AUSSIE BONDS: ACGB Nov-33 Auction Results

The Australian Office of Financial Management (AOFM) sells A$800mn of the 3.00% 21 November 2033 bond:

- Average Yield (%): 4.1592 (prev. 4.0742)

- High Yield (%): 4.1600 (prev. 4.0750)

- Bid/Cover: 4.9300x (prev. 3.2850x)

- Allotted at Highest Accepted Yld as % of Bid at that Yld (%): (prev. 64.8)

- Bidders 33 (prev. 33), successful 10 (prev. 13), allocated in full 2 (prev. 5)

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

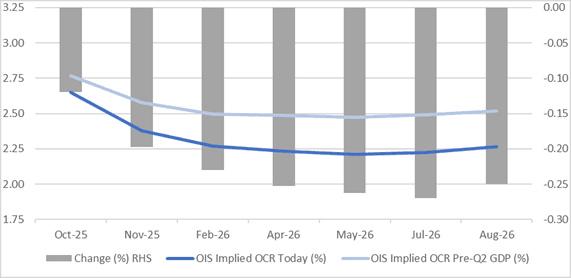

STIR: RBNZ-Dated OIS Set To Move After Today’s RBNZ Decision

RBNZ-dated OIS pricing is slightly firmer across meetings today ahead of today’s RBNZ Policy Decision.

- Easing expectations show 36bps of easing priced for today’s meeting, with a cumulative 63bps by November 2025 and 73bps by February 2026.

- Today’s decision is likely to have a material impact on pricing. A 50bps cut could bring forward the full 75bps of cumulative easing to November, while a 25bps cut would likely push at least half of that 25bps into early 2026.

- Notably, pricing is 12-27bps softer across meetings versus 18 September’s pre-Q2 GDP levels.

- Both the production and expenditure-based GDP measures fell 0.9% q/q in Q2, the weakest since the pandemic. The RBNZ had expected a 0.3% q/q decline.

Figure 1: RBNZ Dated OIS Current vs. Pre-Q2 GDP (%)

Source: Bloomberg Finance LP / MNI

AUSSIE BONDS: ACGB Mar-36 Auction Result

The AOFM sells A$1200mn of the 4.25% 21 March 2036 bond:

- Average Yield (%): 4.3788 (prev. 4.2569)

- High Yield (%): 4.3800 (prev. 4.2600)

- Bid/Cover: 3.4917x (prev. 3.3111x)

- Allotted at Highest Accepted Yld as % of Bid at Yld (%): 84.6 (prev. 24.0)

- Bidders: 41 (prev. 33), successful 17 (prev. 16), allocated in full 9 (prev. 13)

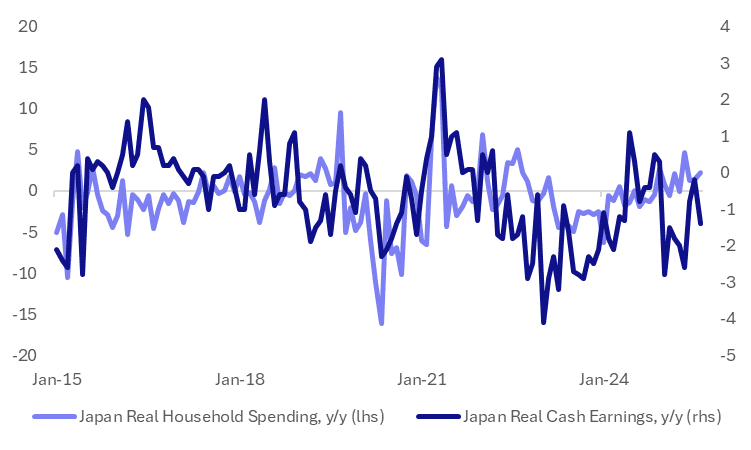

JAPAN DATA: Aug Labor Earnings Notably Sub Forecasts, BoJ Likely Holding In Oct

August labour earnings data in Japan was comfortably below market expectations. Headline earnings rose 1.5%y/y (against a 2.7 forecast and 3.4% July outcome), while real earnings dipped back to -1.4%y/y (-0.5%) was forecast. Real earnings have not been in positive territory (in y/y terms) so far in 2025. This will reinforce expectations of the BoJ likely remaining on hold at the Oct policy meeting. Japan's new political regime had already noted that Oct is too soon for a rate hike. BoJ Governor Ueda also noted recently that the risk was low for the central bank to fall behind the inflation/policy curve( with today's data supporting this theme).

- The chart below updates the household spending versus real labour earnings trend post today's data. Recall yesterday that household spending was stronger than forecast but today's real earnings data re-opens a modest wedge between the two series. This may create uncertainty around the extent which the positive trend in household spending can be maintained.

- Bonus payments were down notably in y/y terms, off -10.5%y/y, versus a 6.3% gain in July, so this provides some offset to the softer headline results. We can often bounce back after negative months.

- On a same sample base, cash earnings printed at 1.9%, versus 2.7% forecast. Scheduled full time pay on the base y/y was 2.4% against a 2.5% forecast. Special payments fell -5.7%y/y (against a 4.7% rise in July).

- This may help offset the weaker than expected headline outcomes, but still the BoJ and authorities are likely to want to see stronger underlying earnings momentum.

Fig 1: Real Earnings Struggling For Positive Momentum

Source: Bloomberg Finance L.P./MNI