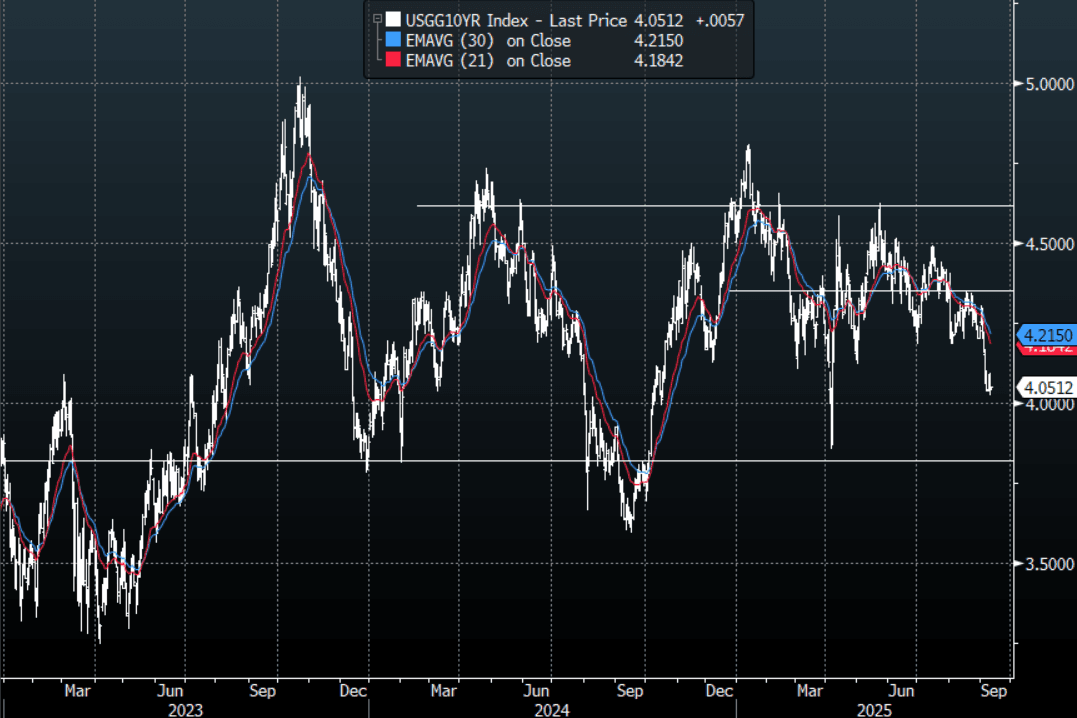

US TSYS: Asia Wrap - Quiet Session Ahead Of US CPI

The TYZ5 range has been 113-13+ to 113-15+ during the Asia-Pacific session. It last changed hands at 113-14, down 0-04+ from the previous close.

- The US 2-year yield is trading around 3.542%.

- The US 10-year yield has edged higher trading around 4.052%, up 0.01 from its close.

- 10-Year Yields should continue to see demand on bounces now as the market reacts to a labour market that is rapidly cooling. The first buy-zone is now back towards 4.20%, having basically reached the first target towards the 4.00% zone, the CPI tonight will determine if the market begins to look towards the 3.80% area.

- MNI US PREVIEW: August CPI: Risks Seen Skewed To Core Tickup To 0.4% M/M. Despite coming in softer than expected on the headline reading, the PPI release doesn't appear to have a significant impact on expectations for Thursday's CPI (0830ET).

- Consensus (Bloomberg median) is for core CPI to come in at 0.3% M/M rounded in August, same as July (0.32% unrounded). Unrounded core CPI expectations suggest a slight skew toward risks of a rounded-up 0.4%, with an unrounded MNI median of 0.32% and range of estimates of 0.29% to 0.36%. That would be steady from 0.32% in July for the joint-highest M/M since January.

- (Bloomberg) -- Bond traders are girding for a high-stakes US inflation report that has the potential to dent their wagers on a deep series of Federal Reserve interest-rate cuts starting this month and extending into 2026.

- Data/Events: CPI, Initial Jobless Claims, Household Change in Net Worth, Federal Budget Balance

