MNI US Macro Weekly: IEEPA's Dead, But Tariffs Will Live On

Feb-20 21:10By: Tim Cooper and 1 more...

US+ 1

Download Full Report Here

EXECUTIVE SUMMARY

- Friday’s announcement of the US Supreme Court decision to strike down the White House’s International Emergency Economic Powers Act (IEEPA) tariffs overshadowed the week’s data and Fed developments.

- Even if the court’s decision wasn’t entirely shocking (prediction markets indicated only a 25% probability that the court would uphold the tariffs), it left open questions over whether and when tariff refunds will be paid, and potential impacts on existing trade deals negotiated under the auspices of IEEPA.

- One thing that does seem clear is that the sudden drop in tariff rates will be reversed at least partially, muting the longer-run macro impact. The administration was quick to announce a global 10% tariff via Section 122 authority with Section 232 and 301 tariffs to remain and be expanded over time. Treasury Secretary Bessent said that this approach would result in “virtually unchanged tariff revenue in 2026”.

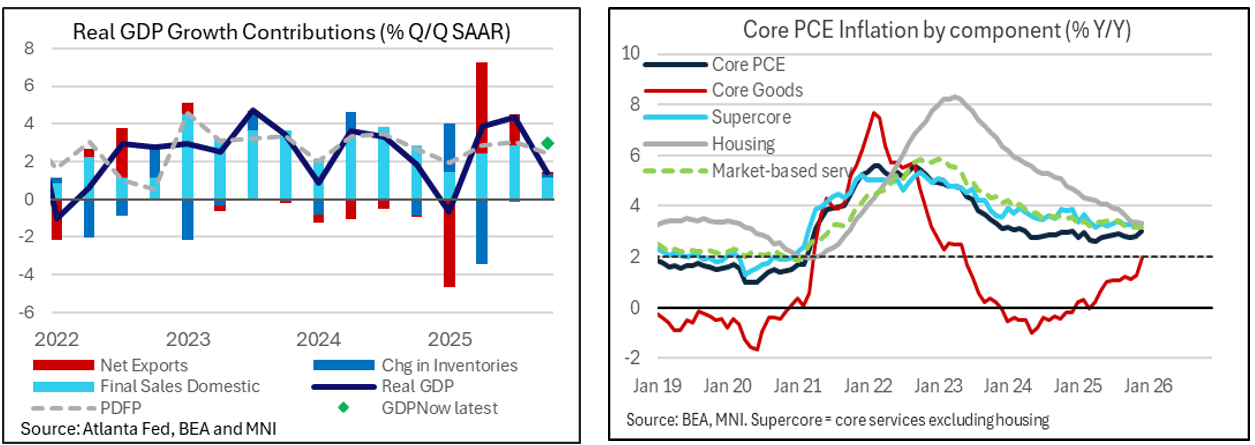

- Elsewhere, real GDP surprised much lower than expected at 1.4% annualized (cons 2.8) in the Q4 advance release after 4.4% in Q3, although the government sector weighed heavily owing to the shutdown and a very strong deflator. Private demand metrics were close to expectations with PDFP at 2.35%.

- Core PCE inflation was in line with unrounded expectations in the delayed December report at 0.355% M/M whilst it ended the year at 3.0% Y/Y (highest since Apr 2024). Core goods inflation accelerated to 2.0% Y/Y (highest since May 2023) whilst supercore PCE inflation at 3.3% Y/Y saw zero disinflationary progress compared to the 3.3% averaged across 2025.

- Second tier data saw some sizeable strength with core durable goods accelerating in a positive sign of business investment and with industrial production growth regaining traction and broadening out.

- Labor data saw some sequential improvements as well, with weekly ADP rising an average 10.25k per week for its fastest since late November and initial jobless claims surprised notably lower.

- Business sentiment indicators were more mixed however, including the flash PMIs for February slipping with the manufacturing index at a seven-month low and services at a ten-month low. It came against a backdrop of strong input and selling cost inflation.

- The December trade deficit surprised higher on a pullback in gold net exports. Tech-led capital goods imports continue to surge but are offset by consumer and industrial goods in tariff front-running payback.

- The FOMC minutes had a hawkish addition with “several” members wanted to keep open the possibility that the next Fed rate move could be a hike, not necessarily a cut.

- Gov. Miran meanwhile pared back his rate cut view, seeing a need for 100bp vs 150bp of cuts this year.

- Near-term, last week’s NFP-driven hawkish shift has extended further this week, with just 15bp of cuts priced for the June FOMC. There is however still a cumulative 56bp of cuts to year-end and terminal yields are at still the dovish end of recent ranges.

Next week sees data focus on the delayed January PPI for both broader input cost pressures after a strong December update plus the usual PCE readthrough following strong tracking after January CPI.

Next week sees data focus on the delayed January PPI for both broader input cost pressures after a strong December update plus the usual PCE readthrough following strong tracking after January CPI.