STIR: Year-Ahead Tightening Expectations Hovering Just Below Cycle High

RBNZ-dated OIS pricing is little changed across meetings today after recent war-induced volatility. ...

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

EUROPE: Viewpoint - Who Is Most Impacted By Oil/Gas Supply Disruption

The market is looking at the disruption to supply of Global Oil/Gas through an optimistic lens at the moment. But who is most at risk should the current malaise be sustained for a longer period than what is currently being priced in. The 2 countries that seem to stick out are Europe and Japan, below are some excerpts from a couple of different financial pundits.

- The Long View(@HayekAndKeynes) wrote an article on his substack: “The 20 Million Barrel Problem. https://hayekandkaynes.substack.com/p/the-20-million-barrel-problem “ The article is definitely worth a read. But for the purposes of the above below is a key excerpt.

- “Europe and Japan: The impact of a supply disruption would not be evenly distributed. Europe consumes roughly 10–11 million barrels per day but produces very little domestically. Including Norway and the UK, European production reaches roughly 4–5 million barrels per day — leaving net imports of 6–7 million barrels per day that must come from elsewhere.”

- “Japan is even more exposed. The country consumes roughly 3.1 million barrels per day and produces almost none of it domestically, making it nearly entirely dependent on imports. For Japan, there is no production buffer and no pipeline alternative. Every barrel arrives by ship. Both economies would face acute pressure quickly in a sustained disruption scenario.”

- Robin Brooks wrote an article on his substack highlighting the same 2 countries because of their high public debt.

- “The spike in oil prices is a symptom of an underlying condition, which is that old alliances are breaking and new ones forming. You really want to have low public debt to make it through this, but Japan and the Euro zone don't. They're in deep trouble...robinjbrooks.substack.com/p/the-lurking- “

- Tracy Shuchart on X: “Natural gas hubs: North America vs Europe ....we are not the same (Bloomberg Maps).” See Graph below.

Fig 1: Natural gas hubs: North America vs Europe

Source: MNI - Market News/Bloomberg Finance L.P/@chigrl

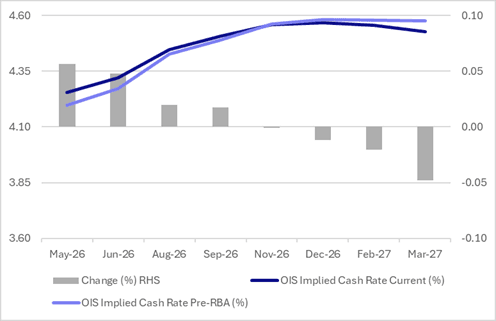

STIR: RBA-dated OIS Firmer For Near Meetings, Softer Further Out

Following yesterday’s RBA policy decision, RBA-dated OIS pricing is 5bps firmer to 5bps softer across meetings.

- MNI RBA Watch - Timing Drove Split Vote, Not Direction- Bullock. Bullock noted rates will need to go higher should inflation prove persistent.

- "RBA Governor Michele Bullock appeared hawkish on inflation during her press conference, saying prices remained too high and the board was worried about second-round effects from higher energy costs." – BBG

- RBA-dated OIS pricing shows tightening across all meetings, with the probability of a 25bp hike rising from 62% in May to 183% by December 2026.

Figure 1: RBA-Dated OIS – Current Vs. Pre-RBA

Source: Bloomberg Finance LP / MNI

JGBS: Bull-Flattener Ahead Of Tomorrow's BOJ Decision, FOMC Later Today

In Tokyo morning trade, JGB futures are stronger, +26 compared to settlement levels, after choppy trading.

- (MTN) “Japan's trade surplus contracted to 57.3 billion yen in February from 559.2 billion yen a year earlier as exports decelerated, provisional data from the Ministry of Finance on Wednesday showed. Exports during the month rose 4.2% to 9.572 trillion yen from 9.19 trillion yen, after shipments to its two largest trading partners, China and the US, fell 10.9% and 8%, respectively.” – via BBG

- Cash US tsys are slightly mixed, with a steepening bias, in today's Asia-Pac session ahead of today’s FOMC policy decision.

- The BOJ is expected to hold rates in March, adopting a cautious stance as the “war in Iran has complicated the BoJ’s outlook,” reversing earlier signals that “the distance to the next rate hike was narrowing.”

- Markets price around a 60% chance of an April hike, but timing remains uncertain (April–July most cited), with decisions hinging on oil prices, yen weakness, wage data, and growth; overall, the BOJ is expected to proceed gradually, balancing inflation risks against growth and financial stability. (See MNI BOJ Preview here)

- Cash JGBs have bull-flattened across benchmarks, with yields 1-5bps lower.

- Swap rates are flat to 2bps lower.

Source: Bloomberg Finance LP / MNI