FOREX: Asia-Pac FX: USD Retraces ADP Losses

The BBDXY has had a range today of 1217.77 - 1219.65 in the Asia-Pac session; it is currently trading around 1219, +0.15%.The USD has retraced most of its move lower from overnight in reaction to a weaker ADP print. I am caught a little undecided on the USD at the moment, I liked the fade into 1230 initially but short term I expect dips back toward 1210-1215 to now be supported first up. We could chop around sideways for a while while the market decides which way to go. Above 1230 and we could start to break higher, below 1205 and the downtrends momentum could be re-engaged. Short-term while the 12221/22 area caps price my bias would be for a test toward the 1210-1215 support, above there and the market will look back toward the 1230 area once again.

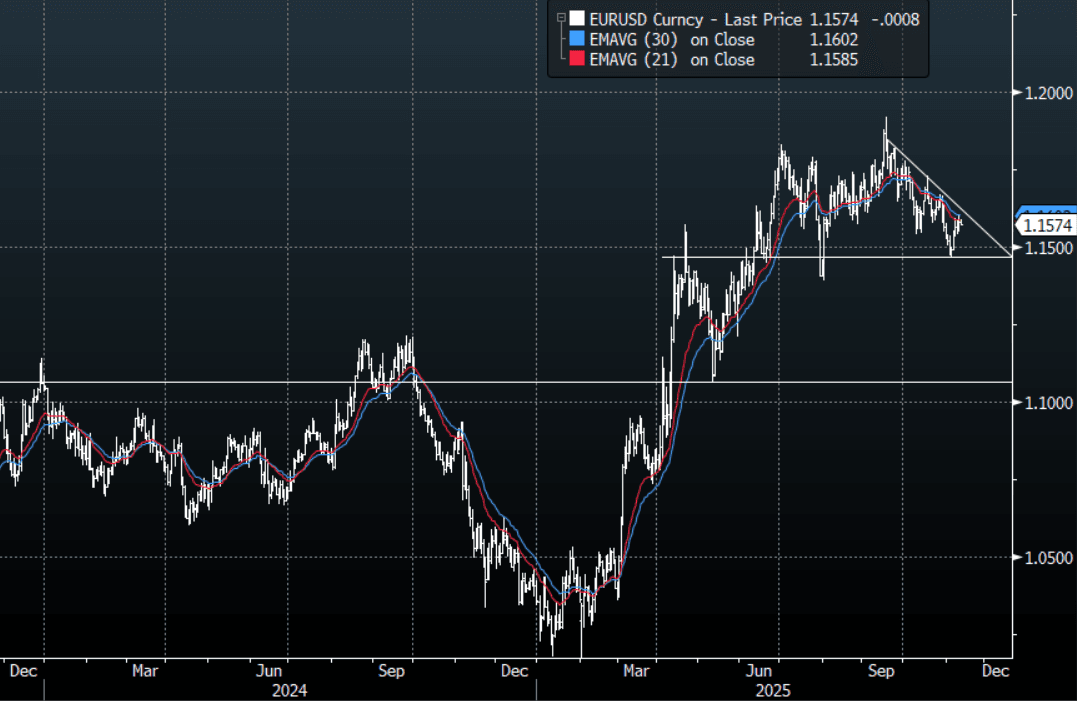

- EUR/USD - Asian range 1.1571 - 1.1587, Asia is currently trading 1.1572. The pair continued to build on its support below 1.1500, I suspect rallies will now find sellers toward the 1.1650 area initially. This 1.1650-1.1700 area has been the pivot within the larger 1.1400-1.1900 range over the past few months. On the day a move back below 1.1530-1.1540 needed to turn lower again.

- GBP/USD - Asian range 1.3130 - 1.3164, Asia is currently dealing around 1.3130. The pair is trading sideways consolidating on a 1.31 handle. I continue to favor fading rallies though as GBP looks to have put in a medium term top. I suspect the 1.3250-1.3300 area is the place to fade if we see that level again.

