US: VP JD Vance To Deliver Remarks On Economy In Wisconsin Shortly

Feb-26 17:02

US Vice President JD Vance is shortly due to deliver remarks in Plover, Wisconsin, a competitive dis...

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

OPTIONS: Larger FX Option Pipeline

Jan-27 17:00

- EUR/USD: Jan29 $1.1930(E1.0bln); Jan30 $1.1800(E1.7bln), $1.1850(E2.0bln), $1.1900(E4.2bln), $1.1925(E1.1bln); Feb01 $1.2000(E2.1bln)

- USD/JPY: Jan30 Y156.00($1.3bln); Feb02 Y150.95-00($1.3bln)

- AUD/USD: Jan29 $0.6825-40(A$1.2bln)

- USD/CNY: Feb02 Cny6.8700($1.8bln), Cny6.9700($1.1bln)

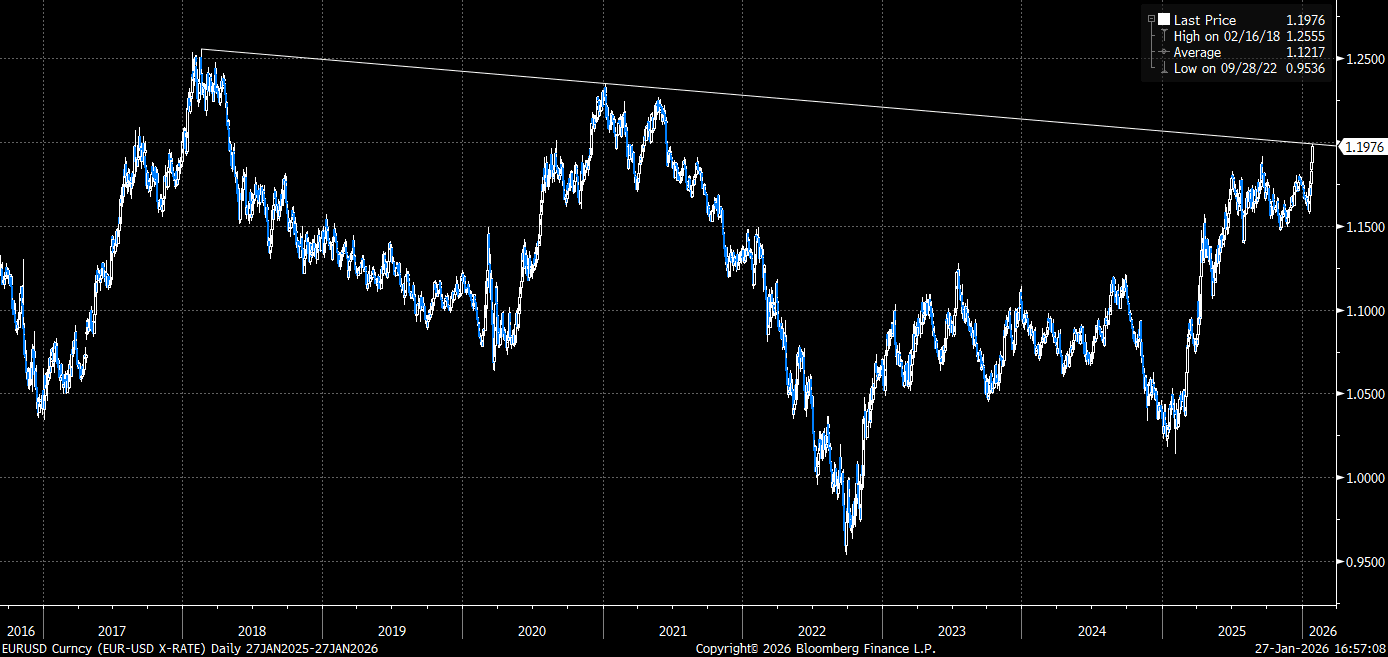

EUR: EURUSD Meets Trendline Resistance Ahead of 1.20 Handle

Jan-27 16:57

- A EURUSD dip down to 1.1850 was well supported earlier today, and the subsequent breach of last year’s highs at 1.1919 has exacerbated topside momentum. with the pair subsequently returning to levels just below 1.19. Broad based dollar weakness continues to provide a key tailwind for the single currency, as the DXY currently tests the 2025 lows as well.

- As well as the psychological 1.2000 mark, it is worth highlighting that EURUSD is currently testing trendline resistance at 1.1988, drawn across the 2018 and 2021 highs which has the potential to stall the price action somewhat. We noted earlier that the bullish trend has stepped into overbought territory, and a pullback would allow this condition to unwind. Support to watch moves up to 1.1716, the 20-day EMA.

- Should the dollar trend continue to gain momentum as we approach tomorrow’s Fed decision, topside levels for EURUSD include 1.2052 and 1.2096, projection levels of the Nov 5 - 13 - 21 price swing.

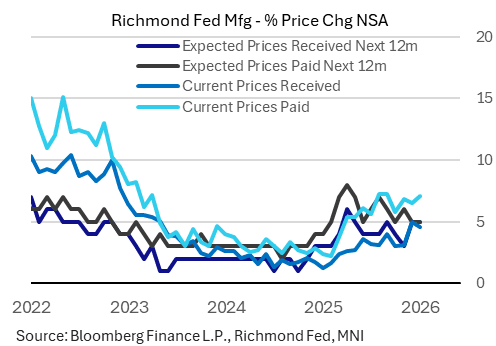

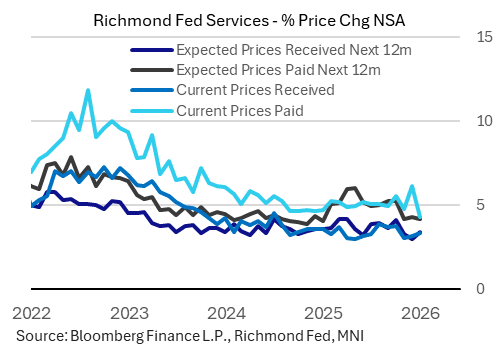

US DATA: Price Dynamics Mixed In Richmond Survey (2/2)

Jan-27 16:51

Services vs Manufacturing price pressures diverged in January, with a pullback in non-manufacturing prices paid reflecting a broader national trend.

- For Manufacturing, Current prices paid rose to 7.1% from 6.5% prior for a 4-month high, with prices received dipping a little to 4.6% from December's 31-month high 5.0%. Expected prices paid/received were both steady at a still-elevated 5.0%. 3 of 5 regional Fed surveys showed higher manufacturing prices paid in January (the exceptions: neighboring NY and Philadelphia).

- Conversely, Services prices paid pulled back sharply, to 4.3% from 6.1% for a 59-month low. And with current prices received ticking up to a 3-month high 3.4% from 3.2% prior, it stands to reason that some of non-manufacturing firms' optimism in the month came from better current margins. (Expected prices were more mixed, with paid basically unchanged at 4.2% though received rose 0.4pp to 3.4%).

- That marked 4 of 5 regional Feds reporting lower non-manufacturing prices paid (Kansas Ctiy the exception).