RUSSIA: Zelenskiy Says Ukraine Won’t Cede Donbas Region to Russia

- Ukrainian President Volodymyr Zelenskiy said he won’t cede the eastern region of Donbas to Russia and pushed for Kyiv to be included in Friday’s talks, Bloomberg report. Putin is demanding that Ukraine give up the Donetsk and Luhansk regions that together form Donbas as a condition to unlock a ceasefire and enter negotiations over a longer-term peace accord.

- Vedomosti report that the upcoming talks between Trump and Putin could lead to temporary volatility for the ruble's exchange rate. If sanctions are eased and foreign investors return to Russia, the ruble could strengthen, but this scenario remains unlikely, according to “experts” cited by the newspaper.

- Modest progress with the possibility of further contacts will not have a major impact on the currency, but a negative outcome could lead to tighter sanctions. Meanwhile, internal factors could also push the ruble down to 85-90 rubles/$1 by the end of the year, the newspaper add.

- The Federal Statistics Service reports July inflation data and 2Q GDP data at 17:00BST/19:00 local time. Yesterday, Putin said at a meeting on economic issues shown on state television that Russian inflation slowed to 8.8% y/y as of end July from 9.4% at the end of June.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US INFLATION: [RPT] CPI Seen Picking Up In June, Core Goods Eyed

Note: Our full CPI preview will be released later today.

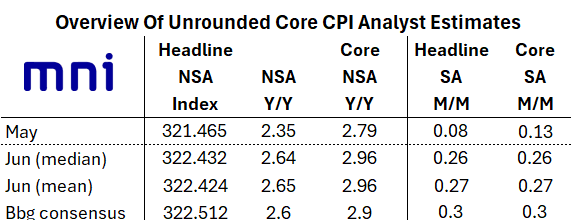

June CPI is the highlight of next week's US data slate, with MNI's early roundup of analyst expectations showing an anticipated acceleration in the main measures of inflation. Both core and headline CPI are seen rising to the mid 0.20s% M/M, from May's readings of 0.13% for core and 0.08% for headline.

- Such outturns would mean the strongest M/M headline CPI since January, with core continuing to range between 0.0-0.3% for a 5th consecutive month. They would also bring the Y/Y core reading to 2.9% or 3.0%, with headline at 2.6% or 2.7% (both would be 4-month highs).

- The first area of focus will be on core goods prices, with the impact of import tariffs expected to become more acute as the summer progresses: core goods are seen up from May's flat M/M reading to closer to 0.2%, with tariff-sensitive categories such as apparel and recreational goods seeing a pickup, offset by a drag from used vehicles.

- Core services are seen picking up modestly from 0.2% M/M in May to closer to 0.3%, with May's relatively tame housing inflation steady-to-higher. "Supercore" (core services ex-housing) is expected to rise from May's surprisingly low sub-0.1% M/M print to closer to 0.3%, as airfares and medical care services prices regain traction.

- It's unlikely that a downside surprise would persuade the Federal Reserve to seriously consider cutting rates in July, given the expected pickup in tariff-related prices in coming months, but it would certainly help lay the groundwork for a resumption of easing in September.

GILTS: Curve Steepens, Front End Supported By Bailey & REC

Futures top out at 91.85 before threatening a break below Friday’s low.

- Contract last 91.75.

- Bears remain in technical control and eye the July 8 low (91.42). Conversely, bulls initially need to clear the July 10 high (92.19).

- Little in the way of tangible impact from BoE Governor Bailey’s dovish comments and a soft REC labour market report further out the curve, although they do feed through into STIRs and the front end of the gilt curve.

- Yields -3bp to +1bp, curve twist steepens.

- Month-to-date ranges intact across the major benchmark yields

- 2s10s registers the highest level since April, 78.9bp, and is on track to register the highest close of ’25. The April 9 high (84.6bp) provides the next major upside target.

- 5s30s trades back above 140bp, with the ’25 intraday high (147.2bp) providing the next upside area of interest.

- GBP STIRs around pre-gilt open levels. SONIA futures flat to +3.0, while BoE-dated OIS shows ~54bp of cuts through year-end.

- The Mansion House event, as well as CPI & Labour market data, headline this week’s UK calendar. Please see our earlier STIR bullet/Global Week Ahead email for greater colour on those events.

US-RUSSIA: Trump Expected To Announce UKR Weapons Package, Endorse RU Sanctions

10:00 ET 15:00 BST: President Donald Trump will hold a (closed press) White House meeting with NATO SecGen Mark Rutte, where he is expected to finalise a new plan to arm Ukraine “that is expected to include offensive weapons,” per Axios. Later today, Trump is expected to make a 'major statement' on Russia. No timing has been released.

- Axios reports the plan is likely to include long-range missiles that could reach targets "deep inside Russian territory” a “major shift for Trump, who had until recently [said] he would provide only defensive weapons to avoid [escalation].”

- Politico reported the weapons package "numbers in the hundreds of millions”, and “could come from the fund approved by [Biden] that lets the DOD give weapons from the U.S. military stockpile...”

- Trump's 'major statement' is also likely to include preliminary approval of Senator Lindsay Graham's (R-SC) punitive sanctions/tariffs bill, reworked to provide Trump full discretion over implementation.

- Graham said on X: “.... A turning point is coming.” He told Axios: "Trump is really pis--- at Putin. His announcement tomorrow is going to be very aggressive."

- Senate Majority Leader John Thune (R-SD) indicated the bill will hit the Senate next week. House Speaker Mike Johnson (R-LA) endorsed the bill, putting it on a track to Trump’s desk.

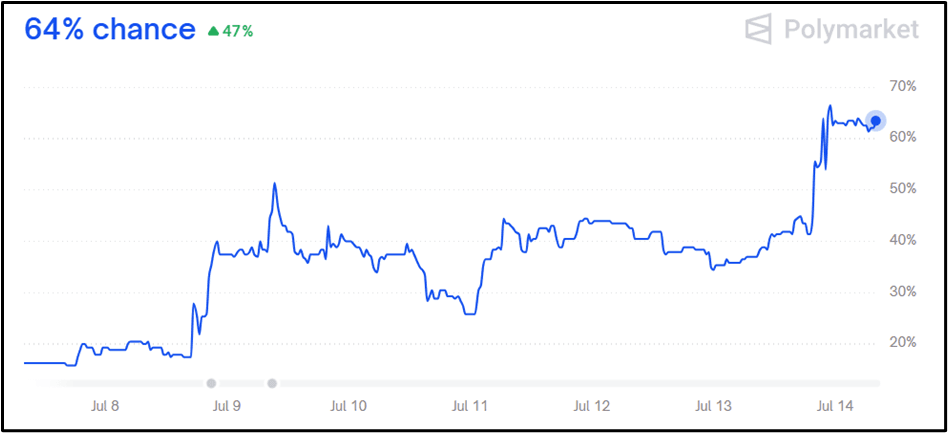

- Polymarket sees a 64% chance Trump increases Russia sanctions before August, a significant spike since last week.

Figure 1: Trump increase sanctions on Russia before August?

Source: Polymarket