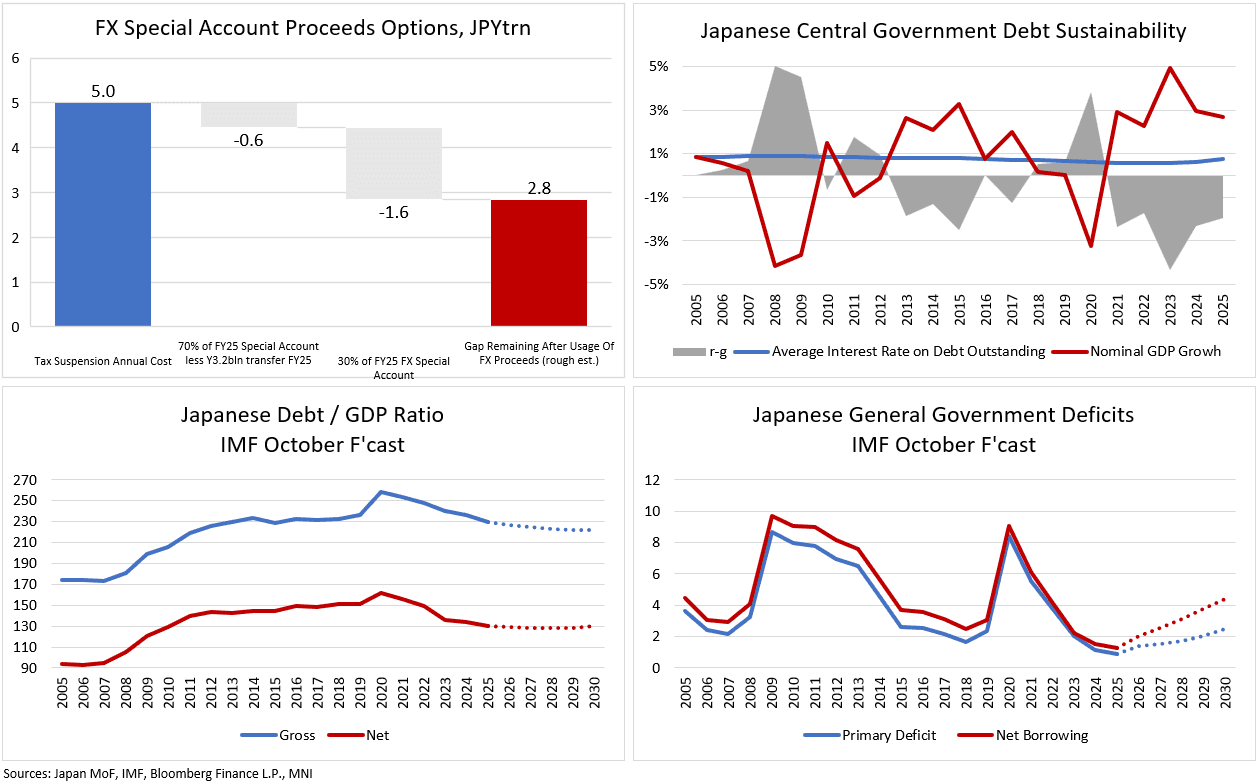

- Financing the JPY5trn food consumption tax suspension with proceeds from the FX special account would likely open up gaps in the general budget

- This leaves the Japanese finance ministry with three options: Plug the gap through increasing the efficiency of the tax base and expenditure, net liquidation of parts of the FX special account, or higher JGB issuance through the backdoor

- Which one of these options it chooses may have substantial consequences for JPY as well as JGB yields. Special account partial liquidation would be a notable JPY positive

- If Japan wants to adhere to its new fiscal rules, its headroom has an upper limit of roughly 8ppts of GDP through 2030 cumulatively