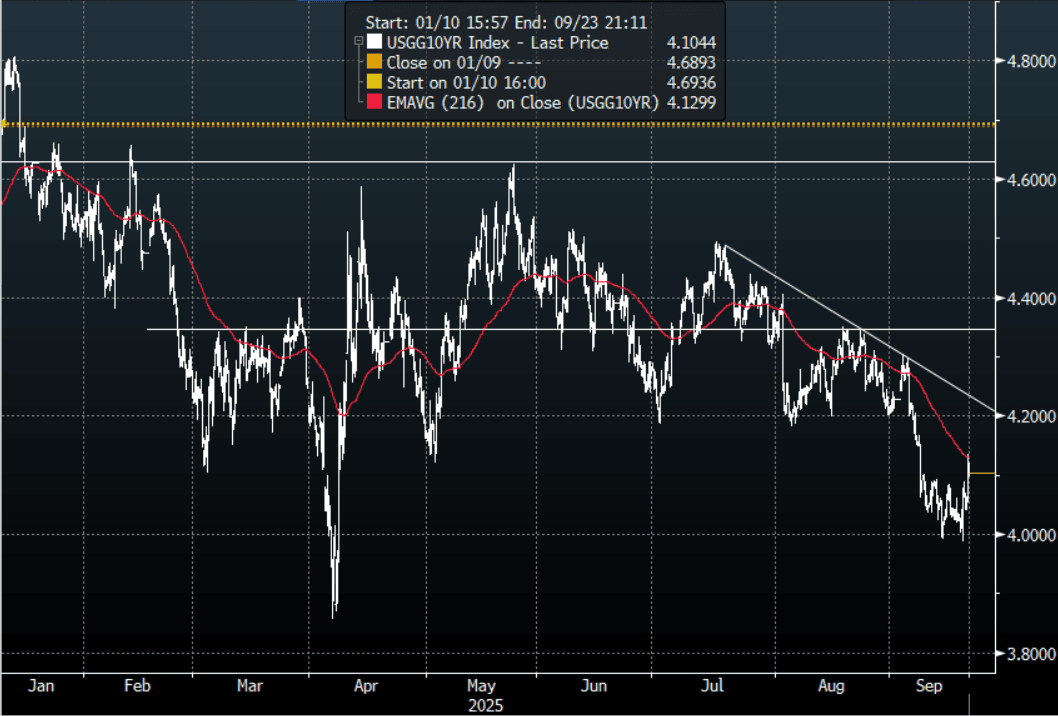

US TSYS: Yields Retrace Higher, Led By The Long-End

TYZ5 reopens at 111-31, down 0-00+ from closing levels in today’s Asia-Pac session.

- Overnight the US 10-year yield had a range of 4.0412% - 4.1352%, closing around 4.104%.

- Treasury yields retraced higher overnight; led by the long-end causing the yield curve to steepen(2s10s +0.69 at 53.885, 5s30s +2.54 at 105.953).

- 10-Year Yields could not extend below 4.00% and have bounced as the Fed could not meet the markets very dovish expectations. The first buy-zone is now back towards the 4.15%/4.20% area where I suspect demand should return initially. A sustained break through 4.00% is needed for the focus to then turn towards the 3.80% area.

- MNI US DATA: Initial Jobless Claims Surprise Lower, Texas Fraud Still Seems Apparent. Initial jobless claims were lower than expected at 231k (sa, cons 240k) in the week to Sep 13, a payrolls reference week. It follows a marginally upward revised 264k (initial 263k) in what was a much higher than expected print at the time after a spike in Texas initial claims in what has since been revealed as linked to ID fraud that has increased since Labor Day.

- MNI US DATA: Continuing Claims See A Fourth Consecutive Weekly Decline. Continuing claims meanwhile also offer a relatively encouraging report, easing to 1920k (sa, cons 1950k) in the week to Sep 6 after yet another downward revision to 1927k (initial 1939k). It marks a fourth consecutive weekly decline for continuing claims from 1961k in the week to Aug 9, taking it further away from the recent high of 1968k in late July.

Fig 1: 10-Year US Yield 2H Chart

Source: MNI - Market News/Bloomberg Finance L.P

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US TSYS: Yields Retrace Lower, Led By The Long-End

TYU5 reopens at 111-24, down 0-00+ from closing levels in today’s Asia-Pac session.

- Overnight the US 10-year yield had a range of 4.2965% - 4.3433%, closing around 4.306%.

- Treasury yields retraced lower overnight; led by the long-end which saw the yield curve flatten(2s10s -1.24 at 55.610, 5s30s -0.28 at 108.242).

- (Bloomberg) --“As the market readies for Powell’s speech at Jackson Hole, we’ll argue that the biggest risk for Treasuries is if the Fed Chief chooses to throw cold water on the widely anticipated September rate cut,” Ian Lyngen, head of US rates strategy at BMO Capital Markets, said in a note.”

- MNI US DATA: Building Permits Downtrend Continues. Housing starts and building permits data for July offered firmly conflicting signs of housing activity, but with the less weather-sensitive permits series pointing to a clearer downtrend that chimes more closely with dour NAHB homebuilder sentiment.

- Yields are still firmly within its wider 4.10%-4.65% range. The 4.35% pivot area in 10-Year yields found solid demand overnight helped by the S&P rating, the market will now be waiting for any clues from Powell's upcoming Jackson Hole speech.

Fig 1: 10-Year US Yield 2H Chart

Source: MNI - Market News/Bloomberg Finance L.P

OIL: US Crude & Gasoline Stocks Fall Last Week

Bloomberg reported that there was a US crude inventory draw of 2.4mn barrels last week, more than offsetting last week’s 1.5mn build, but with only 100k at Cushing. Gasoline stocks fell 1mn barrels but distillate rose 500k, according to people familiar with the API data. The official data is out on Wednesday.

AUSSIE 3-YEAR TECHS: (U5) Holding Bulk of Rally

- RES 3: 97.190 - High May 5 2023

- RES 2: 96.932 - 76.4% of Mar-Nov ‘23 bear leg

- RES 1: 96.860 - High Apr 07

- PRICE: 96.580 @ 15:46 BST Aug 19

- SUP 1: 95.900 - Low Jan 14

- SUP 2: 95.760 - Low 14 Nov ‘24

- SUP 3: 95.480 - Low Jan 11 2023 and a major support

Aussie 3-yr futures gapped sharply higher on the back of the recent soft US NFP data, and last week’s CPI print should also prove supportive. Recent price action has narrowed the gap with resistance at 96.730, the Sep 17 ‘24 high, leaving 96.860 as the next key level. Any continuation lower would instead strengthen a bearish theme. This would refocus attention on 95.760, the 14 Nov ‘24 low. Conversely, a reversal higher would refocus attention on 96.860, the Apr 7 high.