MNI US Macro Weekly: Activity Hums While Labor Market Stutters

Jan-09 20:42By: Tim Cooper and 1 more...

US+ 1

Download Full Report Here

EXECUTIVE SUMMARY

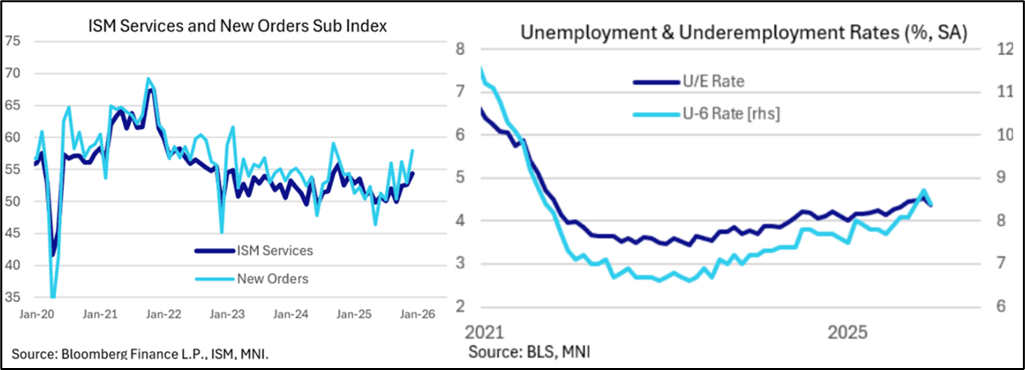

- Jobs growth may have disappointed in December’s Employment Situation report, but the drop in the unemployment rate saw near-term rate FOMC cut prospects trimmed further (January cut = no chance) after hawkish shifts throughout the week.

- A next Fed cut is still fully priced for June, only just at 25.5bp, the first meeting under a new Chair.

- Most labor market data remains concerning but activity is still robust, not least because recent productivity growth was shown this week to be stronger than expected. Additionally while manufacturing activity remains moribund, December's ISM Services report was meaningfully stronger than expected, with the headline PMI index surprisingly jumping to a 14-month high.

- A 5+% real GDP handle in Q4 as implied by the Atlanta Fed tracker may be misleadingly high due to distorted October trade data, but domestic final demand looks to have been roughly as strong at the end of the year as it was through its resilient middle.

- The top-tier data schedule carries on Tuesday with the December CPI report amid a broader set of inflation prints, including delayed October and November PPI data (Wednesday) and Import/Export Prices for November (Thursday).

- Also due to garner attention is the “advance” retail sales report which is likewise on the slightly stale side, being only for November (alternative measures of retail activity have signalled a solid end-of-year). And we should also mention a possible Supreme Court ruling on Wednesday on the legality of the White House’s IEEPA tariffs.

- Consumer price inflation is set to pick up on a sequential basis from November's suspiciously weak price prints, with early consensus pointing to 0.3 to 0.4% M/M rises in both headline and core CPI after an average increase of 0.1% M/M over November and October.

- However, continued data distortions including “payback” effects mean that an inflation acceleration in December shouldn't be taken at face value (more in our week-ahead section) and is unlikely to settle any debates within the FOMC on the outlook for price pressures.