US TSYS: Yields Play Catchup on Weak ADP, Futures Muted

Most major US bond futures finished Wednesday's trading day around flat as cash played catch up after a day out. The US 10-Yr TYZ5 declined -01 to 113-00, just north of the 20-day EMA of 112-30. TYZ5 has opened in Asia trading down -01 at 112-31

Cash was busy with a strong rally across the curve by 2-4.7bps with the 10-Yr the outperformer. Data releases are still delayed but with plenty of FedSpeak soundbites. The bid to cover on the US$42bn 10-Yr new issue declined from the prior 10-Yr auction. A $25 billion 30-year bond auction Thursday is the next focus whilst shutdown discussions continue.

- The US 2-Yr declined -2.1bps to 3.57%

- The US 5-Yr is down -4.2% to 3.673%

- The 10-Yr fell -4.7bps to 4.071%

- The 30-Yr declined -4.1bps to 4.666%

- Federal Reserve Bank of Boston President Susan Collins said Wednesday she supports holding interest rates steady for some time, in part so officials can assess some of the effects of the easing since September. "Given my baseline outlook, it will likely be appropriate to keep policy rates at the current level for some time to balance the inflation and employment risks in this highly uncertain environment," she said. (source MNI Brief)

- The Federal Reserve will return to buying assets to keep pace with demand for currency and other liabilities before too long, and policymakers will decide the ultimate composition of those purchases, Roberto Perli, manager of the System Open Market Account at the New York Fed, said Wednesday. (source MNI Brief)

- MNI BRIEF: Fed Repo Facility Will Cap Rate Pressures- Williams: The Federal Reserve standing repo facility will effectively cap temporary upward pressure on money market rates as long as primary dealers and banks use it, New York Fed President John Williams said Wednesday, also repeating the Fed is assessing market indicators to decide when to begin gradual expansion of its balance sheet.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

MNI: UK BRC SEP BY VALUE SHOP SALES LFL +2.0% Y/Y, TOTAL +2.3% Y/Y

- MNI: UK BRC SEP BY VALUE SHOP SALES LFL +2.0% Y/Y, TOTAL +2.3% Y/Y

UK DATA: Retail Sales Slow Amid Budget Caution, Still Boosted By Food Inflation

BRC Retail Sales data for September posted a 2.3% Y/Y increase, a slowdown from the 3.1% of August, and marginally above the 12-month average of 2.1%. However, it is important to note that the monitor is a value measure and a large proportion of the increase is likely due to inflation.

- Food sales (the largest contributor) slowed slightly versus August, growing 4.3% Y/Y (vs 4.7% Aug), though the press release notes that "growth in food sales was largely inflationary rather than volume growth".

- Non-food sales weakened, increasing 0.7% Y/Y (vs 1.8% Aug), below the 12-month average of 0.9%. The figure was propped up by strong electrical sales, from the release of the new iPhone and Apple Watch, and strong furniture sales.

- Planning spending around high inflation and a "potentially taxing Budget" ahead of the Christmas period is highlighted as a notable downward driver by the BRC.

- Note that ONS's retail sales volume index sees the September data released on 24 October, following a 0.5% M/M rise in August. The in the BRC report covers the same 5 weeks as the ONS report (from 31 August - 5 October 2025).

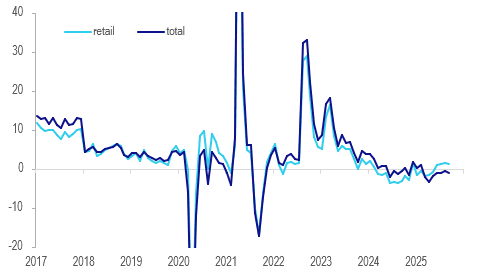

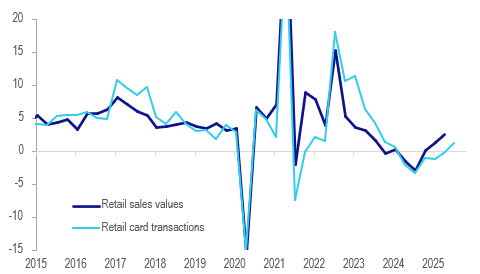

NEW ZEALAND: Q3 Retail Spend Up On Quarter But Still Soft Consistent With Easing

September retail card transactions fell 0.5% m/m after rising 0.6%, the first negative after three consecutive increases. Annual growth slowed to an anaemic 1.2% y/y signalling that while consumption is off its lows the recovery remains weak making additional RBNZ rate cuts more likely. The extent of further easing including in early 2026 remains highly data dependent though.

NZ retail spending y/y%

Source: MNI - Market News/LSEG

- Despite the soft end to Q3, the quarter saw a 0.6% q/q increase in nominal retail spending driven by consumables (+1.0%), hospitality (+1.4%) and motor vehicles (+2.7%). Q3 retail sales volumes are released 27 November. They rose 0.5% q/q & 2.3% y/y in Q2.

- Total expenditure was down 0.4% m/m in September after rising 0.4% to still be down 1% y/y. The total was up 0.7% q/q in Q3.

- Core retail spending fell 0.4% m/m in September but rose 0.7% q/q in Q3. The September decline was broad based with all the major categories falling except hospitality (+1.5% m/m). Motor vehicles sank 2.6% but consumables were down 0.5%, durables -0.8% and apparel -1.4%.

- Services fell 1% m/m while non-retail spending ex services was flat (includes healthcare but also travel).

NZ card expenditure y/y%