US: VP Harris' First Press Interview Underway Shortly

Aug-30 00:58

CNN is shortly due to broadcast an interview with Democratic presidential nominee, Kamala Harris. The interview, which was taped earlier today, is the first major unscripted media appearance for Harris since she became the presumptive Democratic nominee five weeks ago. Livestream available on CNN (paywall).

- Harris’ heavily choreographed campaign has been criticised by Republicans for managing her exposure to unscripted moments. There is a widely held Republican assumption that more intensive press scrutiny will expose some of the communication issues that hindered her in 2020, but that assertion is likely overblown considering the assured start to her 2024 campaign.

- Markets will be watching for firm signals on how a Harris administration would diverge from the Biden administration, particularly on key policy items like China tarrifs and strategy for Trump's 2017 tax cuts, which sunset in 2025.

- She is likely to be asked to define ‘price gouging’ and explain how she intends to ban it. She may also be asked to clarify upon whom her proposed tax increases on the wealthy would fall.

- Harris may also be probed on the Biden administration’s response to inflation and ask for clarity on how Harris intends to prevent another inflationary cycle.

- She may also be grilled on her hawkish pivot on border security, from calling Trump’s border wall "un-American" in 2018 to pledging at the DNC to sign into law the bipartisan border security bill that would continue construction of the wall. She may face similar questions about her pivot on opposition to fracking.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

STIR: RBA Dated OIS: 2025 Meetings Lead Softening Ahead Of Q2/June CPI Data

Jul-31 00:52

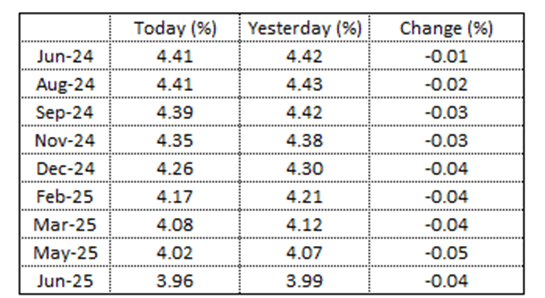

Figure 1: RBA-Dated OIS – Today Vs. Yesterday

Source: MNI – Market News / Bloomberg

JGBS: Cash Curve Bear-Flattens Ahead Of BoJ Decision

Jul-31 00:46

In Tokyo morning trade, JGB futures remain sharply, -59 compared to settlement levels, after extending overnight losses linked to an NHK report that BoJ board members will discuss raising interest rates to around 0.25% from the current range of 0 to 0.1%, citing unidentified people.

- The BoJ will consider raising rates amid a growing view among members that prices are rising in line with forecasts. However, some members are cautious that trends in consumption need to be watched amid falling real wages and will make a final decision after analysing the latest economic data, according to the report.

- The BoJ will also unveil a detailed plan for reducing the pace of its bond purchases over time. (See MNI BoJ Preview here)

- Industrial production declined 3.6% from May led by automakers. That compared with the consensus estimate of a 4.5% drop. Production fell 7.3% from a year ago.

- Retail sales rose a stronger than expected 0.6% m/m in June (+0.2% est) to be +3.7% y/y.

- Cash US tsys are ~1bp cheaper in today’s Asia-Pac session ahead of today’s FOMC decision.

- The cash JGB curve has bear-flattened, with yields 3-7bps higher. The benchmark 10-year yield is 4.8bps higher at 1.052% versus the cycle high of 1.108%.

- The swaps curve has also bear-flattened, with rates flat to 4bps higher. Swap spreads are mostly tighter.

CHINA DATA: PMIs Expected To Ease, But Bond Market Reaction Likely To Be Muted

Jul-31 00:42

- Manufacturing PMIs are Expected To Stay In Contraction for July

- Services PMI are expected to continue to ease as any uplift in spending from the summer holiday period being offset by the continued housing market malaise.

- The manufacturing PMI has oscillated around 50 for several years as the Chinese economy has faced headwinds.

- Last month’s print of 49.5 was the third successive month sub 50 and puts Chinese manufacturing firmly in contraction territory.

- The market survey for July point to further contraction at 49.4.

- Last week’s reduction in policy rates/lending rates points to ongoing concerns about the outlook for the economy, particularly manufacturing.

- The risks to today’s print is to the downside, signaling a weaker manufacturing outcome than anticipated.

- The rally in bond markets in recent weeks could be symptomatic of expectations of material decline in manufacturing in the coming months, suggesting that further policy intervention could be required.

- On the services side, the market survey is for 50.3 outcome (against 50.5 prior) suggesting that services are still expanding albeit modestly