ENERGY: Zelenskiy Says Talks Open Path to Peace

“ZELENSKIY SAYS VITAL PUTIN-TRUMP SUMMIT OPENS UP PATH TOWARDS JUST PEACE, SUBSTANTIVE THREE-WAY DISCUSSION BETWEEN LEADERS OF UKRAINE, UNITED STATES AND RUSSIAN WE ARE COUNTING ON U.S” - rtrs

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

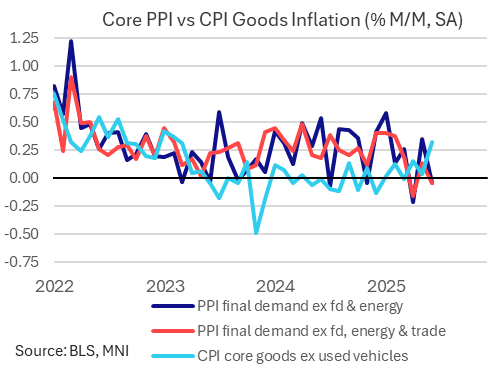

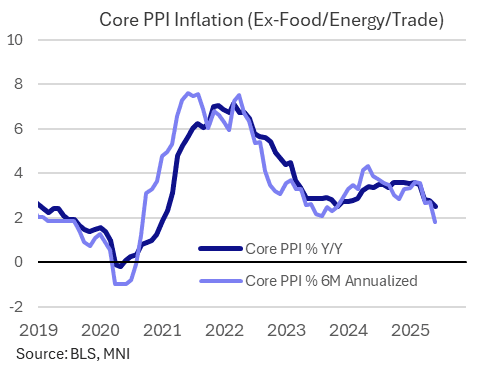

US DATA: PPI Suggests Tariffed Pipeline Price Pressures Less Acute Than Feared

The June Producer Price Index report was roundly softer than expected - and certainly than feared given the context of rising tariffs - despite some upward revisions to prior. While core goods prices did indeed advance, the rise was consistent with the increases seen over the last 6 months rather than a sudden surge.

- The main headline reading was flat PPI % M/M (0.01% unrounded), vs expectations of a 0.2% rise (though this was offset by an upward revision to May, to 0.30% from 0.13%). That left Y/Y PPI at the softest level (2.3%) since September 2024, and down from 2.7% in May. Ex-food and energy final demand inflation unexpectedly fell, by 0.04% M/M (+0.2% was expected), though again May's upward revision must be considered (0.35%, upward rev from 0.14%).

- The core ex-food/energy/trade services reading though was negative for the 2nd month in 3, with only a modest upward rev, coming in at -0.05% M/M (+0.2% expected), with May revised up only marginally (+0.14% from +0.05%). This core category is now deflating for the first time on a 3M annualized basis since June 2020, with the 6M rate slowing to 1.8%, softest since September 2020 - suggesting momentum is waning, not increasing.

- Final demand goods rose by 0.3% M/M - the biggest rise since February - driven by core (ex-food and energy) goods rising 0.3%, with final demand energy and food rising 0.6% and 0.2% respectively. There was some potential tariff-related price hikes here, with communication and related equipment prices rising 0.8% M/M.

- But the core goods reading remained within the 0.2-0.3% M/M range that has prevailed in every month of 2025 so far, so there is not yet clear evidence that tariffs are having an outsized effect in this category. Finished consumer goods ex-food and energy actually saw inflation dip slightly, to 0.2% M/M from 0.3% in the 2 prior months, though core durables remained elevated at 0.4% vs 0.1% nondurables.

- This offset a 0.1% decrease in final demand services, though this was largely for travel services - traveler accommodation services fell 4.1% M/M and as noted earlier, passenger airfares fell 2.7% (after falling 0.9% in May).

- Trade services was a drag on PPI in June (-0.04%), there was a strong upward revision to 1.12% from 0.44% for May that appears to account for most of the prior revision, and this is a category that is not just volatile, but largely imputed from trade margins as opposed to a market-based price.

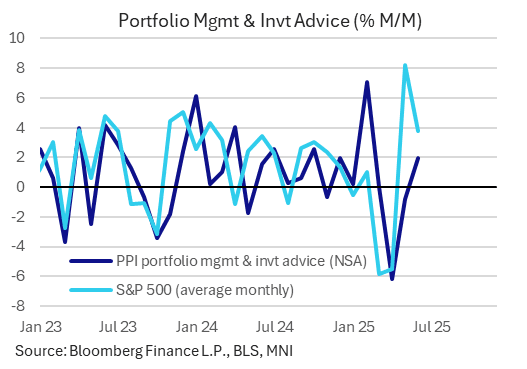

US DATA: PPI Portfolio Services Lift With More Likely To Come

Adding to the above on what looks like roughly a neutral contribution to core PCE from PPI details at first glance.

- Portfolio-related costs look somewhat in the ballpark of limited expectations we'd seen.

- Portfolio management & investment advice: 1.9% M/M in June after an unrevised -0.8% M/M in May.

Within that, portfolio management increased 2.2% after -0.9%. - Citi had eyed 2.5% for portfolio mgmt whilst Nomura had looked for 4.3% for the broader portfolio & invt advice.

STIR: Modest Dovish Move In Fed Pricing On PPI, Hawkish CPI Move Briefly Unwound

Fed pricing little changed to a touch more dovish in the wake of the softer-than-expected PPI data, which comes on the heels of yesterday’s CPI reading.

- Our macro team notes that the PPI reading screens neutral to a little dovish for PCE.

- A reminder that the CPI data pointed to tariff pressures across several core goods categories.

- FOMC-dated OIS shows 0.5bp of easing for this month, 14.5bp through September, 28bp through October and 45bp through year-end. Levels little changed to 1.5bp more dovish vs. pre-data levels.

- The hawkish repricing that followed yesterday’s CPI was retraced at one stage, before the initial post-PPI dovish move faded a little.

- SOFR-implied terminal rate pricing moves to ~3.25% vs. 3.28% pre-data.