EU AUTOMOTIVE: Week in Review

Jun-06 10:59

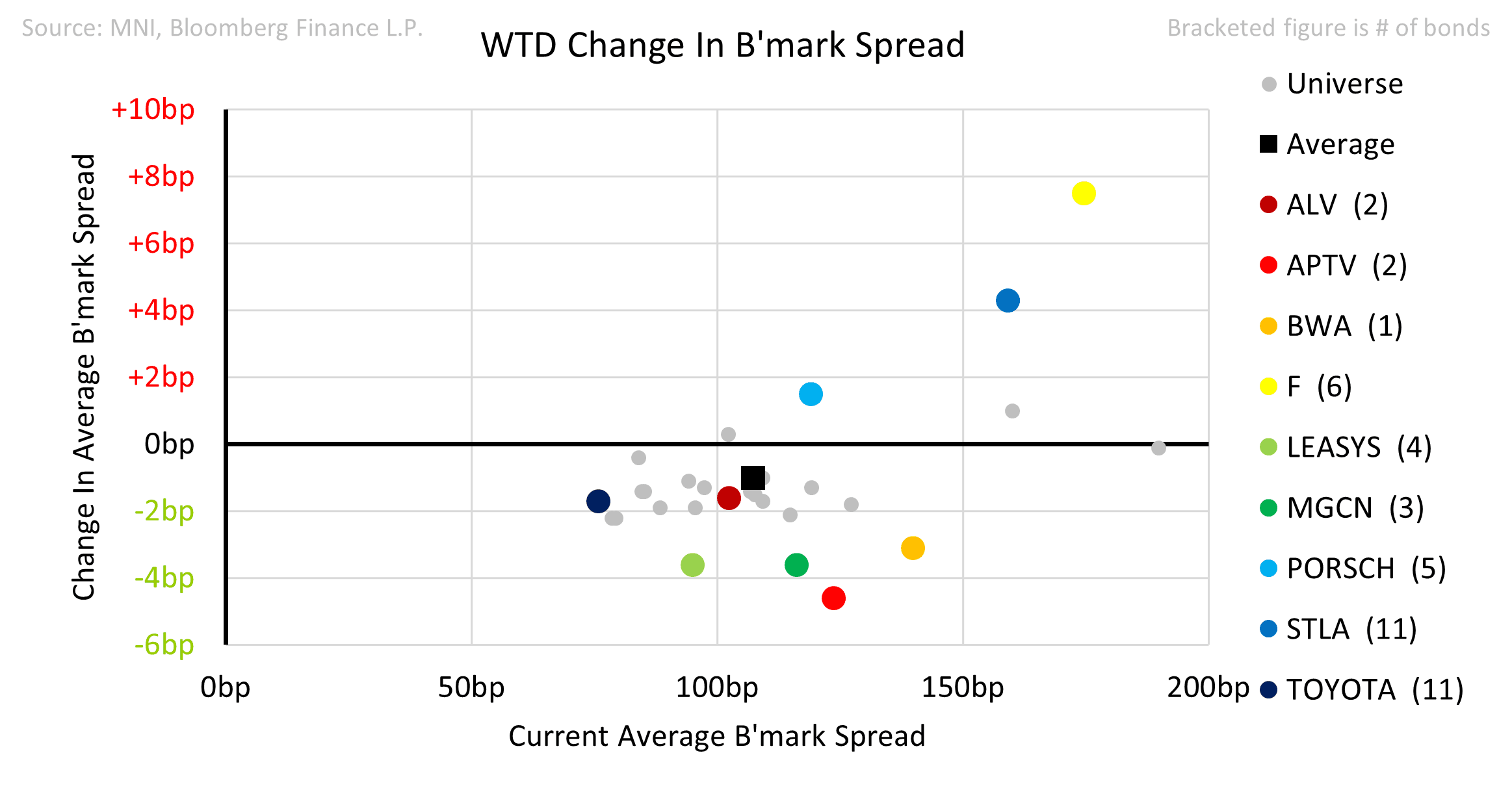

- Spreads lagged marginally at -1bp on the week. High beta F (+8) underperformed, while STLA (+4) lagged on supply.

- Toyota Fudosan tabled a bid for Toyota Industries. The deal would see Toyota Motor draw down some of its cash pile. Moody’s moved outlook from positive to stable as a result.

- Autoliv updated its capital allocation policy at its CMD, with a marginally negative tilt towards shareholder returns.

- Nissan was downgraded to Ba2 by Moody’s with outlook still negative.

- Stellantis printed 6Y and 10Y deals 5/10bp cheap to our FV.

- Volvo Car priced a 4Y green 7bp wide to our FV.

Mercedes-Benz issued a 2Y FRN 10bp inside our FV.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US TSYS: Bear Flatter With A Light Docket Ahead Of The Fed

May-07 10:57

- Treasuries trade bear flatter, with the front end paring some of yesterday’s gains as investors favor pricing a next 25bp cut in July and for now don't want to price in that much more than 75bp of cuts for 2025 as a whole.

- Risk sentiment was supported on early headlines of US-China trade talks scheduled in Switzerland for later this week. This was followed by PBoC easing but US equity futures and Tsy yields are subsequently off session highs.

- Cash yields are 0-3bp higher on the day, with increases led by 3s whilst 20s and 30s lag.

- 5s30s at 88bps is firmly off cycle highs of 100bps from May 1.

- TYM5 trades at 111-08+ (-01+) for close to yesterday’s highs of 111-12+, on another subdued overnight session with volumes at 230k despite no Japan holiday today.

- It hasn’t troubled resistance at 112-01+ (May 2 high) and the contract still trades close to recent lows, undermining the recent bull cycle. Support is seen at 110-27+ (May 6 low).

- Fed: FOMC announcement (1400ET), Chair Powell press conference (1430ET)

- Data: Weekly MBA mortgage data (0700ET), Consumer credit Mar (1500ET)

- Tsy Sec Bessent also sees day two of his Congressional testimony at 1000ET.

OPTIONS: Expiries for May07 NY cut 1000ET (Source DTCC)

May-07 10:56

- EUR/USD: $1.1400(E763mln)

- USD/JPY: Y142.50($804mln), Y143.00($595mln), Y143.20($746mln), Y145.50-55($1.1bln), Y145.85-00($1.6bln)

- EUR/GBP: Gbp0.8555-68(E501mln)

- AUD/USD: $0.6400(A$676mln), $0.6600(A$717mln)

- USD/CAD: C$1.3750-65825mln), C$1.3775-80($961mln)

- USD/CNY: Cny7.2000($500mln)

EQUITIES: Estoxx outright Put buyer

May-07 10:46

SX5E (16th May) 4650p, bought for 2.4 in 5k.