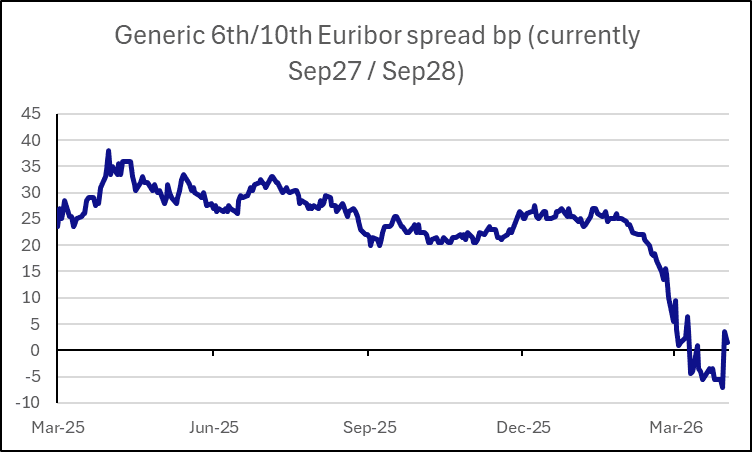

STIR: A less hawkish ECB could pressure red/green Euribor spreads higher

- A less hawkish than expected ECB would disappoint current pricing and could drive some further reversal of the bear-flattening in red/green Euribor spreads.

- Excessive ECB hike expectations have been pared back in line with the de-escalation in the Middle East conflict. In addition, yesterday's MNI sources story suggested there is now less pressure on the Governing Council to act as urgently. There’s now 7bps of hikes priced for April versus 17bps on Tuesday.

- Uncertainty will linger, however, especially as the Governing Council may opt to wait until June’s meeting to have more evidence and fresh forecasts to assess the outlook.

- The upside risks for inflation are clear, but expectations remain contained. At 2.13%, the 5Y5Y inflation swap rate is less than 5bp above its average level over the last year.

- If 5Y5Y remains anchored, it should help drive some further scaling back of hiking expectations, particularly as it will be difficult for wage growth to gain traction with the vacancy rate having been on a sustained downtrend since its mid-2022 peak of 3.3%.

Bloomberg Finance L.P, MNI

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

OUTLOOK: Price Signal Summary - Trend Needle In EURUSD Points South

- In FX, the move higher in EURUSD is - for now - considered corrective. A bear cycle is in play and Monday’s fresh cycle low reinforces current conditions. Scope is seen for a move towards 1.1491, the Nov 21 ‘25 low. Note that MA studies highlight a bearish cross - if confirmed this would signal a medium-term bearish development. Initial firm resistance is at 1.1718, the 20-day EMA.

- The trend condition in GBPUSD remains bearish and the latest recovery appears corrective - for now. A resump[tion of weakness would signal scope for a move towards 1.3212, the 76.4% retracement of the Nov 4 ‘25 - Jan 27 bull cycle. On the upside, initial firm resistance is seen at 1.3575, the Feb 26 high.

- The trend set-up in USDJPY is bullish. Resistance at 157.76, the Feb 9 high, has been cleared. The clear breach of this level opens 159.45, the Jan 14 high and a key hurdle for bulls. On the downside, initial firm support lies at 155.94, the 50-day EMA.

US TSYS: Oil-Related Geopol Leads Before US CPI, 10Y Supply and Trump Remarks

Treasuries are mostly slightly lower on the day, with admittedly modest further selling pressure easing with crude futures off session highs and US equity futures off lows. Oil reserve releases are in immediate focus along with the Middle East conflict more broadly with the US saying it hit 16 Iranian mine-laying vessels near the Strait of Hormuz after Iran moved to further impede transit. Today’s docket sees February CPI in focus before 10Y supply and various opportunities for Trump remarks.

- Cash yields are 0.5bp lower (3s) to 1.2bp higher (20s and 30s).

- TYM6 trades at 112-08+ (-06) off an earlier low of 112-06, on reasonable cumulative volumes of 395k even if that’s much less most overnight sessions in the past two weeks.

- Recent gains appear corrective with a bear threat still present with support at 111-26+ (Mar 6 low, bear trigger) before 111-21+ (Feb 9 low). Resistance is seen at 112-22 (20-day EMA) before yesterday’s 112-24+ (Mar 10 high).

- Data: Weekly MBA (0700ET), CPI Feb (0830ET), Real av earnings Feb (0830ET), Federal budget balance Feb (1400ET)

- Fedspeak: VC Supervision Bowman on regulation (0830ET)

- Coupon issuance: US Tsy $39B 10Y Note re-open - 91282CPZ8 (1300ET). Yesterday’s 3Y saw a rare 1.1bp tail with soft stats, whilst last month’s 10Y also tailed by 1.5bps with the bid-to-cover slipping from 2.55 to 2.39.

- Bill issuance: US Tsy $69B 17W bill auction (1130ET)

- Politics: Trump in site visit at Thermo Fisher Scientific (1430ET), Trump in local TV interview (1505ET), Trump in podcast interview (1600ET), Trump delivers remarks (1625ET)

BONDS: Basing As Bid In Crude Fades

Core global FI markets find a base as WTI & Brent trade back from session highs, with the correlation between the two remaining elevated given focus on the situation in the Middle East and related energy vol.

- Bunds and gilts still bear flatten on the day, while Tsys bull flatten.

- Move lower in crude comes as various countries flag support for IEA-led action.

- Most recently, local reports have noted that Germany is set to release stockpiles from its strategic reserve.

- Austria has signalled support and readiness to act in accordance with any IEA-led stockpile releases.

- Japan has signalled that it will release stockpiles from its strategic reserve, irrespective of the IEA decision, along with introducing curbs for gasoline prices.

- A reminder that RTRS sources reported that the IEA is set to announce its recommendation on the joint strategic oil reserve release at 13:00 London. Several source reports have pointed to the IEA recommending a record release of 300-400mln barrels.