EUROZONE T-BILL ISSUANCE: W/C 1 June

Germany, the Netherlands, France, Spain, Belgium, Finland, the ESM, Greece and the EU are due to sel...

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

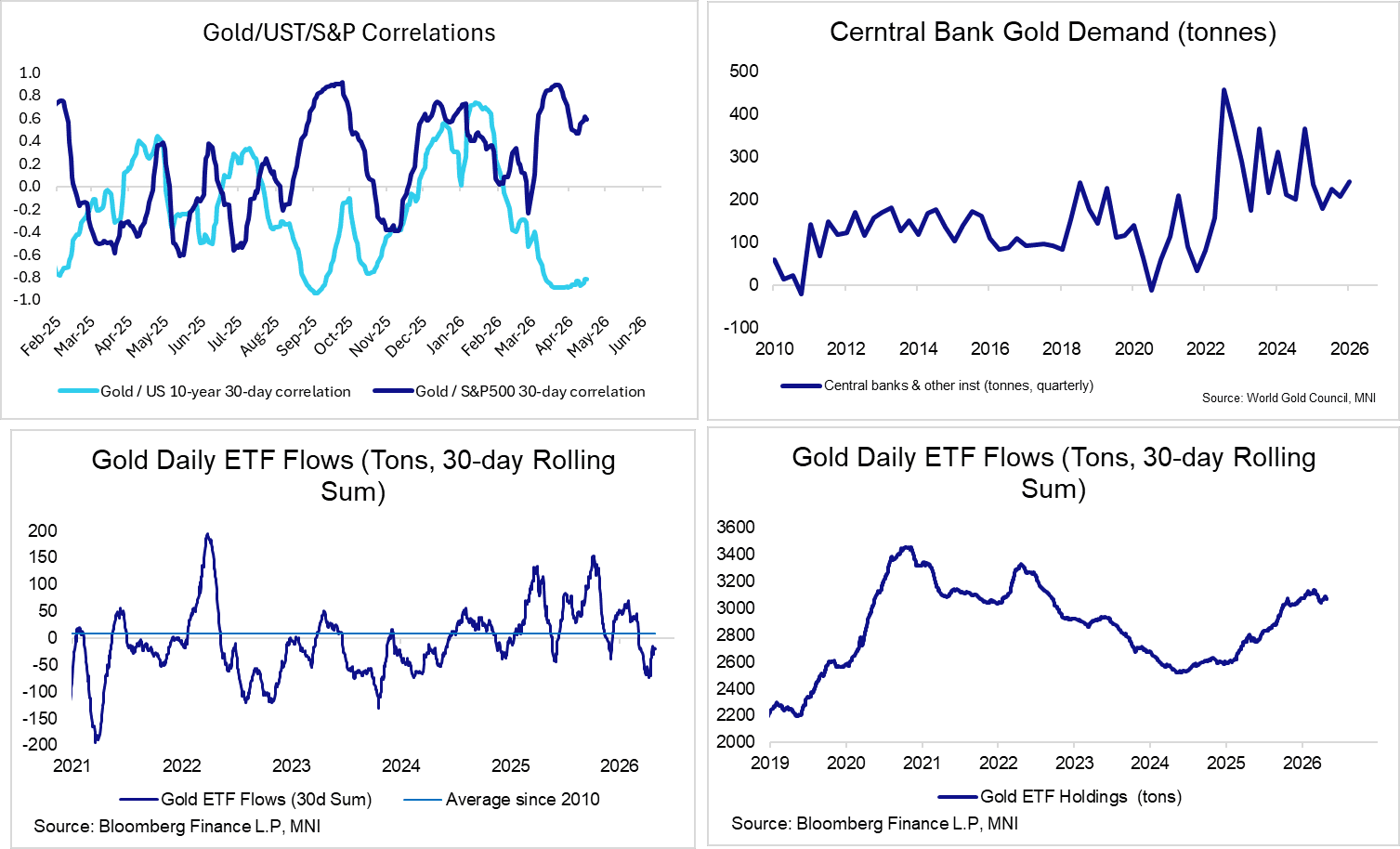

GOLD: Spot Gold Through Support, Dollar and Yields Weighing

Ongoing increases in US yields and the broad dollar index have weighed on spot gold this week. Gold is down 1.25% today at $4,540/oz. Key short term support at $4,554 (April 2 low) has been breached, exposing the March 30 low at $4,420 as the next downside target. Note that the moving average study setup also highlights a bearish theme.

- Since the Iran war started, spot gold has exhibited a strong positive correlation with risk assets (e.g. US equities) and a negative correlation with yields. With recent newsflow certainly not pointing towards an imminent re-opening of the Strait of Hormuz, the near-term risk still appears to be tilted to the downside.

- While the 30-day rolling sum of Western ETF inflows seem to have bottomed out, they remain negative, suggesting retail investors have limited appetite to buy dips in gold in the current environment.

- Despite speculation around the Iran war's impact on global central bank gold demand, the World Gold Council’s latest quarterly report suggested Y/Y demand was still up 3% Y/Y in Q1. However, April data – usually released in early May - may provide a better snapshot of these dynamics.

