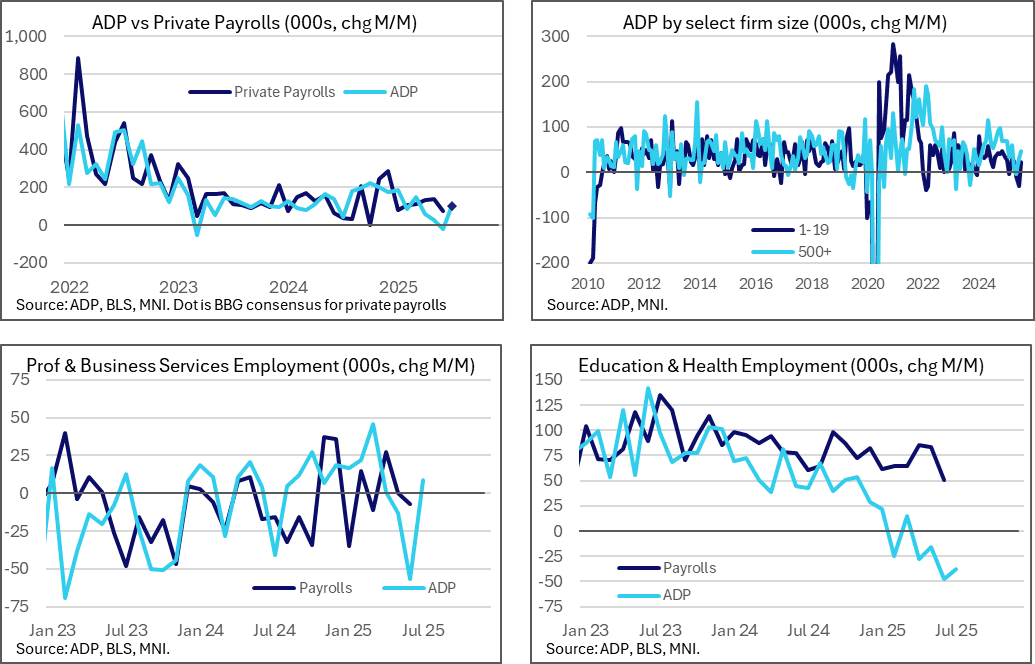

US DATA: ADP Surprises Stronger, With Improvements Across Most Sectors

Jul-30 12:28

- ADP private employment was stronger than expected in July, increasing 104k (cons 76k) after an upward revised but still unusually weak -23k (initial -33k) in June.

- Service-providing jobs increased 74k and goods-producing jobs increased 31k.

- Within services, there were sequential improvements almost across the board with exception for the education & health which continues to strangely weak compared to its BLS payrolls counterpart.

- The largest sequential improvement came for “professional and business” at 9k after a particularly heavy -57k and “financial activities” at 28k after a rare -12k.

- “Education & health” continued to buck the trend, falling -38k after -48k for a fifth monthly decline across the past six months. Highlighting just how weak this has been relative to payrolls, it averaged -31k in Q2 and 4k in Q1 compared to 73k and 64k for education & health private payrolls.

- Smallest businesses (1-19 employees) had come under most pressure with -31k in June but somewhat bounced back with 22k in July.

- ADP’s Nela Richardson on the report: “Our hiring and pay data are broadly indicative of a healthy economy. Employers have grown more optimistic that consumers, the backbone of the economy, will remain resilient."

- From the separate Pay Insights report: “ADP Pay insights:

- "Year-over-year pay growth in July was 4.4 percent for job-stayers and 7 percent for job-changers. Gains have held steady for the past four months."

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

GLOBAL POLITICAL RISK: Week Ahead 30 June-6 July

Jun-30 12:16

Download Full Report Here

(MNI) London – All timings are subject to change.

Monday 30 June:

- United States: The US Senate is set to start a ‘vote-a-rama’ on the One Big Beautiful Bill at around 09:00ET. These sessions can last around 9-15 hours. Following the close 51-49 vote that advanced the reconciliation bill on 28 June, the legislation is expected to pass at some point on 30 June, or on the morning of 1 July. It will then return to the House of Representatives.

