STIR FUTURES: What's priced ahead of US CPI?

Jan-12 07:52

It's a big day ahead for STIR markets with the upcoming release of US CPI (a reminder our preview is here).

- Euribor futures saw the biggest moves since the official close with a move around 16:45GMT / 17:45CET yesterday, mainly in the Whites, with a move up to 6 ticks higher. There appear to have been no headlines driving the move at the time. Looking at pricing for the ECB markets are pricing in 48bp for the February meeting, a cumulative 89bp by March, 119bp by May and peaking at 142bp by July. The curve then inverts thereafter.

- We discussed the drivers of the moves in SONIA yesterday here with Reds moving as much as 20 ticks higher. Today we have moved 1-3 ticks higher across Whites / Reds / Greens. In terms of BOE pricing, 44bp is priced for February, a cumulative 74bp by March, 91bp by May and 98bp by June. The curve inverts after fully pricing 100bp in August.

- Eurodollar futures are 1-2 ticks softer through Whites since the close. Markets price 31bp for February, a cumulative 50bp by March and a peak of 62bp by June before inverting, with rates expected to be at lower levels than today by the January 2024 meeting.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

USD: Testing new intraday lows

Dec-13 07:38

- AUD has taken over the NOK as the best performer in G10 against the Greenback.

- The Aussie is up 0.44%, with Equities trending in the green overnight and into the cash Govie open, as China moves away from its zero approach.

- USD makes new lows in early trade, against GBP, EUR, SEK, CAD and CHF.

- AUDUSD sees initial resistance towards the 0.6800 figure.

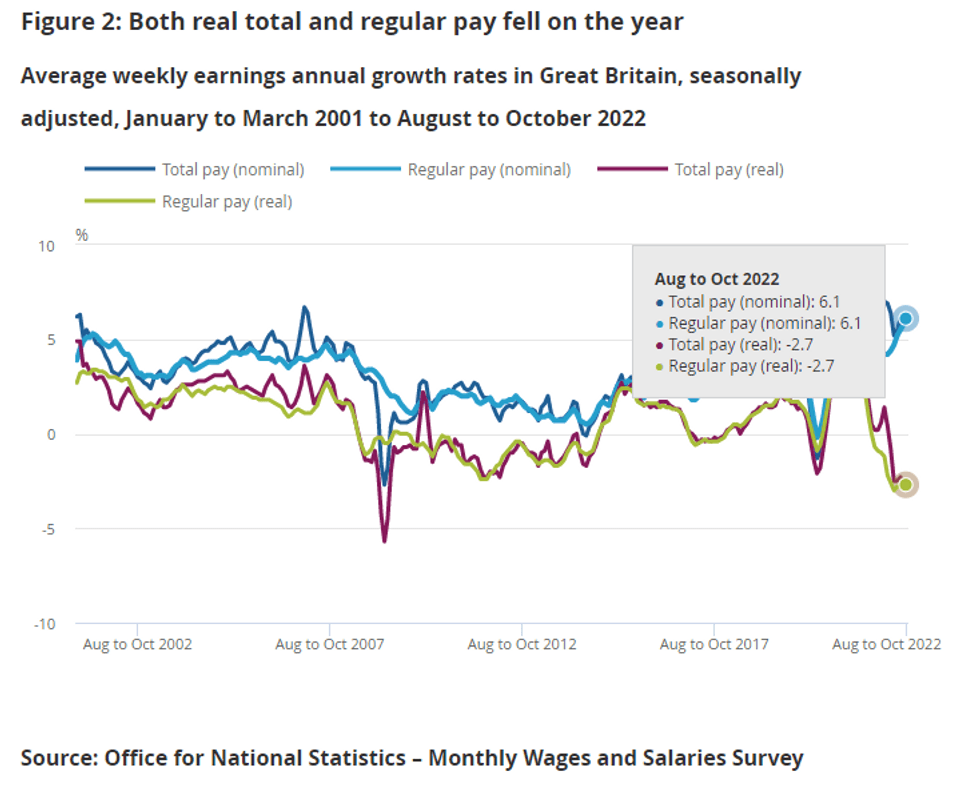

UK DATA: Initial Signs of Declining Inactivity in Latest Data

Dec-13 07:36

The November UK labour report displayed both continued robustness in the labour market (reflected in a jump in payrolls) alongside an increase in jobless claims.

- This reflects more previously inactive participants re-entering the labour force, likely driven by the increased cost of living. This saw the inactivity rate down 0.2pp on the quarter and boosted payrolled employees by 107k (vs 42k expected). A continuation in this trend would imply less pressure on wages.

- Total and regular pay both expanded by +6.1% 3m/yoy, which barring the pandemic was the highest monthly uptick since the series began in 2001. According to an ONS, this translated into real wages falling by -3.9% y/y.

- The unemployment rate ticked up by 0.1pp to 3.7%, yet remains slightly lower than pre-pandemic levels.

- Commenting on today’s labour market figures, ONS head of economic statistics Sam Beckett said "though job vacancies are still at a very high level, they continue to fall and are now lower than they were a year ago."

- Ahead of Thursday's BOE meeting, this data was relatively in line with expectations and focus turns towards tomorrow's November CPI print. Markets are currently pricing 50bp.

EQUITIES: Roll pace update

Dec-13 07:31

Equity rolls should dominate ahead of Friday's quadruple witching.

Roll pace:

- S&P: 53.5%.

- NQA: 46.0%.

- DOW: 48.0%.

- VGA: 29.0% (below pace).

- DAX: 23.0% (below pace).

- FTSE: 36.0%.