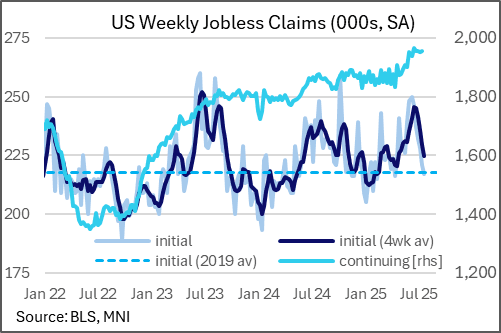

US DATA: Weekly Claims Increasingly Consistent With Low Firing, Low Hiring

Initial jobless claims unexpectedly fell in the Jul 19 week, to a 14-week low 217k (226k expected, 221k prior unrevised). That's the 6th consecutive decline in initial claims since the recent peak of 250k in the first week of June, and brings the 4-week average down to 225k (230k prior), a 13-week low.

- Continuing claims in the Jul 12 week were basically right on consensus however at 1,955k (1,954k expected, 1,951k prior rev 1,956k), keeping the level in its 4-week range of 5k (1,951-1,956k). However that range effectively represents the post-Nov 2021 high and shows no signs of pulling back. The insured unemployment rate remained steady at 1.28% for a 4th week.

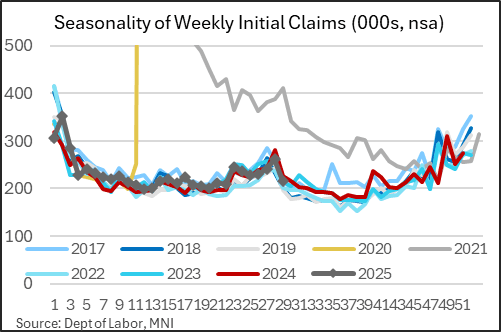

- As such, incoming weekly data continue to portray a low firing, low hiring labor market. Note that the level of seasonally adjusted initial claims is running not just below last year's, but 2023's as well.

- In terms of seasonal adjustment, there basically wasn't any in this week for claims, though the 216k NSA represents a 45k dropoff NSA from the week prior. The same week of the prior year saw a 54k drop in NSA claims to 226k vs a 4k drop in SA claims to 236k.

- NSA continuing claims ticked up 5k, with the level remaining above the 2,000k mark

- On a state-by-state basis, nothing particularly stands out as unusual.

- The report will offer some comfort to the FOMC majority looking for a hold going into next week's meeting, with initial claims if anything suggesting less stress on the labor market as the summer proceeds.

- However Gov Waller could cite the continuing claims data in his case for a cut, noting in his recent speech that "With hiring already low, at a certain point, declining demand would overcome any instinct to hold on to workers, and if that attitude does shift, it implies that a larger and more sudden reduction in payrolls and an increase in the unemployment rate are a risk."

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

MNI: US REDBOOK: JUN STORE SALES +4.8% V YR AGO MO

- MNI: US REDBOOK: JUN STORE SALES +4.8% V YR AGO MO

- US REDBOOK: STORE SALES +4.5% WK ENDED JUN 21 V YR AGO WK

EURIBOR OPTIONS: Call Ladder Buyer

ERU5 98.12/98.1875/98.25c ladder, bought for 1 in 4k.

CANADA DATA: Core CPI Latest Trends

All major core CPI aggregates slowed in May from April, as expected, though sequentially are stronger than they were in March. The trim and median average CPI comes down to 3.00% Y/Y (from a downwardly revised 3.10% in April, was 3.15%) as expected, with 3-/6-month rates also moderating. Still at top end of BOC's target range and keeping Q2 tracking above the BOC's April forecasts.

Core CPI (median & trim av - BoC focus):

% M/M: 0.21 in May'25 after 0.37 in Apr'25

% 3mth ar: 3.0 in May'25 after 3.4 in Apr'25

% 6mth ar: 3.2 in May'25 after 3.3 in Apr'25

% Y/Y: 3.0 in May'25 after 3.1 in Apr'25

CPI xFE (ex food & energy):

% M/M: 0.26 in May'25 after 0.33 in Apr'25

% 3mth ar: 2.4 in May'25 after 3.2 in Apr'25

% 6mth ar: 3.3 in May'25 after 2.9 in Apr'25

CPIX (ex 8 most volatile & indirect taxes):

% M/M: 0.19 in May'25 after 0.44 in Apr'25

% 3mth ar: 1.8 in May'25 after 2.6 in Apr'25

% 6mth ar: 3.1 in May'25 after 3.0 in Apr'25

Source: Bloomberg, MNI