Download full PDF report from link at top or below:

FOREX: Analyst Views on Further Dollar Depreciation

Jun-30 12:10

- *Goldman Sachs: The fast USD depreciation trajectory is very much in line with other large depreciation episodes from the peak. Beyond this point, the move has often become slower and choppier across historical episodes.

- A clearer dovish tilt from the Fed on the back of more visible weakening in the upcoming labour market data could be an important near-term catalyst, sparking further Dollar weakness versus majors such as EUR and JPY.

- Absent that, a more gradual grind weaker in the Dollar is still the most likely outcome, supporting EM carry strategies, and a steady move stronger in CNY, with implications across Asia.

- *JP Morgan cites the main anchors of their bearish USD view remaining unchanged. Specifically, moderation in US growth, global longs in US equities (or assets), growth-supportive fiscal and monetary policies outside the US, and higher probability of a structural USD weakening, which deserves a dollar discount.

- To JPM, conditions are favourable for EM currencies to outperform the US dollar and past experience indicates that once initiated, dollar bear cycles can persist for a while. In their latest FX weekly publication, JPM remain bullish the euro- and Antipodean bloc FX.

- *ING say the balance of risks remains tilted to the downside for the dollar, but their calls for only a gradual slowdown in payrolls and an inflation bump in the coming months imply that markets have overshot on dovish pricing. A September cut may be ultimately priced out, and some short-term support for the dollar should emerge. Conversely, a major payrolls disappointment can send DXY below 96.0 even without the OBBBA and tariff factors.

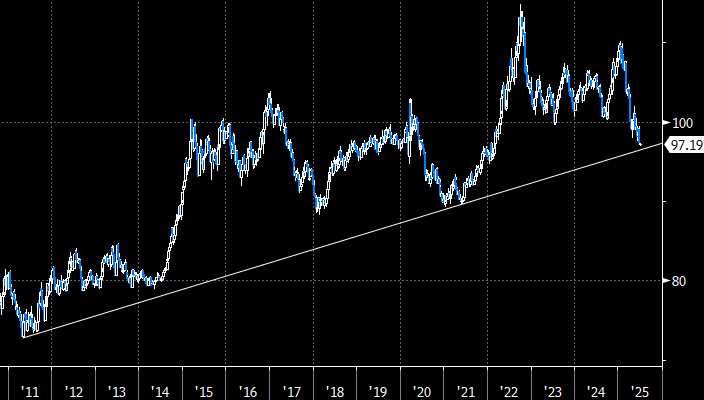

FOREX: Dollar Index Approaching Long-Term Trendline Support

Jun-30 12:08

- The dollar index resumed its downtrend last week, closing at its lowest weekly level since February 2022. Price action has propelled the likes of EURUSD above 1.17, GBPUSD above 1.37, while USDCHF has continued to plumb fresh 10-year lows below the psychological 0.8000 mark.

- Analysts have been quick to highlight that the latest greenback selling has notably been paired with an adjustment lower for the front-end of the US curve, which was pertinent alongside a significant reduction in geopolitical risk premia. This dynamic may place a greater focus than usual on this week’s US employment report, notably scheduled on Thursday owing to the July 4th holiday. Using EURUSD as a proxy for the potential dollar move, the break-even on a Thursday straddle sits at +/- 85 pips.

- Interestingly, the long-term uptrendline for the dollar index, drawn across the 2011 and 2021 lows, intersects around 80pips below current levels at 96.40, which remains a key medium-term target for the move. Options pricing might suggest this level as providing solid support on a first test and a potential obstacle to EURUSD’s well-forecasted move towards 1.20.

- With material changes in immigration flows under the Trump administration, breakeven rates of payrolls growth are likely much lower than last year. It should keep focus on the unemployment rate as a broad barometer of labour market slack even if it’s from the noisier household survey. Separately, ISM and JOLTS data will also provide important inputs into short-term expectations for Fed pricing.

Source: Bloomberg Finance L.P. / MNI