- Cross asset : SPX +0.15%, Gold $4110, US 10-Year 4.08%, BBDXY 1219, Crude Oil $60.85

- Data/Events : Germany Wholesale Price Index/CPI/Current Account Balance, Italy Industrial Production,

Fig 1: EUR/USD Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

CHINA: Country Wrap: September Exports Surge (Ex US) as Trade War Intensifies

Market Summary: With Japan out today, it was left to China's major bourses to guide sentiment as the trade war rhetoric ramps up. Having declined over -1.9% Friday, the CSI 300 started the week on the back foot, dragging the other key bourses with it. Down -1.7% today, it was the biggest two days of consecutive falls since April when the trade war began first ratcheted up. The Hang Seng fell sharply, down -3.3% as it traded through the key 20-day and 50-day EMA's and now is approaching the 100-day EMA which it last traded below in April. There was little positives to find as Shanghai Comp fell -1.30% and Shenzhen down -2.2%. The retail expansion of equity accounts over recent months has been a key contributor to the performance of stocks and comes on the back of a multi year decline in housing. The authorities will be loathe to see significant stock losses for investors and news agencies over the weekend were keen to spell out that the outlook for the CSI 300 should be little impact by the threats coming from Washington. The Yuan Reference Rate at 7.1007 Per USD; Estimate 7.1234 and bonds are staging a mini rally with the 10-Yr back down to 1.83%, having trade above 1.9% just prior to the recent break. The stability in CGBs comes despite the PBOC releasing details that it undertook no government bond trading for a ninth consecutive month.

- The moderation of exports in August was short-lived as September's numbers jumped +8.3% YoY, beating expectations and much stronger than the month prior. According to BBG estimates, the decline in exports to the US was significant, down -27% YoY. This points to the growth of demand from non US markets, arguably weakening the US's position in a trade war. Exports to Africa, India and other Asian nations are soaring with the latter back to pre-COVID levels. US President Donald Trump had threatened to raise tariffs on China and withdraw from a high-profile upcoming meeting with Chinese President Xi Jinping, in a lengthy statement on Truth Social, citing a letter from Beijing which he claims lays out new rare earth export control measures. The new Chinese rare earth export control measures are scheduled to take effect on December 1. Starting November 8, Beijing will also restrict exports of equipment needed to manufacture batteries for electric cars in a bid to protect the competitiveness of Chinese autos, per The New York Times. Imports climbed +7.4% in September for it's largest monthly expansion since April 2024. Despite being a crude indicator for domestic demand, the result nevertheless comes a an invaluable time as the US rhetoric ramps up. Along with the decline in exports to the US, imports from the US declined -16.1%, widening the trade surplus with the US to $22.bn. Whilst this data captures a period before the weekend's escalation it may slightly strengthen Beijing's position in negotiations, given the ever growing decline in the US's importance to China's trade outcome. (source MNI)

- Mainland China’s commercial and financial hub Shanghai has pledged to remove all regulatory hurdles for foreign investors to set up manufacturing businesses, as authorities move to shore up confidence in the local and national economies despite rising US-China trade tensions. Mayor Gong Zheng said on Sunday that deepened reforms had been carried out to grant overseas companies in the fields of electric vehicles, value-added telecommunications services, biotechnology and hospitals full access to the Chinese market. (source SCMP)

FOREX: Asia-Pac: USD Drifts Lower

The BBDXY has had a range of 1211.98 - 1214.25 in the Asia-Pac session; it is currently trading around 1212, -0.10%. The USD correction higher stalled just as it began to probe its longer-term resistance. The 1215-1225 area remains tough resistance, only a sustained close back above 1230 would start to challenge the conviction of the USD shorts. The weaker hands may be folding but I suspect we would need to do some work before the market can call a low for the USD as longer term accounts potentially look to fade this squeeze as they increase hedging ratios.

- EUR/USD - Asian range 1.1592 - 1.1628, Asia is currently trading 1.1620. Price found some decent demand towards its first support around the 1.1550 area; a break through here is needed to signal a deeper correction towards the more important 1.1200-1.1300 support. Expect sellers back towards the 1.1700 area first up.

