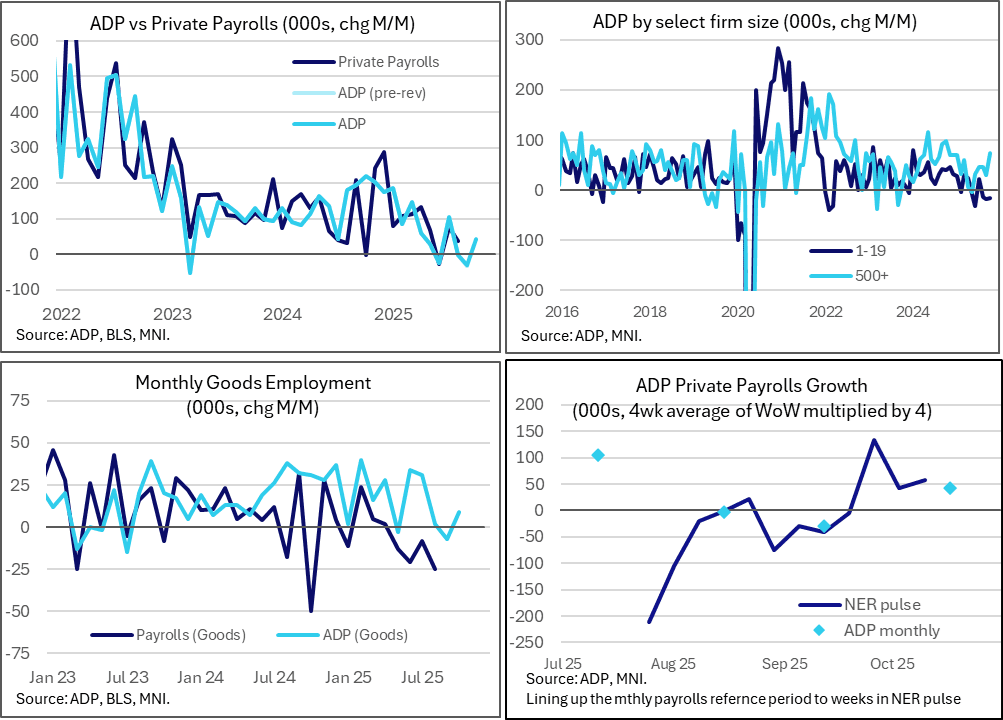

US DATA: ADP Confirms Payroll Stabilization In October, Trend Still Very Soft

ADP private payrolls growth stabilized in October after two monthly declines, coming in between Bloomberg consensus and last week’s fresh ADP New Pulse report along with minimal revisions. The combination drove only a marginal hawkish reaction.

- ADP employment change: 42k (cons 30k) in October after -29k (initial -32k) in Sept and -3k (initial -3k) in Aug.

- Whilst a small beat of consensus at 30k, it’s also not as solid as the 57k implied by last week’s newly published weekly series for the four weeks ending Oct 11, i.e. just shy of the reference period used for this month’s October report.

- The three-month average now stands at just 3k despite this latest increase. It has steadily declined from a recent peak of 206k in Nov 2024, moderating in all but one month since then.

- These private sector job gains look concentrated, with “trade, transportation & utilities” seeing +47k after two weak months, “education & health” +25k and “financial activities” +11k.

- Largest declines were seen with information -17k, professional business services -15k and other services -14k. That’s a third straight monthly decline for professional business services, information and leisure & hospitality.

- Largest firms continue to see most resilience: those with 500+ employees saw headcount rise by 74k compared to a next highest of 5k for those with 20-49 employees. That follows September when only firms with 500+ employees saw net job creation.

- There’s no clear story behind which of the smaller firms are most heavily affected though, with firms with 50-249 employees seeing a second month of largest declines, outstripping declines in the smallest 1-19 employee category.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

ECB: ECB Speak Wrap (Sep 25 – Oct 6)

The past two weeks has seen an increase in the frequency of ECB Executive Board monetary policy commentary. There haven’t been any major surprises, with Lagarde, de Guindos, Lane and Cipollone all providing some variant of rates being in a “good place” at present.

For a full summary of ECB speak since the September decision, see here

SOFR OPTIONS: Red Pack Vol Buyer

SFRU6/Z6/H7/M7 96.875^, bought for 306.5 in 300 lots.

EQUITY TECHS: E-MINI S&P: (Z5) Northbound

- RES 4: 6831.38 2.500 proj of the Aug 20 - 28 - Sep 2 price swing

- RES 3: 6819.25 1.500 proj of the Aug 1 - 15 - 20 price swing

- RES 2: 6812.29 2.382 proj of the Aug 20 - 28 - Sep 2 price swing

- RES 1: 6800.00 Round number resistance and Friday’s high

- PRICE: 6786.50 @ 14:24 BST Oct 6

- SUP 1: 6684.22 20-day EMA

- SUP 2: 6624.25 Low Sep 25

- SUP 3: 6566.78 50-day EMA

- SUP 4: 6506.50 Low Sep 5

A bull cycle in S&P E-Minis remains intact. The contract traded to a fresh cycle high last week to confirm a resumption of the uptrend and maintain the positive price sequence of higher highs and higher lows. Sights are on 6812.29, a Fibonacci projection. Initial support to watch is at the 20-day EMA, at 6684.22. It has recently been pierced, a clear break of it would signal scope for a deeper pullback, potentially towards the 50-day EMA, at 6566.78.