GLOBAL: Worsening Outlook Leaves EM Cyclical Stocks Vulnerable

Jun-15 08:46

Executive summary

- Even though selling pressure on LT government bonds remain elevated (i.e. LT bond yields are surging), EM financials have been underperforming the market in recent weeks as global outlook worsens.

- In addition, the fall in China real M1 (in 2021) has been pricing in ‘cheaper’ financials for months.

- Hence, as the global outlook is not about to change anytime soon, the ‘cheap’ EM cyclical sectors may continue to underperform in the near term and defensive allocation should continue to be investors key allocation in the coming months.

Link to full publication:

EM Financials Underperform As Economic Slowdown Accelerates

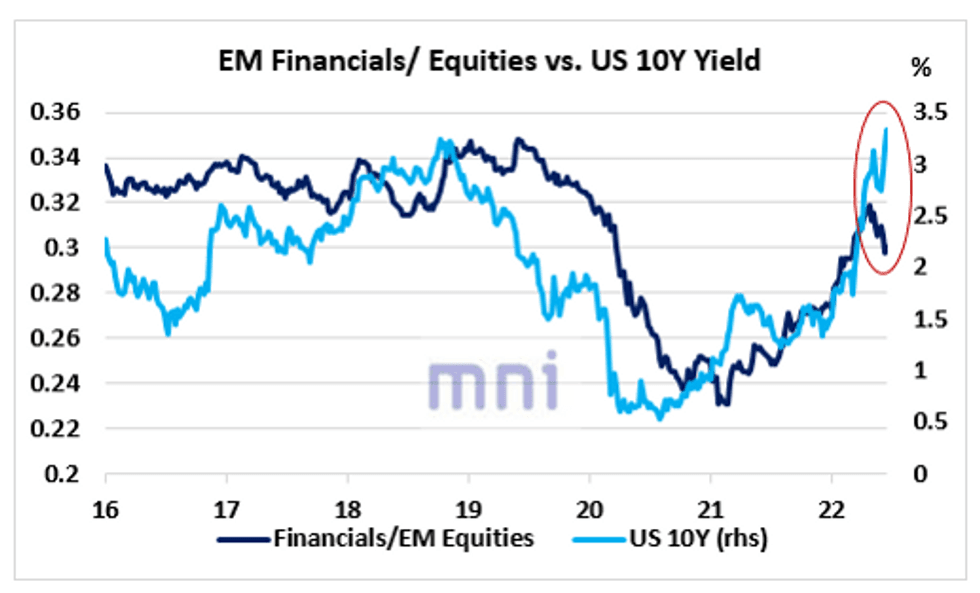

The significant liquidity injections following the Covid shock combined with the surge in ST and LT bond yields had been a strong driver of EM financial stocks until the Ukraine invasion.

However, we mentioned after the start of the war in the end of February that the momentum on cyclical stocks was clearly unsustainable as the economic outlook was set to worsen considerably. The chart below shows that even though selling pressure on LT government bonds remain elevated (i.e. LT bond yields continue to surge), EM financials have been underperforming the market in recent weeks.