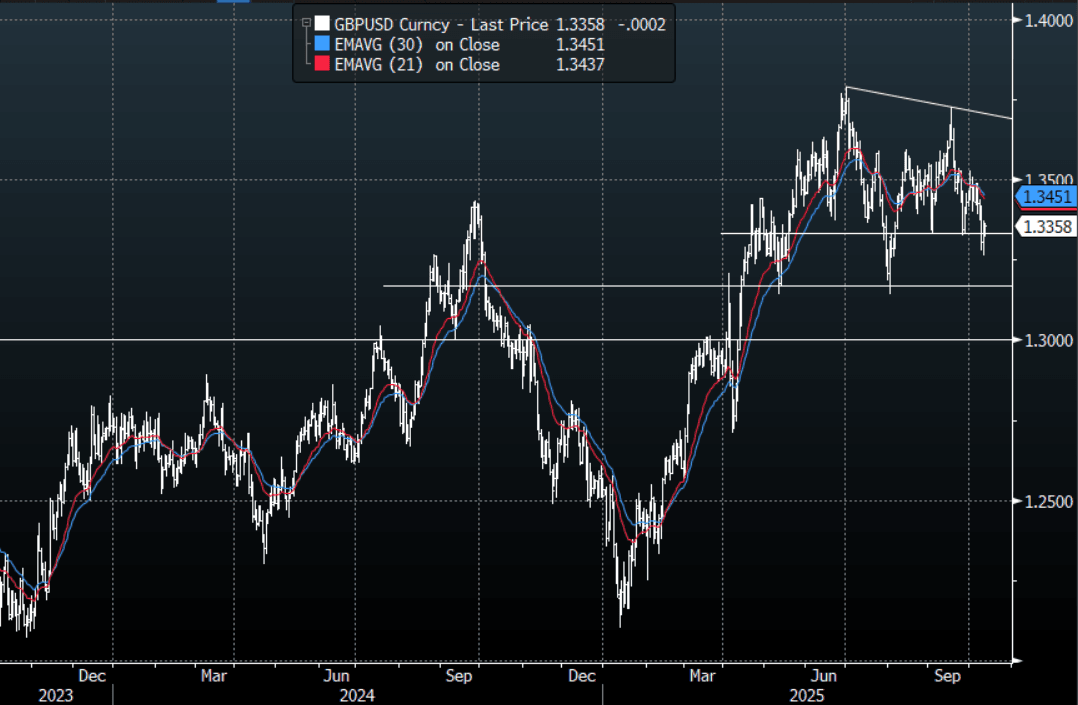

- GBP/USD - Asian range 1.3333 - 1.3363, Asia is currently dealing around 1.3360. The pair looks to have had a false break below the 1.3300 area. I suspect sellers should reemerge on any bounce back toward the 1.3450/1.3500 area.

- USD/CNH - Asian range 7.1320 - 7.1455, the USD/CNY fix printed lower at 7.1007, Asia is currently dealing around 7.1380. The area around 7.1500/1600 has proved to be solid resistance and with the PBOC managing the fix lower, it looks likely we could consolidate 7.09-7.16 for the moment.

- Cross asset : SPX +1.25%, Gold $4055, US TYZ5 112-31+, BBDXY 1212, Crude Oil $59.74

- Data/Events : Italy Bloomberg Oct. Italy Economic Survey, Germany Wholesale Price Index/Bloomberg Oct. Germany Economic Survey/Current Account Balance, EZ Bloomberg Oct. Eurozone Economic Survey, France Bloomberg Oct. France Economic Survey, Spain Bloomberg Oct. Spain Economic Survey

Fig 1: GBP/USD Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

AUSSIE BONDS: Key Resistance For Futures Remains Intact, RBA Mins Tomorrow

Aussie bond futures are holding higher, but away from best levels. Important key resistance points remain intact. 3yr futures were last 96.47 (+7bps), while 10yr futures were at 95.685 (+7bps). Earlier highs were at 96.505 for the 3yr and 95.7050 for the 10yr. Some cap for futures has come from the softer US Tsy futures tone and better risk appetite trends more broadly, with US official comments showing reduced recent rhetoric around US-China trade issues (albeit still with the threat of higher tariff levels come Nov 1, per remarks by US President Trump).

- Short term resistance points for futures are as follows. For 3yr: RES 1: 96.615 - High Sep 12 , while for 10yr: RES 1: 96.615 - High Sep 12.

- Cash ACGB yields are around 6-7bps lower across the curve, with the front end slightly weaker in yield terms. The 33yr benchmark last 3.50%, while the 10yr was at 4.29%, with little change in the Au3/10s curve.

- The bias is likely to be fade this yield move in Aussie, given RBA comfort around the current macro backdrop. A risk remains from higher US tariff levels on China, export controls etc, which could see negative spill over to the Australian economic outlook. For the 3yr Aussie bond, moves under 3.45% may be faded.

- At this stage, per Polymarket, 100% tariff odds by Nov 1 sit at 17%.

- Looking ahead to tomorrow, the publication of the September 30 decision minutes will be important given the Board’s more cautious tone and Bullock avoiding to state what the current stance is. She also noted that Board is concerned about certain CPI components including market services. NAB’s September business survey also prints on Tuesday.