EU CREDIT UPDATE: EUR Market Wrap

- Bunds are 3-5bp tighter with 2y/10y yields at 2.04%/2.32% - DM team flagged second round impacts from equity weakness in China & Europe, coupled with some USD demand in FX trade, seem to factor into the latest round of bond buying.

- Main/XO are -1.1bp/-5bp at 56.6bp/308bp while €IG looks -0.5bp on average. No supply but primary is showing signs of waking with a 2Y Sr Pref FRN mandate from LBBW. €IG curve movers include ERFFP (up to 5bp wider), ENXFP (4-5 tighter).

- SXXP is flat at 508pts while SPX futures are +1.0%. €IG's biggest risers/fallers include Vestas Wind Systems A/S (+6%), Neste Oyj (+4%), Ireland Group PLC (-4%), BPER Banca SPA (-4%).

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

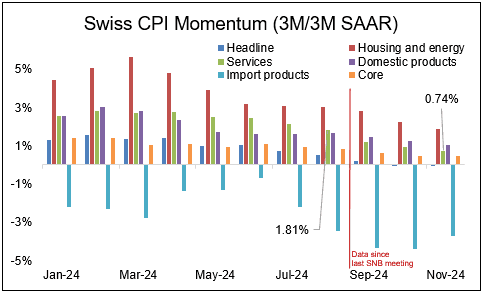

EUROPEAN INFLATION: Swiss SA Data Shows Broader Momentum Deceleration

Swiss inflation data shows a clear trend lower in seasonally-adjusted momentum on services and domestic categories, with the 3M/3M SAAR measure for services calculated by MNI standing at 0.7% as of November vs 1.8% as of August (the latest release before the last SNB policy meeting).

- Barring an uptick in momentum, this should also result in lower yearly rates on services / core inflation in the coming months.

- For the broader core measure, momentum (3M/3M SAAR) stands at 0.5% as of November, compared to 0.8% as of August. Domestic inflation momentum meanwhile is 1.1% now vs 1.7% in August.

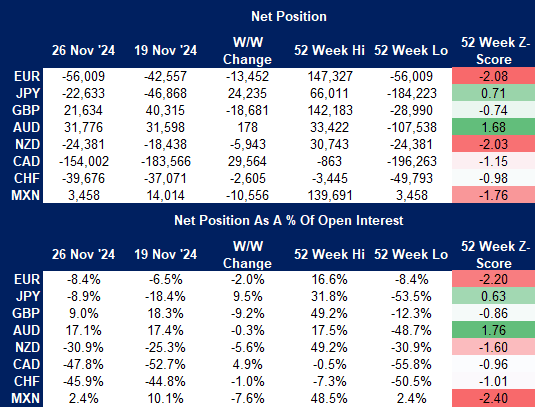

CFTC: JPY Net Position Improves Further, Near Neutral Pre-BoJ

- The JPY net short position reduced further, halving to 9% of open interest to represent a 9.5% swing in the net position. This underpins the current positive momentum seen across JPY futures, with the positioning Z-score rising to +0.63, the second highest among the currencies surveyed.

- The rising net position coincides with USD/JPY's decline from ~154.50 to ~Y153.00 and the extension of that sell-off below Y150.00 will likely mean the realtime position is back to near-neutral well ahead of the BoJ's last decision of the year - at which markets remain evenly split between unchanged, and a 25bps rate hike.

- In contrast to the improving JPY position, markets cut exposure to GBP, with the net long reduced by 18.6k contracts to +9.0% of open interest.

- Lastly, the MXN net position was cut further, hitting a new 52w low of 3.4k contracts, or 2.4% of open interest. This presses the positioning Z-score to -2.40 points, the lowest among all currencies surveyed and pointing to increased downside momentum for MXN. The survey period captures the USD/MXN rally from 20.11 to 20.65.

Full dataset here:

US TSYS: Early SOFR/Treasury Option Roundup

SOFR and Treasury options still favoring downside puts overnight despite the short end rebound following Fed Gov Waller's dovish comments - leaning toward rate cut on Dec 18. Underlying futures mixed, curves twisting steeper as short end rates outperform. Projected rate cuts into early 2025 after surging late Monday following Fed Gov Waller's comments, current levels vs. late Monday (*) : Dec'24 cumulative -18.1bp (-20.0bp), Jan'25 -23.5bp (-24.3bp), Mar'25 -36.9bp (-37.5bp), May'25 -45.9bp (-45.5bp).

- SOFR Options

- 2,600 SFRH5 95.50/95.62 put spds vs. 95.75/95.87 call spds

- 2,000 SFRF5 96.00/96.25/96.50 2x3x1 call flys ref 95.795

- Block, 3,000 SFRG5 95.62/95.75/95.87 put flys, 2.25

- 2,000 SFRG5 95.56/95.75/95.87 broken put flys ref 95.785

- Treasury Options

- 3,000 TYF5 115 calls, 1 ref 110-31.5

- over 3,200 TYF5 112 calls, mostly 21

- over 11,000 TYF5 109/110 3x1 put spds, 1.5 net ref 111-00