MNI US Employment Insight: U/E Rate Improves But Payrolls Soft

Jan-09 21:14By: Chris Harrison and 1 more...

Employment+ 4

Download Full Report Here

Executive Summary: Lower U/E Rate Counters Tepid Jobs, Quality Concerns Linger

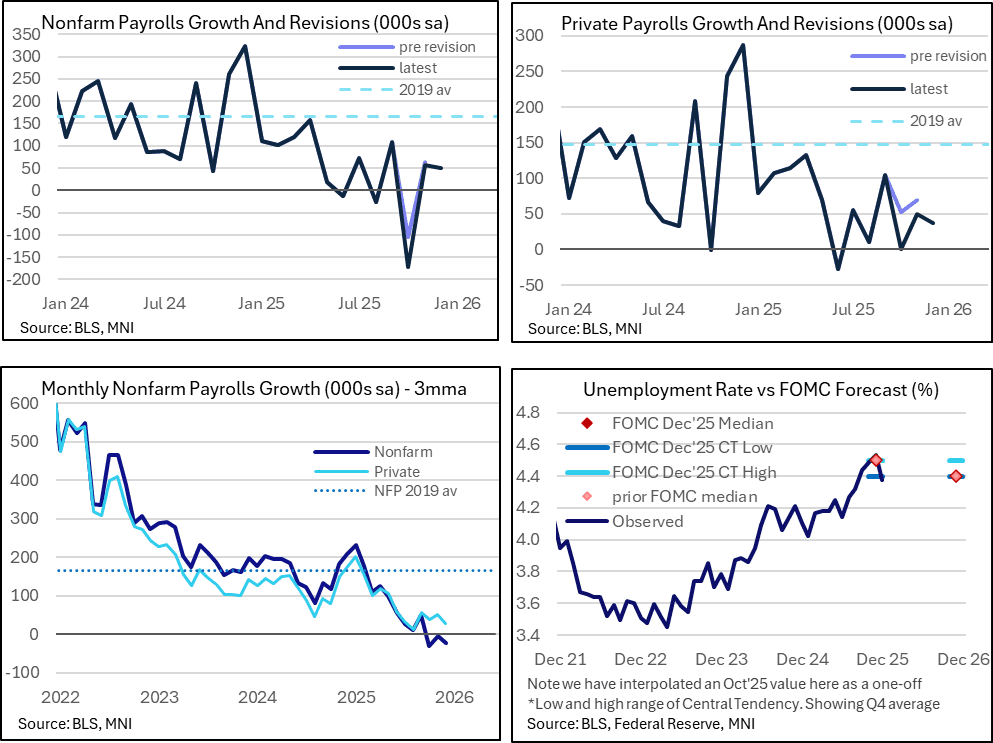

- Nonfarm payrolls growth was softer than expected in Dec at 50k (cons 70k) and with a larger downward surprise for private payrolls at 37k (cons 75k).

- The solid two-month downward revisions (-76k for NFP) were concentrated back in Oct (-68k) and driven by the private sector with -70k of which -51k was in Oct.

- Colder than usual early December weather likely weighed although we suspect the impact is modest.

- The household survey meanwhile showed several signs of improvement from November's, even if that largely just reversed some weakness seen on survey- and government-shutdown related distortions.

- The unemployment rate fell back to 4.375% in Dec after a downward revised 4.54% in Nov (initially 4.56% with rounded figures on screens exaggerating the move) and 4.49% in Oct (initial 4.50). Seasonal adjustment factors were updated in annual revisions covering the past five years.

- The u/e rate averaged 4.47% in Q4 (using an interpolated value for Oct) to match the 4.5% the median FOMC participant forecast in the Dec SEP. Seven FOMC members had looked for 4.6-4.7% across Q4.

- AHE growth was on the solid side but growth of 3.8% Y/Y and 4.0% annualized in Q4 won’t trouble the Fed from a unit labor cost angle with productivity still increasing rapidly.

- Data quality concerns are still elevated though, particularly with the household survey response rate barely increasing from November’s record low.

- Jobs growth may have disappointed but the drop in the u/e rate saw near-term rate FOMC cut prospects trimmed further after hawkish shifts throughout the week on data and oil prices. It sees a cumulative 12.5bp of cuts priced for Apr vs 14.5bp pre NFP and 18.5bp prior to Wednesday’s strong ISM services report. A next cut is still fully priced for June, only just at 25.5bp, the first meeting under a new Fed Chair.