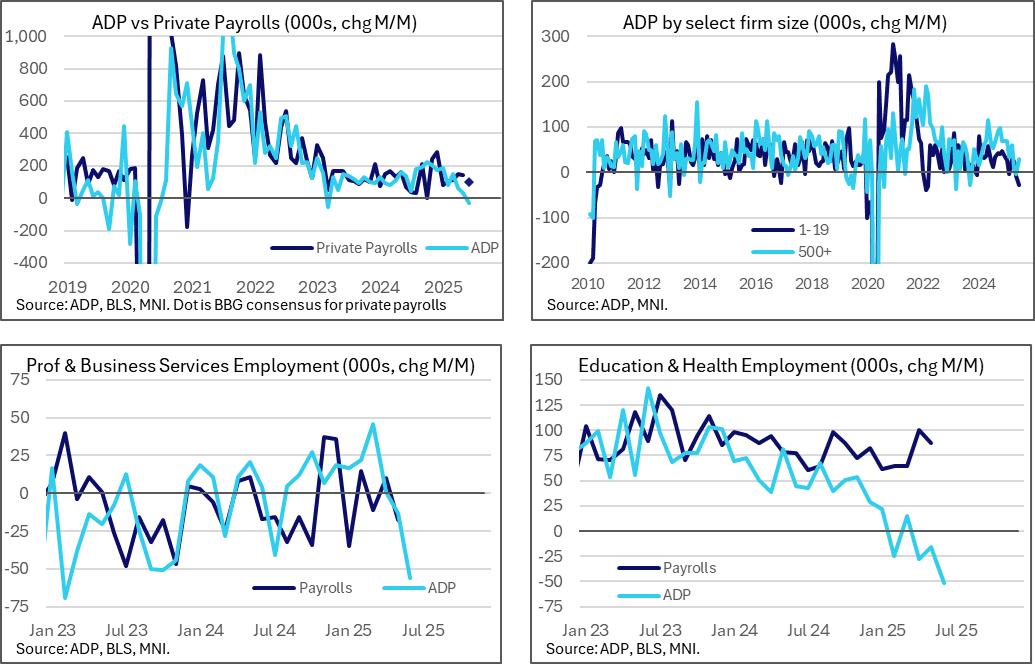

US DATA: A Large Miss For ADP As Slowing Trend Escalates

ADP employment surprisingly fell in June as it continued a trend of clear moderation in recent months compared to what has been a steadier trend for private payrolls up to May ahead of tomorrow’s NFP release. Declines were led by two sectors in particular, one of which has had a strangely weak relationship with BLS payrolls, but it’s still a soft report no matter how you look at it.

- ADP private sector employment was much weaker than expected in June as it fell -33k (sa, cons 98k) along with last month’s soft print confirmed with a downward revision to 29k vs the initial 37k.

- The decline was led by professional & business services (-56k after -13k, its sharpest decline since Feb 2023) and education & health services (-52k after -16k, its sharpest decline since Jul 2020).

- The typically cyclically insensitive education & health services component is showing an increasingly puzzling disconnect with NFP industry data although the weakness in professional & business is more concerning from a direct readthrough for tomorrow’s NFP print.

- Financial activities rounded out the third sector with net job losses in June, -14k for its first decline since Sep 2024 and its largest decline since Dec 2022.

- To the upside, leisure & hospitality continued to fare well, rising 32k after 43k and showing no sign of reduced discretionary demand in those sectors.

- There isn’t a clear-cut story for job losses by firm size although the very smallest did suffer the most. Those with 1-19 employees saw -29k after -8k, 20-49 employees saw -18k after -5k and 250-499 -27k after -7k, whilst those with 50-249 saw +12k after +53k and 500+ +30k after -4k.

- The -29k drop in those with 1-19 employees is the sharpest since Mar 2022.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US: MNI POLITICAL RISK - Senate Starts Work On Big Beautiful Bill

Download Full Report Here

- President Donald Trump will meet Vice President JD Vance for lunch.

- White House officials expect a call between Trump and Chinese President Xi Jinping “very soon,” as both countries accuse the other of violating May's tariff truce.

- OMB Director Russell Vought will receive a hostile reception from Democrats when he delivers testimony to the Senate Appropriations Committee on Wednesday.

- Trump announced he will double the tariff rate on steel and aluminium imports to 50%, starting on Wednesday. The European Commission said it "is prepared to impose countermeasures".

- Commerce Secretary Howard Lutnick said “tariffs are not going away”, and noted: "We could sign lots of [trade] deals now," but "we’re trying to make them better...”

- The legal argument the US Supreme Court used to block swathes of former President Biden’s agenda could be used to block Trump's 'Liberation Day' tariffs.

- The Senate comes back into session this evening to start modifying the Republican tax megabill. Senate Majority Leader John Thune (R-SD) wants the bill on Trump’s desk by July 4, but some Senators are questioning that deadline.

- There is little hope for a breakthrough as a second round of Ukraine-Russia talks gets underway. Without progress, more pressure will build on Trump to authorise a punitive package of sanctions.

- Iran is expected to reject a US nuclear proposal.

- Poll of the Day: Trump’s three weakest issues are all linked to the economy.

Full Article: US DAILY BRIEF

EUROPEAN INFLATION: Analysts Continue to Centre on 2.0% Y/Y May Headline HICP

Updated analyst tracking estimates point to only slight downside risks to consensus for tomorrow's May release of Eurozone flash HICP (10:00 BST). The median estimate we've seen over the weekend of 2.0% Y/Y matches the broader Bloomberg consensus although with a few looking for a 1.9% print. MNI's tracker eyes 1.9%.

- Citi see headline 1.9% ("albeit with risks of 2.0%"), core 2.4% as national-level data came in in line with their original Eurozone aggregate forecast.

- HSBC see headline at 1.9%, core 2.4% (cutoff appears to have been ahead of the Spain and Germany results).

- Goldman Sachs see 1.95% headline, 2.37% core after German, Italian and Spanish data.

- Barclays see headline 1.96% Y/Y and core 2.43%.

- ING see headline at 2.0%, core 2.5%.

- Lloyds see headline at 2.0%, 2.4%

- Morgan Stanley see headline at 2.0%, core 2.4% "forecast revision today is probably largely attributable to airfares, but, most likely, the non-volatile components of services inflation remained relatively sticky"

- Société Générale see headline 2.0% ("risk of a slightly weaker print"), core 2.4% "most of the easing in May is likely to come from this Easter effect unwinding"

- TD Securities see headline 2.0%, core 2.4% as they "have seen disinflation continue across major member states in May".

Ahead of the EZ-wide release, the Netherlands will be the last key national-level print, scheduled for tomorrow 05:30 BST, and is expected for a 0.3pp deceleration to 3.8% Y/Y. Remember that in April, the Netherlands saw an outsized 0.7pp 'beat' in headline at 4.1%, which was driven by services inflation speeding up by 1.6pp vs March.

EGB OPTIONS: Option Package in Buxl, Bund, Bobl, Schatz

- DUU5 107.30p, sold at 21.5 in 6.75k

- DUU5 107.20p, sold at 17.5 in 6.75k.

- UBU5 119.00p, sold at 280 in 500.

vs

- RXU5 130.00p, bought for 115 in 2k.

- OEU5 117.75p, bought for 64.5 in 4k.