MNI US Macro Weekly: Risk-Off Before Data Resumes In Earnest

Feb-27 18:38By: Chris Harrison and 1 more...

US+ 3

Download Full Report Here

Executive Summary

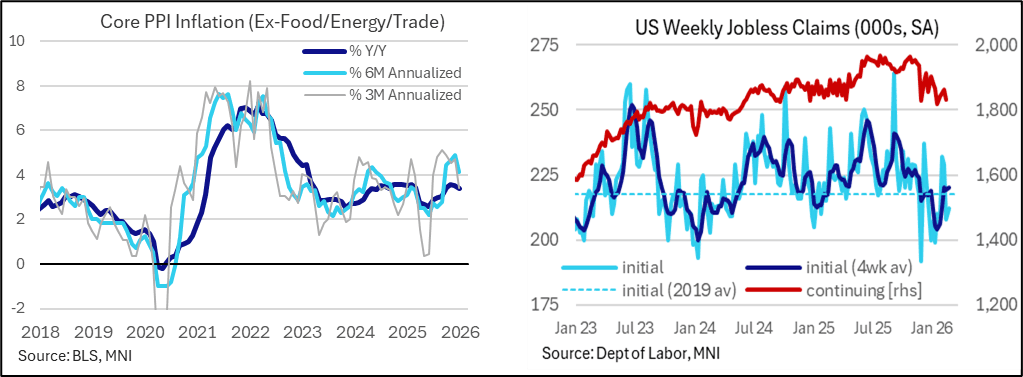

- PPI inflation was stronger than expected at a headline level in January but core PPI was in line with M/M expectations for January alone and a little softer after factoring in downward revisions. Still, core input cost pressures clearly remain elevated despite a slightly softer print.

- Weekly labor indicators were solid by recent standards for both ADP and jobless claims, although the Conference Board’s labor differential continues to point to a trend increase in the u/e rate.

- Business surveys were mixed although the MNI Chicago PMI in February extended what was a particularly sharp increase in January before surprise ISM manufacturing strength.

- 10% tariffs under Section 122 came into effect on Tuesday, with President Trump’s weekend threat of 15% tariffs not being made into a formal order but supposedly still being in the pipeline. Effective tariff rates should only be slightly smaller to those under the previous IEEPA-heavy regime, assuming they're set at 15%, although the Section 122 tariffs can only be in place for 150 days before needing Congressional approval to extend.

- In Fedspeak, Governor Waller (voter, dove) currently sees the March rate decision as a coin toss that will depend on upcoming February data, firmly in contrast to Fed Funds futures pricing just 1.5bp of cuts.

- Governor Cook (voter) meanwhile added to various official comments fearing a scenario in which monetary policy would be unable to address structural job losses under AI displacement if there is a rise in the natural rate of unemployment.

- Rates markets are ending the week at their most dovish but still only price a cumulative 15bp of cuts for the June FOMC decision having mid-week touched their most hawkish levels in months.

- The next cut is fully priced for July (25bp) whilst a combination of geopolitical risks, private credit exposure and AI bubble fears weigh further out on the rate path, with 60bp of cuts to year-end and a SOFR terminal yield of sub-3.00% set for its lowest close since November.

- After a quieter week for data, next week sees ISM manufacturing and services surveys before February nonfarm payrolls and January retail sales reports both at 0830ET on Friday.

- These are some important updates before the March 17-18 FOMC meeting with its new SEP, with further notable releases the following week including CPI for February (Mar 11) and PCE for January (Mar 13).