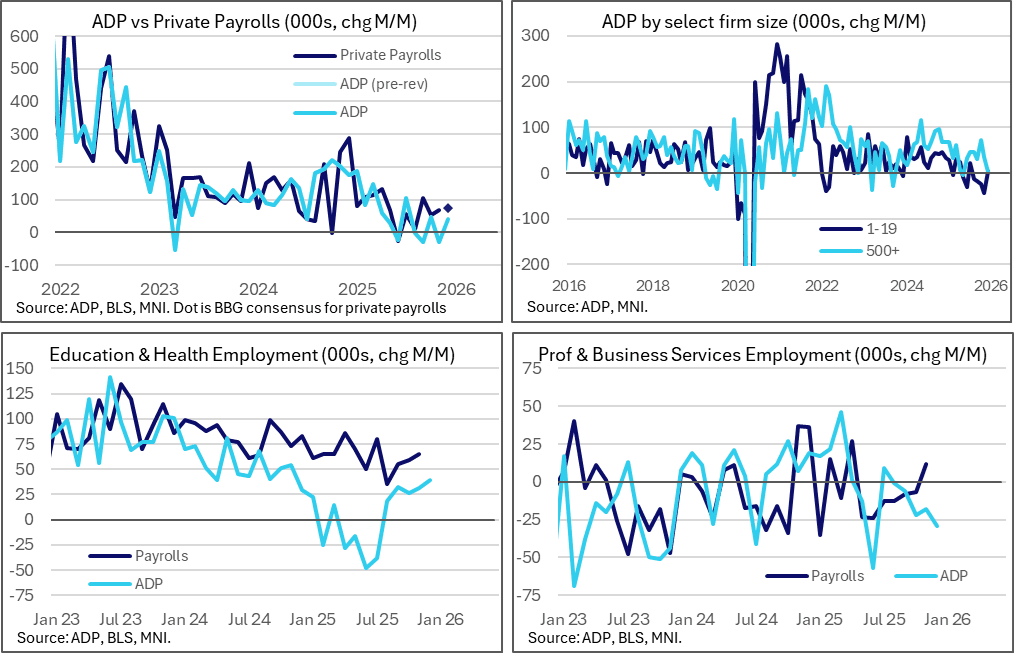

US DATA: ADP Employment Increase A Touch Softer Than Tracking

ADP private employment modestly disappointed Bloomberg consensus in December but was closer to weekly tracking when considering volatility within the data. It continues a trend of oscillating between modest declines and then increases in recent months, and has declined in three of the past six months. At 41k and a three-month average of 20k it confirms an alternative indicator that is softer than the 73k increase expected for BLS private payrolls on Friday, although it has mostly undershot the latter for the past six months.

- ADP private employment increased 41k in December, a small miss on Bloomberg consensus of 50k and weekly tracking equivalent to 46k.

- That’s close to being in line with weekly tracking when considering a realistic margin of error given how much these weekly figures can move. The monthly equivalent of the four weeks to Dec 6 of 46k followed a monthly 70k in the update up to Nov 29 and 15k up to Nov 22 (with this monthly update based on a reference period around the 12th of the month).

- Still, it confirms an alternative indicator that is softer than the 73k increase expected for private payrolls in Friday’s BLS report. That said, it has undershot private payrolls growth for some time, with an average undershoot of 33k over the past six months including 98k in November.

- The 41k increase follows -29k in Nov (revised from -32k first reported) after 47k in Oct and -29k as it’s oscillated between small declines and increases in recent months.

- Services drove the increase (+44k after -9k) as it continued to be supported by education & health (39k after 31k) along with a large increase in leisure & hospitality (24k after 14k). Professional & business services saw the largest monthly decline (-29k after -18k). Monthly correlation with equivalent BLS payrolls series is at best mixed for these sectors.

- Goods-producing industries meanwhile fell by 3k after -18k, with a third consecutive decline for manufacturing jobs (-5k after -18k in Nov).

- A recent theme of smallest firms suffering and largest firms driving jobs growth appeared to pause in December. Those with 1-19 employees saw headcount increase by 4k after four-month cumulative decline of -100k before that (including -44k in Nov) whilst those with 500+ employees saw headcount increase just 2k after a four-month increase of 186k (including 36k in Nov).

