COMMODITIES: WTI Futures Remain Close to Recent Cycle Highs

A bull cycle in WTI futures remains intact and the latest pullback is - for now - considered corrective. Price has recently traded through $65.99, the Jan 29 high and a bull trigger. The clear break of this level confirms a resumption of the uptrend and opens $68.11, the Jun 23 ‘25 high and the next key resistance. Key support to watch lies at the 50-day EMA, at $62.03. A clear break of this average is required to signal a stronger reversal. Gold traded to a fresh short-term cycle high on Tuesday marking a continued retracement of the Jan 29 - Feb 2 sell-off. The next resistance to monitor is $5314.0, a Fibonacci retracement level. Note that the reversal from the Jan 29 high continues to highlight a potential top in the L/T trend and from a S/T perspective, an unwinding of the overbought condition. A resumption of bearish activity would refocus attention on $4403.0, the Feb 2 low.

- WTI Crude up $1.31 or +2.01% at $66.49

- Natural Gas up $0.03 or +0.99% at $2.849

- Gold spot down $5.94 or -0.11% at $5179.02

- Copper up $10.55 or +1.76% at $611.4

- Silver up $1.41 or +1.59% at $89.689

- Platinum up $78.33 or +3.43% at $2361.52

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

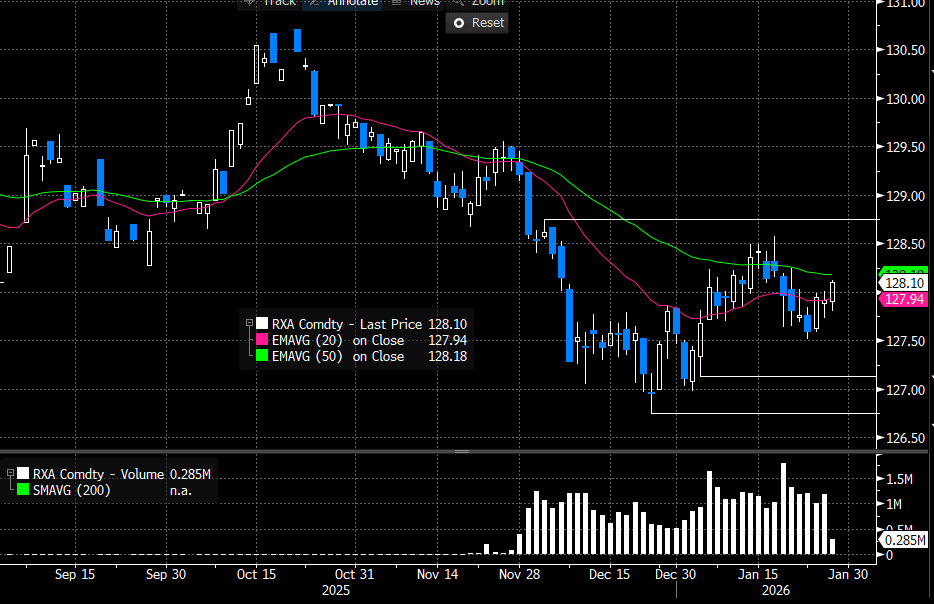

EGBS: German Curve Bull Steepens On Dovish ECB Signals

The German curve has bull steepened following somewhat dovish commentary from ECB’s Kocher and Villeroy this morning. Schatz and Bobl yields are down 3bps, after Kocher suggested to the FT that continued EUR appreciation could create “a certain necessity to react in terms of monetary policy”. Villeroy similarly noted that the exchange rate was one factor guiding policy.

- Note that in the same interview, Kocher stressed that recent EURUSD appreciation has been “modest” and does not necessitate a response for now – we think this aligns with the median Governing Council view.

- 10-year yields are down 2.3bps to 2.85%, though heavy impending supply (E6bln of the 2.90% Feb-36 Bund) is likely containing downside to an extent.

- German 5s30s is +2bps at 104.5bps. The spread has been relatively rangebound since mid-September, with a tighter implied distribution of ECB outcomes coming alongside a more muted-than-expected impact from Dutch pension fund transition flows.

- Bund futures are +17 ticks at 128.09. The trend outlook remains bearish and recent short-term gains are considered corrective. Initial resistance is the 50-day EMA at 128.19.

- 10-year EGB spreads to Bunds are little changed. Portugal will sell OTs at 1030GMT. French PM Lecornu survived two more censure votes yesterday – as expected.

- Broader global focus remains on today's BOC and Fed decisions.

Figure 1: Mar-26 Bund Futures (Source: Bloomberg Finance L.P)

EUROPEAN INFLATION: MNI Eurozone Inflation Preview – January 2025

We've just published our preview of the January Eurozone inflation round - DOWNLOAD FULL REPORT HERE

Price Resets and Idiosyncratic Factors To Shape January Report

- The Eurozone January flash inflation round is split across two weeks. Germany and Spain are scheduled to release data on Friday January 30, with France due Tuesday February 3 and Italy, the Netherlands, and the Eurozone aggregate following on Wednesday February 4. The release will be an important input ahead of the ECB's February 5 decision. While the bar to a near-term rate change in either direction remains high, the data will inform assessments of the balance of risks for 2026.

