WTI TECHS: (Z5) Trades Through The 50-Day EMA

- RES 4: $67.68 - High Jul 30

- RES 3: $65.77/68.43 - High Sep 26 and key resistance

- RES 2: $62.34 - High Oct 8

- RES 1: $62.12 - Intraday high

- PRICE: $61.59 @ 14:51 BST Oct 23

- SUP 1: $55.96 - Low Oct 20

- SUP 2: $54.85 - Low May 5

- SUP 3: $54.16 - Low Apr 9 and a key support

- SUP 4: $53.23 - 1.764 proj of the Jul 30 - Aug 13 - Sep 26 price swing

The latest recovery in WTI futures appears corrective for now, however, note that price has traded through resistance at the 50-day EMA, at $61.08. The breach of this average signal scope for a stronger recovery and exposes $62.34 next, the Oct 8 high. Clearance of this level would expose key resistance at $65.77, the Sep 26 high. Key support and the bear trigger has been defined at $55.96, the Low Oct 20.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

STIR: J.P.Morgan Recommend Jun/Dec '26 SEK FRA Flatteners

J.P.Morgan recommend entering Jun26/Dec26 SEK FRA curve flatteners as they believe that “some easing bias, despite current Riksbank’s forecast, will likely get priced into the money market curve over the coming weeks/months”

- They go on to note that their baseline “is for the Riksbank to be on-hold over the coming quarters. This should be supportive of carry trading, especially at the front-end of the curve where yields are expected to stay in a tight range. The relationship between money market curves and outright yield has been weak recently but we believe that this relationship with strengthen over the coming weeks/months with the curve expected to exhibit a strong positive directionality versus yields; flatteners will behave essentially like low-beta bullish duration proxies, in our view”.

SONIA OPTIONS: Ratio Put Spread seller

SFIM6 96.15/96.00ps 1x2 sold the 1 at half and 0.25 in 3.75k.

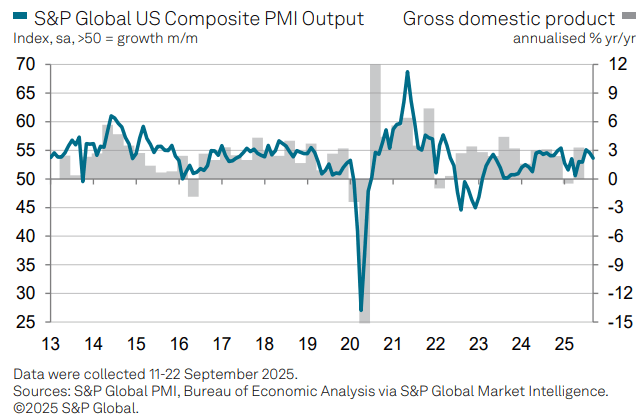

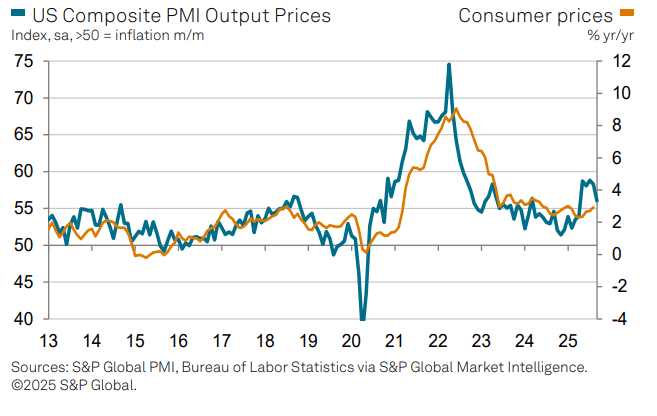

US DATA: Flash PMIs Point To Moderation In Q3 Expansion

September's flash US PMIs brought a 2-month low for Manufacturing at 52.0 (52.2 consensus, 53.0 prior) and a 3-month low for Services at 53.9 (54.0 consensus, 54.5 prior), but both readings were pretty much in line with consensus and suggest an economy in expansionary territory (consistent with 2.2% Q/Q annualized GDP expansion in Q3, per the S&P Global report).

Highlights from the report:

- "US business activity growth slowed for a second successive month in September, according to early ‘flash’ PMI data, accompanied by a softening of demand growth. While growth was again seen across both manufacturing and service sectors, both categories reported weakened expansions, leading to slower hiring in both cases."

- "Tariffs were meanwhile again widely cited as the main cause of sharply higher costs, but weaker demand and stiff competition reportedly limited the scope to raise selling prices, which rose on average at the slowest rate since April. Slower than expected sales reportedly also contributed to the largest rise in factory inventory levels of unsold stock in the history of the survey.

- "More encouragingly, business confidence in the outlook improved, partly reflecting hopes that lower interest rates will help offset some of the anticipated impacts from tariffs and broader policy uncertainty."

- On labor market conditions: "Employment rose for a seventh straight month in September, though the rate of job creation slowed. Lower job gains were seen across both manufacturing and service sectors. Although service companies continued to take on extra staff in response to rising workloads and improved confidence, the September survey saw a higher incidence of companies unable or unwilling to fill vacant positions. In manufacturing, the survey saw more of a focus on job losses due to cost cutting."

- Inflationary pressures remained hot but have been tempered a little, and this is of note from a tariff passthrough perspective: "Firms across both manufacturing and services often reported difficulties passing higher costs on to customers due to weak demand and growing competition. Goods price inflation cooled especially sharply, down to its lowest since January whilst selling prices in the service sector rose at the weakest rate since April."