MNI Eurozone Inflation Preview – January 2026

Jan-28 10:14By: Moritz Arold and 1 more...

Inflation+ 1

Price Resets and Idiosyncratic Factors To Shape January Report

- The Eurozone January flash inflation round is split across two weeks. Germany and Spain are scheduled to release data on Friday January 30, with France due Tuesday February 3 and Italy, the Netherlands, and the Eurozone aggregate following on Wednesday February 4. The release will be an important input ahead of the ECB's February 5 decision. While the bar to a near-term rate change in either direction remains high, the data will inform assessments of the balance of risks for 2026.

- Headline inflation is expected to decelerate to 1.7% Y/Y (vs 1.9% prior). Across categories, analysts expect energy HICP to ease materially to around -4.5% Y/Y (from -1.9% in December). This will primarily be driven by base effects following January 2025's strong 3.0% M/M print, but some idiosyncratic factors are also at play.

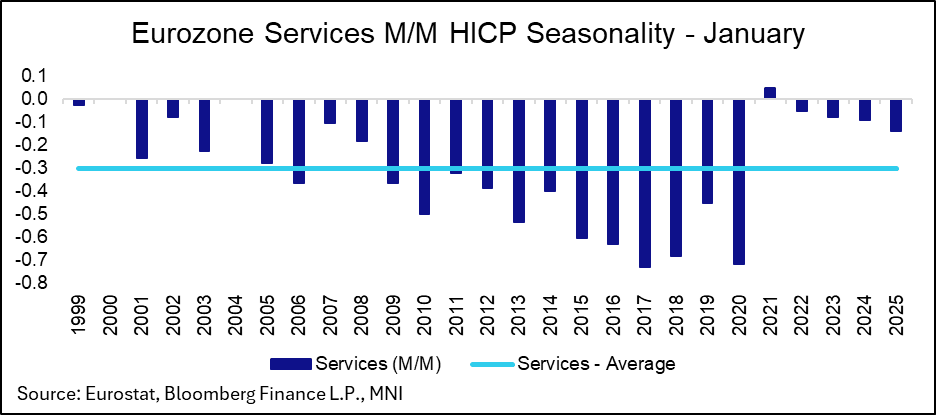

- Core inflation is seen roughly stable to marginally lower at 2.2% Y/Y, with a small expected uptick in core goods not enough to offset a deceleration in services. Food, alcohol and tobacco is expected to see little changes around 2.5% Y/Y with no major seasonal effects beyond normal January patterns.

- There is more uncertainty than usual surrounding the January release due to several idiosyncratic factors.