US TSYS: Yields Lower on Profit Taking; 20-Yr Auction Wednesday Key

In a morning highlighted by low volumes, the US 10-Yr bond future is up just 01+ to 108-24+ having t...

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

CROSS ASSET: Risk Sentiment Off Earlier Lows As US/Iran Developments Eyed

Risk sentiment is comfortably away from earlier Asia Pac lows, as markets await further developments around the US/Iran conflict. US equity futures have pared losses back to around 0.50% for Eminis (we opened down around 0.9%). Likewise for the USD, which is still up modestly for the session, but comfortably off earlier highs. AUD/USD got to lows of 0.7117, but is now back to 0.7150. Oil futures remain +5% higher, but Brent was last near $94.75/bbl, after touching $97.50/bbl in the first part of trade.

- Market price action still appears to be trading conflict risks with a glass is half full approach, i.e. we are still closer to the end of the conflict rather than significant further escalation.

- Near term focus will likely rest on whether we see further action around the US naval blockade, after the earlier incident of firing and boarding an Iranian ship. Iran officials stated they responded by launching drone attacks against US ships. Further actions of this nature are likely to drive fresh market risk off.

- Beyond that will be focus on whether further talks between both sides take place, with conflicting reports as to whether talks will go ahead. This comes ahead of the 10-day ceasefire period ending on Apr 22.

AUD: Antipodean Update - Both Pare Back Early Losses

The AUD & NZD both opened lower on the Asian open on the back of the failed weekend talks. They have both spent the majority of our morning filling in those gaps and paring back some of those early losses. I suspect though that with the deadline approaching and no deal looking imminent, they could both find sellers on rallies in the short-term at least.

- {AUDUSD Curncy} - 0.7145, -0.38%

- {NZDUSD Curncy} - 0.5875, -0.15%

- {AUDNZD Curncy} - 1.2165, -0.30%

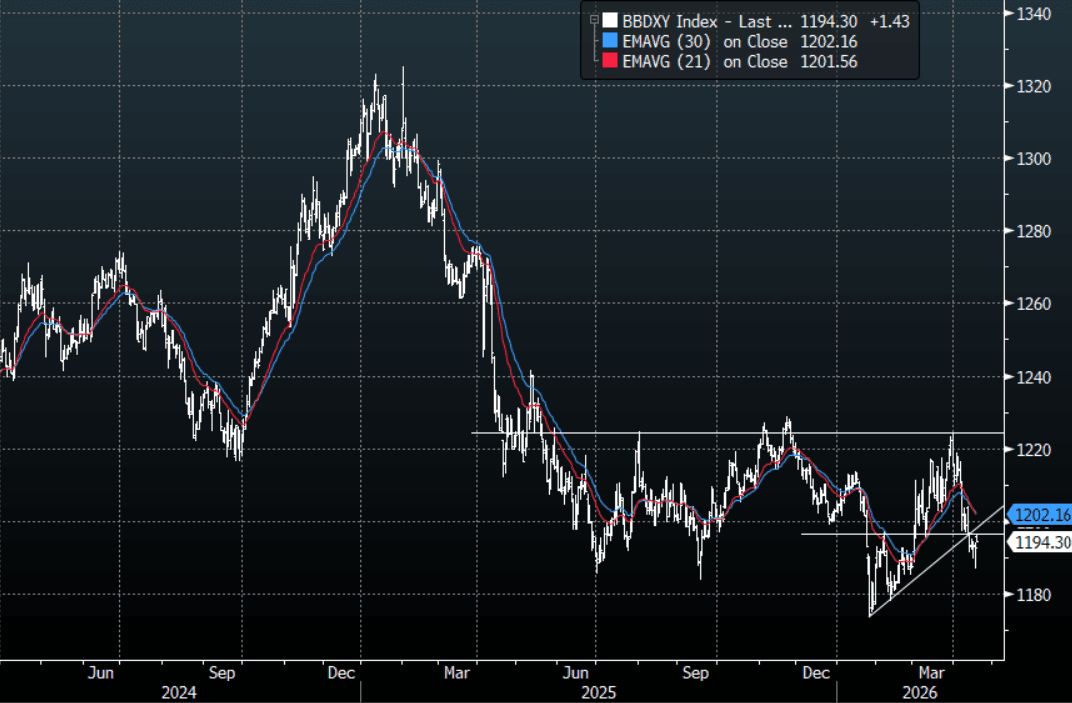

USD: BBDXY - Opens Higher After Friday's Rejection Below 1190

The BBDXY range Friday night was 1186.95-1194.21, Asia is currently trading around 1194. The USD tried to accelerate and build on its break lower on Friday but the move below 1190 was rejected. This morning the USD has opened higher and remains supported as risk pulls back on the failed talks over the weekend. The price action in the USD would potentially concern those bears who added to their risk on this break, they will be hoping for Trump's talk of new imminent talks to be more truthful than his comments on Friday. Reports Iran will not be engaging in them as the deadline approaches will be concerning. The market was trading like a peace deal was already done, should the ceasefire break down at any time and fighting resume I suspect this will all come out the price. On the day, I suspect the USD should now be supported in the short-term on dips as the markets' belief the crisis is over begins to be challenged. The first resistance is back toward 1198-1202, with support seen in the 1187–1190 area.

- WSJ - “Kevin Warsh and the Erosion of the Dollar. Congress needs to acknowledge its error in not preserving the value of America’s currency.” https://www.wsj.com/opinion/kevin-warsh-and-the-erosion-of-the-dollar-8db02a25

- Mohamed A. El-Erian on X: "A warning from the @FT (which has economic, political and social implications): "war in Iran has unleashed a torrent of inflation in the US that economists warn will linger long after the conflict ends, squeezing Americans ahead of November’s midterm elections."

- The BBDXY Average True Range for the last 10 Trading days: 5.75 Points

Fig 1: BBDXY Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P