MNI US Macro Weekly: Data Leaves Fed On Sidelines For Summer

Jul-18 19:26By: Tim Cooper and 1 more...

Federal Reserve+ 1

Download Full Report Here

Executive Summary

- June’s inflation and economic activity readings didn’t settle the debate over the ongoing and eventual impact of tariffs, very likely leaving the Fed on the sidelines through the summer.

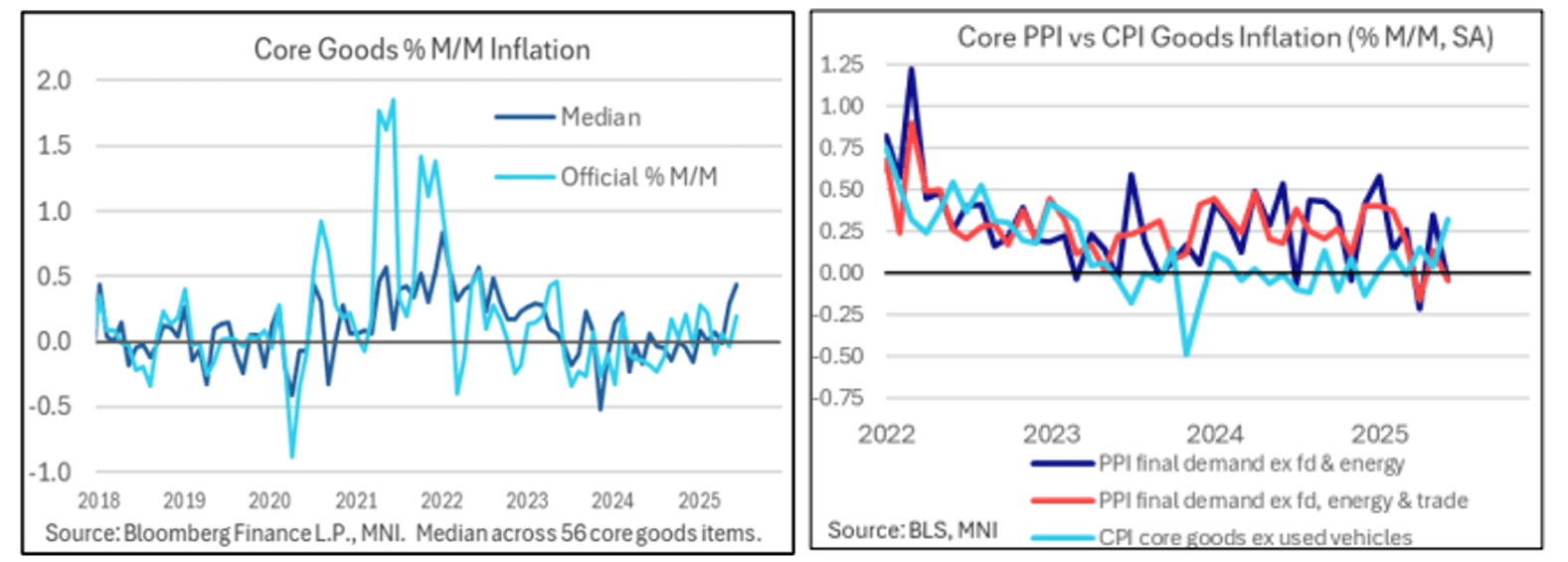

- Core CPI picked up vs May but was softer than expected, with services inflation remaining tame. But core goods prices jumped, with a pickup in key categories suggesting that tariff passthrough is underway.

- Producer and import price aggregates were on the soft side as well, but a closer read of the data showed potential pressures building, with exporters not appearing to offer discounts to offset tariffs for US buyers.

- Gov Waller continued to make his case for a rate cut on July 30th, citing the transitory nature of tariff-driven inflation and fearing falling behind the easing curve given downside risks to the labor market.

- He may be supported by Gov Bowman - but the vast majority of the Committee – including Collins, Hammack, Kugler, and Williams this week – support maintaining a restrictive stance in the meantime.

- The FOMC majority is unlikely to be swayed to a July cut by this week’s data. Growth is tracking above 2% in Q2, with various data this week suggesting that the economy ended the quarter stronger than it began.

- In particular, retail sales picked up strongly in June after a weak run, with initial jobless claims declining for a 5th week and industrial production stabilizing.

- The Fed’s Beige Book noted a pickup in activity from late May, while noting that the biggest price increases are yet to come. Meanwhile, regional Fed manufacturing/services surveys and the University of Michigan consumer survey pointed to a continued improvement in sentiment in July as tariff uncertainty abated.

- There was Fed drama outside of the rate cut debate too, with the biggest market moves of the week coming Wednesday on reports (later denied) that President Trump was planning to fire Chair Powell soon.

- For all that, near-term Fed Funds implied rates closed only a little higher on the week, slightly more hawkish than pre-CPI levels. July is still seen as a non-event from a rate decision perspective (1bp priced) with a cumulative 16bp for the Sept FOMC and 46bp for December.

- There were however larger declines for implied rates into 2H26 and beyond on the assumption that a new Fed Chair after Powell’s term expires in May 2026 will be more overtly dovish.

- The data calendar gets quieter next week, with highlights including flash July PMIs and durable goods orders, while the pre-FOMC blackout period means we won’t get any monetary policy commentary.