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

EURIBOR OPTIONS: Calendar Call Spread

ERZ5/M6 98.25/98.37cs calendar spread, bought the Z6 for 1 in 25k.

US TSYS: Early SOFR/Treasury Option Roundup: Hedging Hawkish Cut

FI desks reported mixed SOFR & Treasury options overnight - leaning towards puts ahead of Wed's FOMC policy annc, anticipating a hawkish cut. Underlying futures moderately lower, curves flatter (2s10s -0.714 at 56.555, 5s30s -1.525 at 106.249). Projected rate cut pricing large steady vs late Friday levels (*): Dec'25 at -24.9bp (-23.8bp), Jan'26 steady at -31.0bp, Mar'26 steady at -38.7bp, Apr'26 steady at -45bp.

- SOFR Options:

- +2,000 SFR5 96.18 puts, 1.0

- 2,000 SFRZ6 96.31/96.43/96.56 call flys ref 96.265

- 14,000 SFRZ6 96.87/97.37 call spds 0.5 over 96.50 puts

- 1,100 SFRG6 96.25/96.37/96.43/96.50 broken put condors

- 6,700 SFRZ5 96.50/96.87/97.37 broken call trees ref 96.83

- +3,000 SFRZ5 96.18/96.25/96.31 put flys, 2.5 ref 99.265

- Block, +4,300 SFRH6 96.18/96.43/96.56 broken put flys, 0.0 ref 96.43

- -5,250 SFRZ5 96.31/96.37 call spds, 0.25 net ref 96.265

- Blocks +6,000 0QH6 96.12/96.25/96.37 put flys, 0.5

- +3,370 SFRZ6 99.00/100/101 call flys, 2 vs. 96.89/0.05%

- 1,785 SFRZ5 96.31/96.37 call spds ref 96.265

- 1,350 0QZ5 96.62/96.87/97.00/97.12 broken put condors ref 96.835

- -10,000 0QF6 96.93/97.06 call spds, 3 ref 96.85

- Treasury Options:

- 4,400 FVF6 108.5/110.25 strangle vs. FVG6 108.25/110.25 strangle

- over 4,000 TYH6 110 puts, 14

- 2,000 TYF6 110/111.5 put spds ref 112-13

- 2,000 TYF6 110.5/112 put spds ref 112-13

- over 39,800 TYF6 112 puts, 17-20

- 5,650 TUH6 104 puts, 9

- 1,500 TYF6 113 straddles

- +2,000 TYF6 112/113 2x5 call spds 10

- +4,000 TYF6 111.5 puts, 9 vs. 112-16/0.18%, total volume over 10k

- +1,500 TYH6 113.5 calls vs. TYG6 114 calls, 20 net (Mar over)

- -20,000 TYF6 112/112.5 put spds vs. 114.5 calls, 11 net ref 112-15

- +1,600 FVF6 108.25/108.75 put spds, 6.5 vs. 109-06.25

- +5,000 TYF6 111.25/112.25 put spds vs. 113.5/114.5 call spds 12 net ref 112-115

- over 7,100 wk2 TY 112.5 puts, 14 exp Fri

- +2,130 TYH6 110/111/112 put flys, 9 ref 112-18

FOREX: Scotia Point to Significant CAD Narrative Shift, JPM Remain Bearish

- USDCAD has printed 1.3800 in recent trade, moderately extending the impressive move lower following Friday's employment report. Despite the recent breakout, Scotiabank and JPM have differing views over the devlopments for the Canadian dollar.

- While Scotiabank acknowledge the latest employment data was not entirely positive; they believe the latest trends point to a significant narrative shift for the CAD after a prolonged period of tariff-driven doldrums. Consequently, Scotia highlight that markets have moved quickly to price in the start of the BoC tightening cycle late next year, which has been Scotia’s base case view for some time.

- Scotia point out that USDCAD is trading very close to their fair value estimate (1.3801) today and expect the CAD to remain well-supported on minor dips.

- Meanwhile, JP Morgan highlight that their desk saw significant CAD demand from real money, hedge funds, and systematic accounts, with Friday’s move seeing decent follow through given CAD shorts remain a widely held position.

- However, JPM are not turning bullish at this stage and instead plan to use this move as an opportunity to buy USDCAD topside into next year, which they will continue to use as a funder to EM FX longs.