US DATA: Another Trade Surprise But Goods Deficit Is Still Smallest Since 1990s

Jan-29 19:13

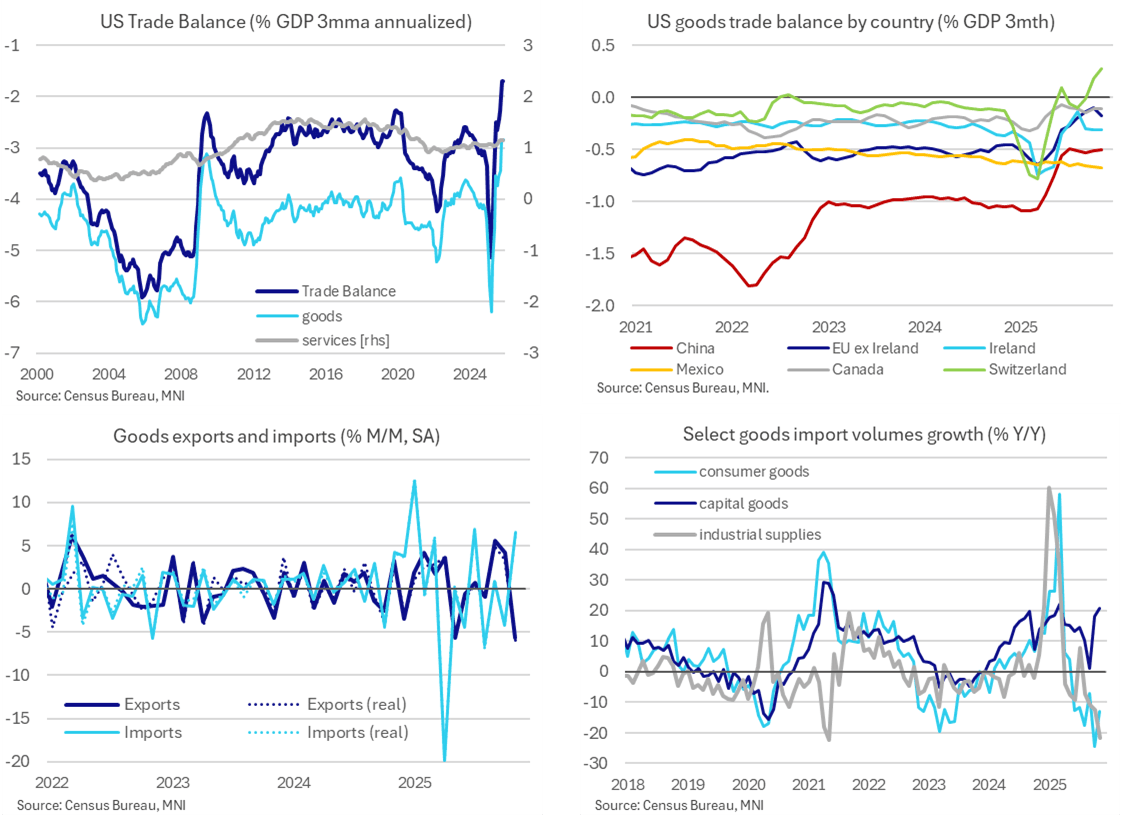

Volatility remained rife in trade data for back in November, with the goods & services deficit surprising higher after the particularly small deficit in last month’s update. The recent goods-only deficit at 2.8% GDP continues to track at its lowest since the late 1990s.

- The goods & services trade deficit swung back higher in November, to $56.8bn (cons $44bn) after $29.2bn in Oct ($29.4bn initially in what had been a much smaller than expected print last month) for its largest monthly deficit since July.

- It was driven entirely by the goods deficit ($86.9bn after $59bn in Oct and $78bn in Sep) whilst the services surplus held at $30.1bn after $30.0bn.

- Highlighting the volatility, goods exports fell -5.6% M/M after 4.2% whilst goods imports rose 6.6% M/M after -4.3%. Drivers here include a pullback in gold exports along with higher computer and pharma imports – see part two.

- It left a goods & services trade deficit unchanged at 1.7% GDP on a three-month rolling basis, whilst the goods deficit narrowed a tenth to 2.8% GDP (a new recent low since the late 1990s) and the services surplus dipped back a tenth to 1.1% GDP.

- Last month’s Q3 current account release caught President Trump’s attention, writing at the time on the goods balance that: “Numbers released today show that the United States of America has the lowest Trade Deficit since 2009, and going even lower”.

- Comparing the latest three month goods balances with those from end-2024 by country, the largest adjustments have come from China at +0.5pp (deficit halved from 1.0% to 0.5% GDP), Switzerland at +0.5pp (deficit of 0.3% GDP to a surplus of 0.3 GDP) with gold shipment volatility at play, and the EU ex Ireland at +0.3pp (deficit from 0.5% to 0.2% GDP).

- USMCA partners continue to have seen relatively little change however, with the Canadian balance improving by just 0.1pp (deficit from 0.2% to 0.1% GDP) and the balance with Mexico actually widening 0.1pp (deficit from 0.6% to 0.7% GDP).

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US TSYS: Post-FOMC Minutes React

Dec-30 19:01

- Treasury futures show little reaction to the FOMC minutes release for the December meeting, holding modest losses, near midrange for the day

- Currently, TYH6 trades 112-20 (-3.0) vs. 112-17 low / 112-25.5 high, curves mixed: 2s10s at 66.528 +1.165, 5s30s -.381 at 112.333.

- Trend theme remains bearish and a break of 111-29 would confirm a resumption of the bear cycle. This would open 111-19, a Fibonacci projection. Key short-term resistance has been defined at 112-31, the Dec 18 high, where a break would undermine a bear theme and signal scope for a stronger recovery instead.

- Bloomberg US$ index firmer: BBDXY +1.25 at 1202.72

MNI: MOST SAW FURTHER CUTS IF INFLATION DECLINES - FED MINUTES

Dec-30 19:00

- MOST SAW FURTHER CUTS IF INFLATION DECLINES - FED MINUTES

- SOME WANT RATES UNCHANGED FOR SOME TIME AFTER DECEMBER

- PARTICIPANTS EXPRESSED RANGE OF VIEWS ON RESTRICTIVENESS

- PARTICIPANTS JUDGED CAREFUL BALANCING OF RISKS REQUIRED

- PARTICIPANTS SEE ELEVATED NEAR-TERM PRICES, RETURN TO 2%

- MOST SEE LABOR MARKET RISKS TILTED TO DOWNSIDE

SOFR OPTIONS: SOFR Put Strip & Midcurve Vol Sales

Dec-30 18:55

Modest tone change from better low delta put buying earlier: put strip seller and midcurve vol seller via straddles ahead of the Dec'26 FOMC minutes release

- -1,000 SFRU6/SFRZ6/SFRH7/SFRM7 95.00 put strip, 6.0 total

- -2,000 0QH6 96.93 straddles, 28.0 ref 96.925

- -1,000 0QF6 96.93 straddles, 14.0 ref 96.925

Trending Top

Mar-27 20:13