Source: Bloomberg/MNI

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

EGB OPTIONS: Bund upside structures

May-16 08:41

- RXM2 158.00c, bought for 3 in 2k

- RXM2 154.5/156.00cs 1x1.5, bought for 11 in 1k

- RXM2 153.5/154.00cs, bought for 22 in 1.9k

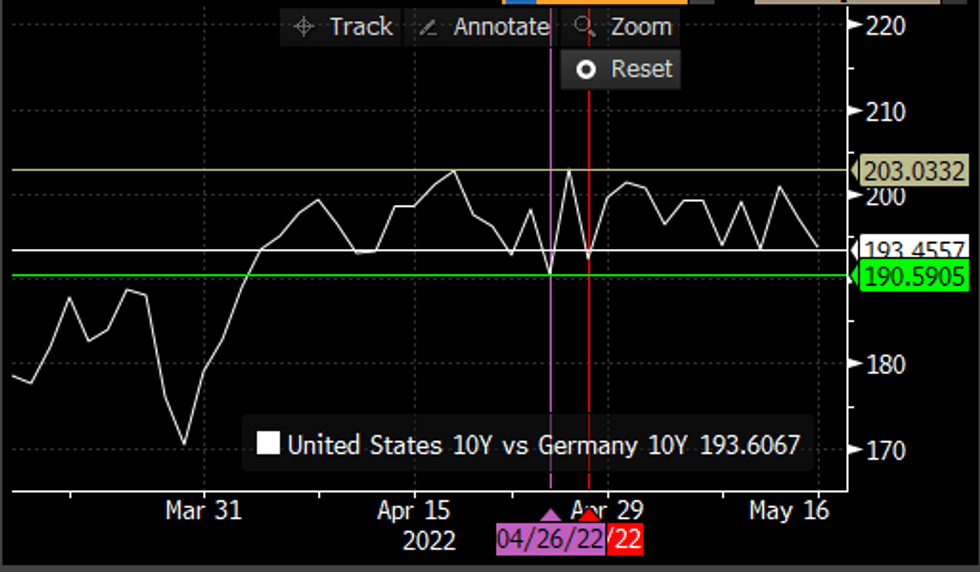

BONDS: US vs Germany

May-16 08:33

- Further small tightening in the Tnote/Bund spread, this was led by some of the sell off in Europe, after Villeroy's comment on the EUR.

- Bund is fairly illiquid so far today, and the US/Germany 10yr spread test initial support at 193.45, this is the May's low and tightest level since late April.

- Better support is seen at the 26th April low, 190.59.

Chart source: MNI/Bloomberg

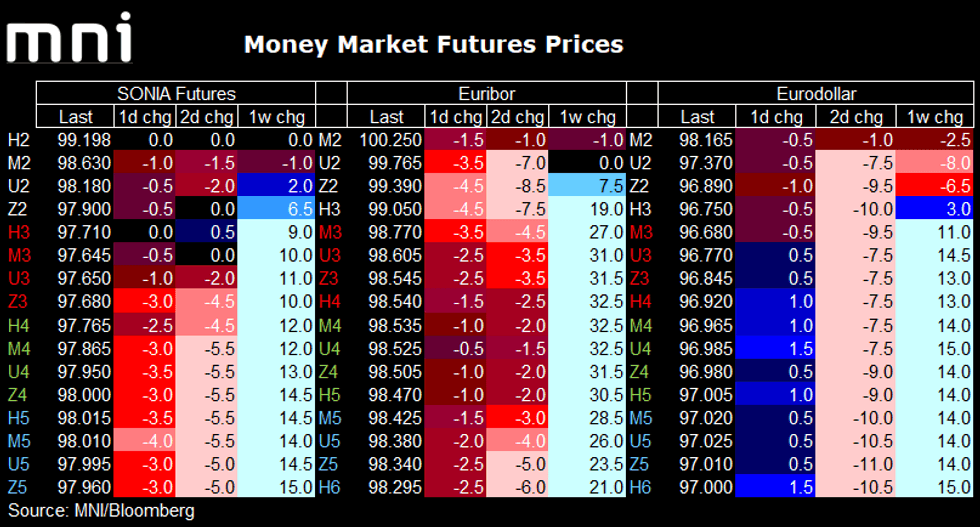

STIR FUTURES: Euribor moving lower this morning

May-16 08:18

- As core fixed income has seen a move lower over the last hour or so, the biggest moves in the STIR space have been in Euribor Whites which are down up to 4.5 ticks - effectively pricing in a more aggressive near-term ECB hiking cycle.

- Markets now price in around 22bp (cumulatively) for a July ECB hike, up from 21bp on Friday, 53bp is priced by September (from just below 51bp on Friday) and 92bp is priced by year-end (up from 85bp on Friday).

- Moves in SONIA futures have been more focused on the Greens / Blues. Markets continue to price in 28bp for June, 57bp by August and 108bp by year-end (from 110bp on Friday).

- The Eurodollar futures strip is generally within 0.5-1.0 ticks of Friday's close. Markets price 53bp for June (from 54bp Friday), 102bp by July, 140bp by September and 190bp by year-end (from 189bp Friday).