UK: Another Senior Gov't Figure Leaves With PM Still Under Pressure

Feb-12 16:57

10 Downing Street has confirmed that the UK's seniormost civil servant, Cabinet Secretary Sir Chris ...

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US STOCKS: Midday Equities Roundup: Reversing Post-CPI Gains, Financials Lagging

Jan-13 16:47

- Stocks are holding weaker ahead midday Tuesday, reversing short post-data rallies to new record highs in SPX eminis (7,036.25) and Nasdaq (23,813.30) after markets digested the anomalous CPI inflation data.

- Underperforming by late morning, the DJIA currently trades down 276.18 points (-0.56%) at 49316.86 after failing to breach yesterday's record high of 49,633.35, the S&P E-Mini Futures down 7 points (-0.1%) at 7010.5, Nasdaq up 25.3 points (0.1%) at 23761.62.

- Energy, IT and Health Care sector shares primarily led advances in the first half, oil and gas shares buoyed by another geopol-risk driven rally in crude (WTI +1.78 at 61.28): Texas Pacific Land Corp +3.94%, APA Corp +3.91%, EOG Resources +3.26%, Devon Energy +3.11% and Diamondback Energy +2.95%

- Semiconductor makers faired well in the first half: Advanced Micro Devices +5.79%, Intel Corp +5.79%, Jabil +4.18%, Arista Networks +3.11%, Corning Inc +2.99% and ON Semiconductor Corp +2.02%.

- While pharmaceuticals buoyed the Health Care sector: Moderna +11.35%, Revvity +5.57%, Cardinal Health +4.51%, Charles River Laboratories +2.31% and Cencora +1.71%.

- Conversely, Financial sector shares underperformed: Mastercard -4.66%, Visa -4.54%, T Rowe Price Group -3.53%, Progressive Corp -2.86%, Arthur J Gallagher -2.77% while JPMorgan Chase declines -2.77% to 315.0 after hitting 326.78 briefly after reporting earnings that included over a $2B credit card losses.

US 10YR FUTURE TECHS: (H6) Spike Sold

Jan-13 16:44

- RES 4: 113-00+ 61.8% retracement of the Nov 25 - Dec 10 bear leg

- RES 3: 112-31 High Dec 18 and key short-term resistance

- RES 2: 112-25+ High Dec 30 / 31

- RES 1: 112-22 High Jan 7

- PRICE: 112-05+ @ 16:40 GMT Jan 13

- SUP 1: 111-29 Low Dec 10 and the bear trigger

- SUP 2: 111-19 1.236 proj of the Oct 17 - Nov 5 - 25 price swing

- SUP 3: 111-11 1.382 proj of the Oct 17 - Nov 5 - 25 price swing

- SUP 4: 111-00 Round number support

Prices rallied sharply on the CPI print, but the spike was quickly sold to leave the outlook softer for now, albeit above a key support at 111-29, the Dec 10 low. The trend set-up is bearish and a breach of 111-29 would confirm a continuation of the bear cycle. Note that a head and shoulders reversal pattern on the daily chart also highlights a bearish threat. Scope is seen for a move towards 111-19 initially, a Fibonacci projection. Key short-term resistance is unchanged at 112-31, the Dec 18 high.

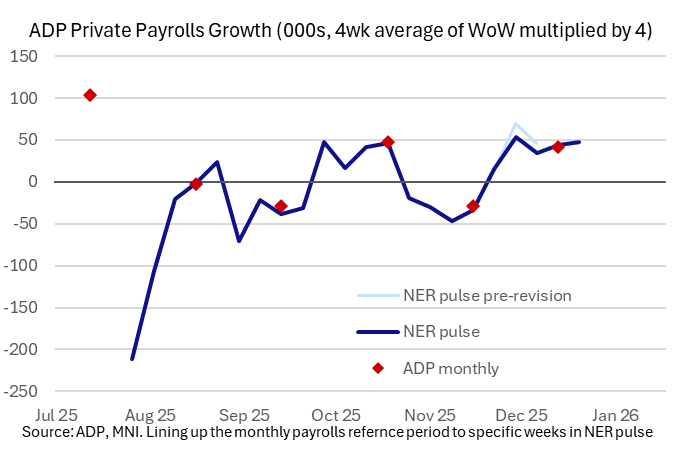

US DATA: Weekly ADP Sees Similar Tracking To Last Week’s December Update

Jan-13 16:39

- ADP earlier today reported solid private payroll growth averaging 11.75k per week in the four weeks to Dec 20.

- It follows an 11k in the week to Dec 13 (as you’d expect broadly chiming with the 41k increase in the monthly report published last week with its reference week including the 12th of the month) plus downward revisions to 8.75k (initial 11.5k) to Dec 6 and 13.25k (initial 17.5k) to Nov 29.

- Being only one week on from the monthly report it doesn’t offer much new information, but it at least continues a reasonably solid trend by recent month standards. A monthly equivalent of 47k is close to the 41k increase in the December report after a volatile few months with -29k in Nov, 47k in Oct and -29k in Sept.

- ADP proved to be a useful indicator ahead of private payrolls in Friday's December BLS report, which saw a 37k increase vs consensus of 75k. The previous correlation has been mixed though, with BLS private payrolls increasing 50k in Nov (vs that -29k for ADP) and just 1k in Oct after a heavily downward revised previous estimate of 52k (vs 47k for ADP).