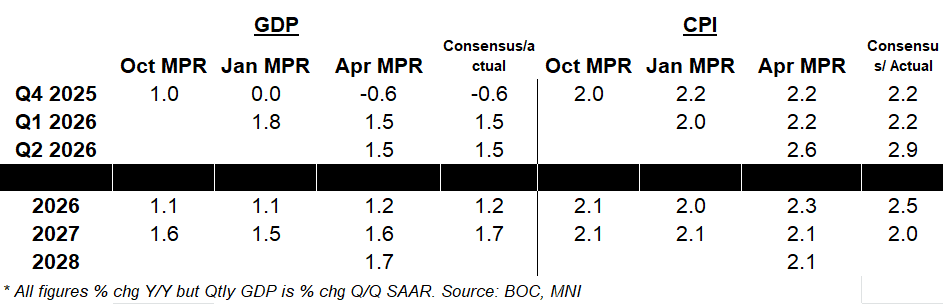

BOC: Neutral Rate Range Remains Steady At 2.25-3.25%

The BOC's policy guidance paragraph also drops references to risks to growth being tilted to the downside with inflation risks to the upside. This in part reflects the incorporation of higher inflation forecasts in the updated Monetary Policy Report vs January's edition - an inflation impulse which the Bank sees being transitory, in line with the message that its baseline is to "look through" the ongoing energy price shock for now.

- "CPI inflation will likely rise further in April to about 3%. Based on the assumption that oil prices will ease" (based on market expectations: "from an average of about US$90 a barrel in the second quarter to about US$75 a barrel by the middle of next year"), "inflation is forecast to come down to the 2% target early next year and remain around 2% over the projection horizon."

- And GDP growth projections are seen a little weaker in the near-term (Q1), though medium-term projections remain fairly robust.

- That growth comes "as growth in exports and business investment gradually resumes" - "While the war in Iran may alter its composition, overall GDP growth is little changed in the updated forecast: Since Canada is a large net exporter of oil, higher oil prices increase national income even as consumers are squeezed by higher gasoline prices."

- And "With GDP growth slightly above potential, the current excess supply in the economy is slowly absorbed." The lower end of the range of potential GDP growth in 2026 has been upped; overall it's 0.8-1.6% vs 0.6-1.6% prior; for 2027 it's been raised to 0.8-1.8% (0.7-1.7% prior) with 2028 at 1.0-2.0%.

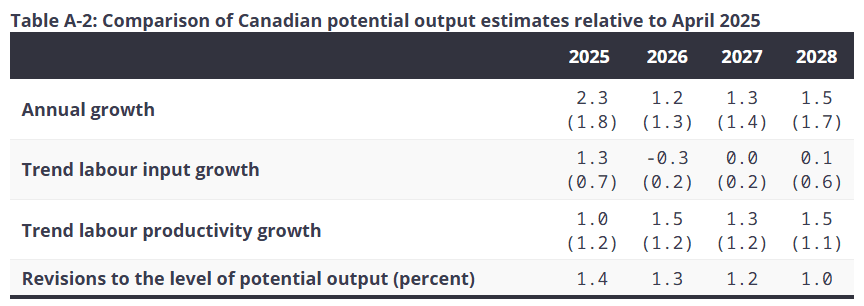

- The MPR notes that "The current level of potential output is above the estimated range from the April 2025 Report. Upward revisions to historical data for Canadian gross domestic product (GDP) and the capital stock, combined with an assumed positive impact from AI, suggest somewhat stronger trend labour productivity." However the estimated rate of potential output growth has been revised lower, with 2026 at 1.2% (1.3% prior), 2027 1.3% (1.4% prior), and 2028 1.5% (1.7% prior), reflecting weaker trend labor input growth (softer population/labour force growth) overall despite upped productivity (despite US tariffs weighing).

- That combination still leaves inflation drifting down to 2.1% by 2027-2028. And the quarterly core (average CPI-trim/median) inflation projections remain tame: 2.1% Y/Y for Q2 vs 2.6% for headline, 2.0% for 2026 Q4 (down from 2.1% in January's projections) and 2.2% in 2027 Q4 (2.1% in January's projections).

- It also leaves the estimated nominal neutral rate at 2.25-3.25% - unchanged from last April's update.

BONDS: Gilt/Bund Spread Signals Limited Uptick In UK Political Risk Premia

The 10-Year gilt/Bund spread trades through the year-to-date closing high (195.03bp) but is only ~2bp wider in the time since the comments from Manchester Mayor Burnham crossed.

- Support in 10-Year futures held to the tick.

- This suggests that the market is not pricing a particularly high likelihood that Burnham returns to parliament and ousts PM Starmer at some point, likely owing to recent experience, whereby his attempt to return was blocked by the Labour NEC.

- Our political risk team has also noted that all 3 of the leading soft-left candidates to replace the PM would benefit from more time elapsing before a leadership contest takes place (see recent bullets for greater details), seemingly lessening the near-term risk to Starmer’s premiership and limiting follow through in the gilt market.