MEXICO: March Trade Balance Data, USDMXN Continues Upward Trajectory

Apr-27 11:03

- USDMXN continues to trade with underlying bid tone, after touching a fresh short-term high of 20.4856 on Monday.

- A double bottom reversal pattern has been confirmed on the daily chart, reinforcing a short-term bull theme. Attention is on the 50.0% Fibonacci retracement of the Mar-Apr range, at 20.5975.

- Clearance of this level would open 20.8028, the 61.8% retracement. Key support has been defined at 19.7274, the Apr 4 low.

- Just released: *Mexico March Trade Surplus $198.72M; Est. -$130.0M (BBG)

- Mexico Mar Imports +12.7% On Year To $51.8B

- Mexico Mar Exports +20.9% On Year To $52.0B

- The U.S. Supreme Court questioned President Joe Biden’s effort to rescind his predecessor’s “remain in Mexico” policy, which has forced tens of thousands of asylum-seekers to stay south of the border while their applications are processed.

- 10am Mexico City time: Banxico will hold a swap auction to extend maturities on government securities

- Mexico’s Health Ministry said it will release data on Covid-19 cases and deaths on Friday, April 29, and from then on weekly on Fridays, switching from a daily release.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

LIBOR: JAPAN FIX - 28/03/22

Mar-28 10:59

- 1M -0.06375 0

- 3M -0.00521 0.00165

- 6M 0.04330 0

LIBOR: US FIX - 28/03/22

Mar-28 10:58

- US00O/N 0.32786 0.00129

- US0001M 0.44943 0.00429

- US0003M 0.99629 0.01343

- US0006M 1.49271 0.04157

- US0012M 2.19886 0.11015

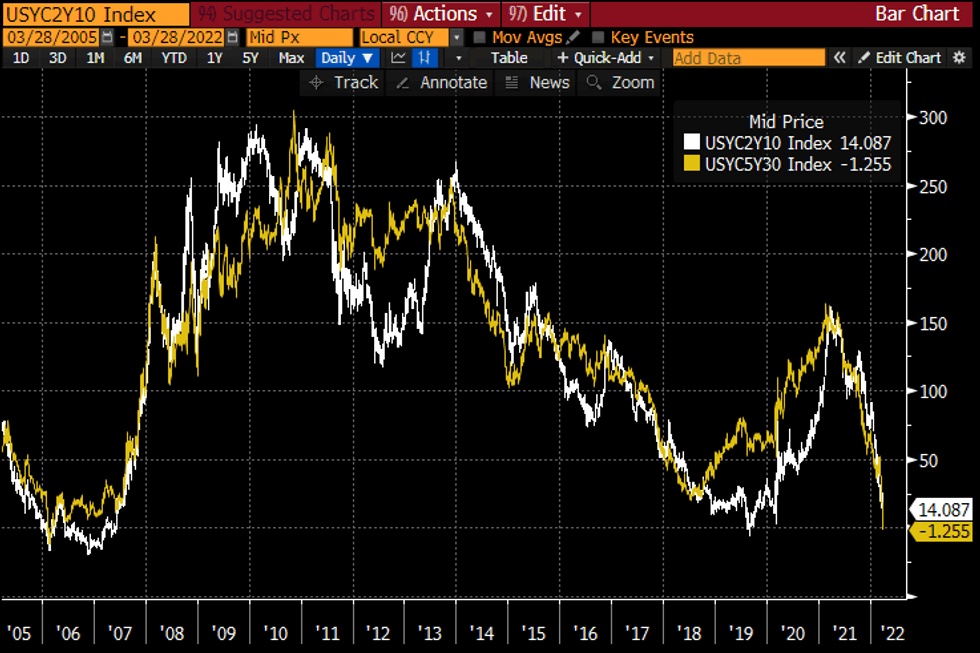

US TSYS: First Inversion In 5s30s Since 2006

Mar-28 10:53

- Cash Tsy yields are off earlier highs but have still seen a sizeable bear flattening, driving the curve to new recent flats and in the case of 5s30s, the first inversion since 2006.

- A two-stage lockdown in Shanghai and the further inflationary pressure this could have helped drive the overnight sell-off, only partially reversed by Russia downplaying the chances of Putin and Zelensky meeting, noting a lack of progress in talks and noting Biden’s statements on Putin as being alarming.

- 2YY +7.1bps at 2.340%, 5YY +5.1bps at 2.596%, 10YY +1.5bps at 2.488%, 30YY +0.3bps at 2.588%.

- TYM2 sits 4 ticks lower on the day at 121-13+, but off an earlier low of 120-30+ which now forms first support just above 120-28, the continuation of the Dec 26, 2018 low. Volumes are solid for the day as a whole but have slowed down in recent trading.

- Data: Second tier data releases with wholesale & retail inventories, the advance goods trade balance and Dallas Fed manufacturing activity.

- Bond issuance: US Tsy $50B 2Y Note auction (1130ET) and US Tsy $51B 5Y Note auction (1300ET)

- Bill issuance: US Tsy $57B 13W, $48B 26W bill auctions (1130ET)

US 2s10s and 5s30s Tsy curvesSource: Bloomberg

US 2s10s and 5s30s Tsy curvesSource: Bloomberg