- Headline inflation is expected to decelerate to 1.7% Y/Y (vs 1.9% prior). Across categories, analysts expect energy HICP to ease materially to around -4.5% Y/Y (from -1.9% in December). This will primarily be driven by base effects following January 2025's strong 3.0% M/M print, but some idiosyncratic factors are also at play.

- Core inflation is seen roughly stable to marginally lower at 2.2% Y/Y, with a small expected uptick in core goods not enough to offset a deceleration in services. Food, alcohol and tobacco is expected to see little changes around 2.5% Y/Y with no major seasonal effects beyond normal January patterns.

- There is more uncertainty than usual surrounding the January release due to several idiosyncratic factors.

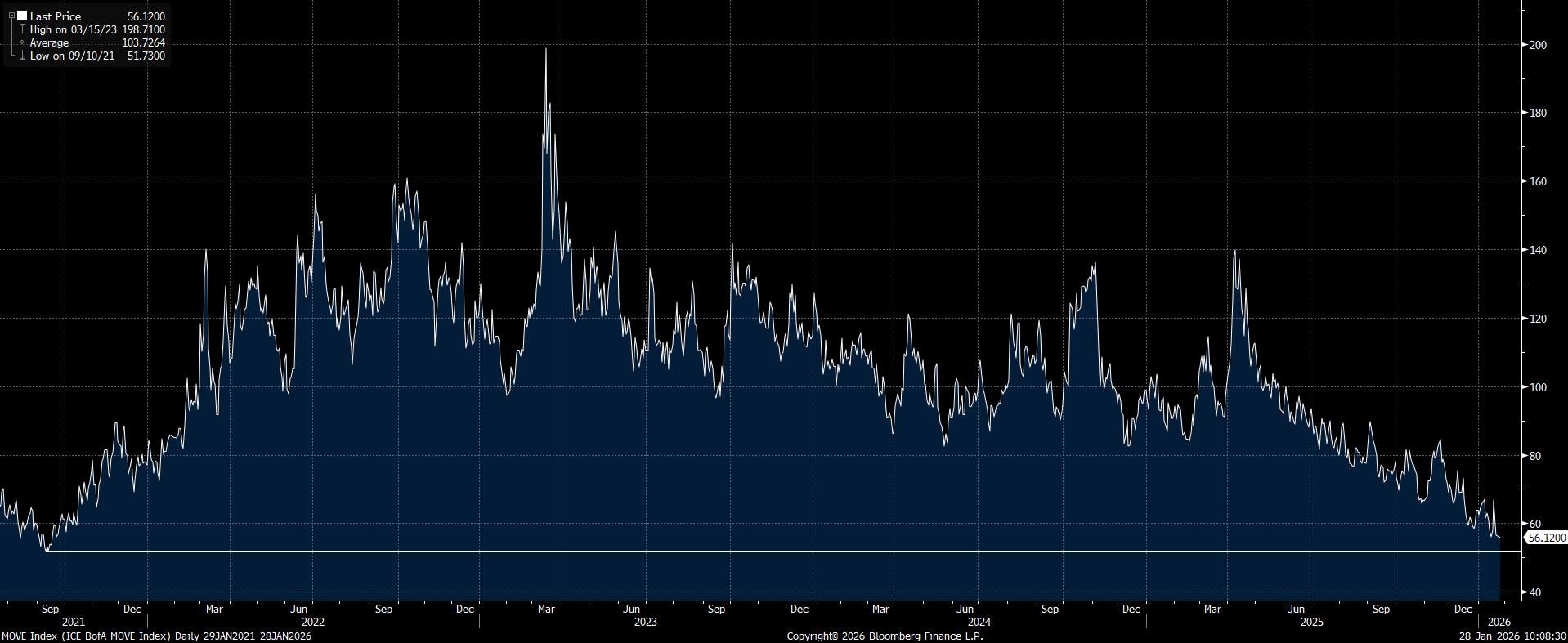

US SWAPTIONS: MOVE Index Holds Near Multi-Year Lows

The ICE-Bank of America MOVE index operates around the lowest level seen since ’21, leaving the steady downtrend witnessed since the ‘Liberation Day’ tariff announcement-induced spike higher in ’25 intact.

- Vol. selling strategies have received greater interest on a multi-year/decade horizon, with the increasing role of policymakers in smoothing market disfunction/stresses, ongoing focus on carry plays and subsequent ‘buy the dip’ mantra across wider markets helping compress vol.

- Assumptions that the Fed is closer to the end of the easing cycle than the start also aid the vol. reduction.

- This theme is evident even with questions about the fiscal sustainability and institutional integrity of the U.S. creating structural pressure for Tsys amid a wider debate surrounding the idea of the ‘sell America’ trade.

- The next downside level of note comes in at the Sep ’21 low (51.73).

Fig. 1: ICE-Bank of America MOVE Index

Source: MNI - Market News/Bloomberg Finance L.P.