Fig 1: 10-Year US Yield Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

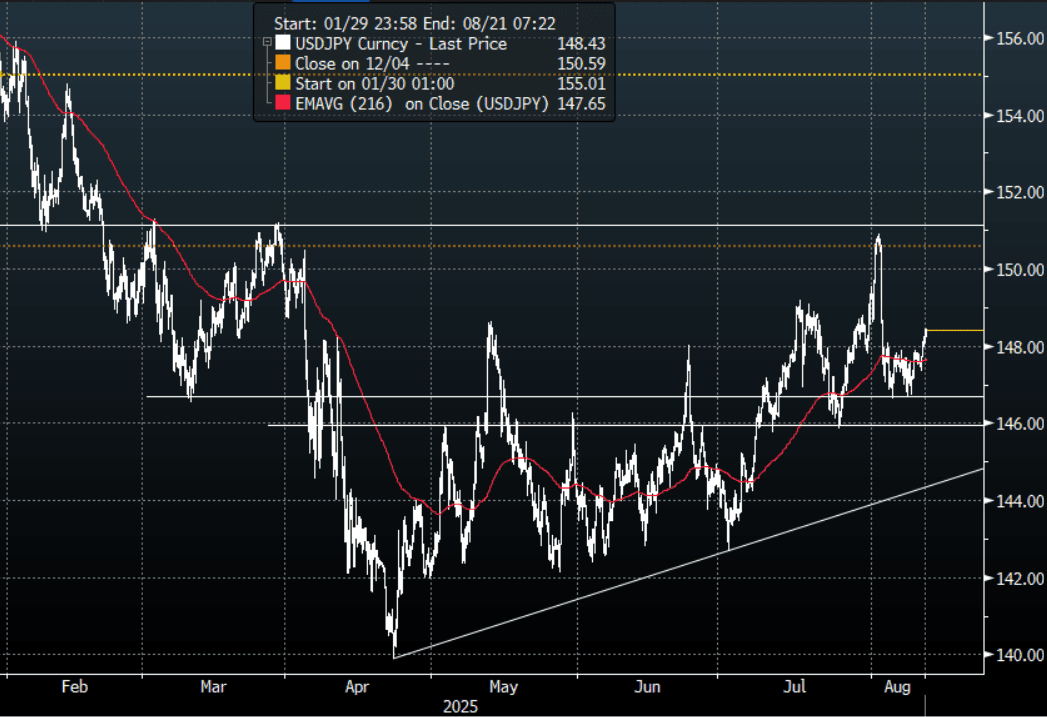

JPY: Asia Wrap - USD/JPY Probes Above 148 As Shorts Pared Back Into US CPI

The Asia-Pac USD/JPY range has been 148.05 - 148.45, Asia is currently trading around 148.45, +0.19%. USD/JPY is probing above 148.00 as the market pares back on some USD’s shorts going into the US CPI tonight. Price is holding above the support area between 146.00/147.00, a move sub 145.00 is needed to turn momentum lower once more, until then the 145.00-151-00 range should dominate. US CPI tonight will determine which end of the range is tested.

- MNI US CPI Preview: High Early Bar To September Fed Hold. The CPI report for July is released on Tuesday Aug 12, at 0830ET. Consensus sees core CPI inflation at a seasonally adjusted 0.3% M/M in June and unrounded analyst estimates broadly echo this with a median 0.32% M/M. It would mark a further acceleration from 0.23% M/M in June and 0.13% M/M in May for its fastest pace since January, with the latest firming seen coming from core goods inflation doubling to 0.4% M/M.

- (Bloomberg) -- Bond investors betting on a Federal Reserve interest rate cut next month face a potential roadblock: inflation. July’s consumer price index, due on Tuesday, will give traders clues on how President Donald Trump’s tariffs are affecting costs. Economists surveyed by Bloomberg expect the annual core inflation rate to rise to 3%, the highest since February.

- Options : Close significant option expiries for NY cut, based on DTCC data: 147.30($878m), 146.00($597m).Upcoming Close Strikes : 147.00($1.01b Aug 13), 150.25($1.47b Aug 13) - BBG.

- CFTC data shows asset managers reduced their JPY longs +60532( Last +75119), leveraged funds slightly reduced their newly built short JPY position -29308(Last -31280).

Fig 1 : USD/JPY Spot H2 Chart

Source: MNI - Market News/Bloomberg Finance L.P

OIL: Crude Range Trading Ahead Of Key Events Later Tuesday

Oil prices are slightly higher today ahead of US July CPI data, industry-reported US inventories, and EIA and OPEC monthly reports out later. Moves so far this week signal some stabilisation as the market watches the outcomes of the week’s events, which also include Friday’s Trump-Putin meeting on Ukraine.

- WTI is up 0.3% to $64.17/bbl after rising to $64.22 and then falling to $63.90 – a narrow range. Brent is also 0.3% higher at $66.83/bbl and has traded between $66.92 and $66.60.

- Trump said that Friday is more of a “feel-out meeting” and that he will report back to Ukrainian/European leaders afterwards. So it remains some time before the easing of sanctions on Russia can be considered.

- The 90-day extension of the current US-China trade stance to November 9 has calmed markets concerned that an escalation in trade tensions would weigh on growth and especially energy demand.

- US July CPI data are forecast to show both core and headline ticking up 0.1pp to 3.0% and 2.8% respectively (see MNI US CPI Preview) and will be monitored for signs of any tariff impact. A higher-than-expected print could pressure oil as demand concerns would increase. The market has around an 85% chance of a rate cut for the Fed’s September meeting.

- July US NFIB small business optimism, real earnings and budget data are also released, as well as UK labour data and euro area/German August ZEW sentiment. The Fed’s Barkin and Schmid speak on the economy.

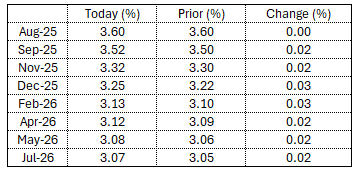

STIR: RBA Dated OIS Slightly Firmer Ahead Of Today’s RBA Decision

At the time of writing, RBA-dated OIS pricing is slightly firmer on the day across meetings ahead of today’s RBA Policy Decision.

- A 25bp rate cut this week is given a 96% probability, with a cumulative 59bps of easing priced by year-end (based on an effective cash rate of 3.84%).

Figure 1: RBA-Dated OIS – Current Vs. Yesterday

Source: Bloomberg Finance LP / MNI