US: Voters Support Deportations But Disapprove Of Hardline Tactics

A new Reuters/Ipsos survey: https://www.reuters.com/world/most-americans-back-trumps-deportation-goa...

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

BOC: January Decision Seen As Marginally Dovish By Canada Bank Analysts

The Bank of Canada's January meeting did little to change analysts' expectations for the path forward. Like MNI, most saw a hint of a dovish tilt vs expectations in the meeting communications but not large enough a deviation from the neutral path to warrant a reassessment. In particular analysts pointed out the lack of mention of fiscal stimulus as a potential upside driver of activity/inflation, as well as the projections showing sustained economic slack.

- Some Canadian institutions' comments, along with their BOC rate views:

- TD (Hold through 2026, hike in 2027): "the policy statement took a more dovish tone by placing more emphasis on heightened uncertainty around the near-term outlook.... There were few attempts to play up domestic strength in the policy statement...The (near) omission of fiscal supports in the January policy statement also struck us as a dovish given the magnitude of new spending in the Federal Budget...Stronger Q3 growth received only a passing mention in the policy statement, while labour market strength was downplayed amid a pullback in BOS hiring intentions. The statement also downplayed the acceleration in headline CPI a consequence of last year's HST pause, while stating that the Bank expects headline to stabilize near 2% going forward... New economic projections in the January Monetary Policy Report added to the dovish tone."

- Desjardins (Hold through 2026. 50bp hikes in 2027): "the federal Budget 2025... was scarcely mentioned in the MPR. The upward adjustment to the government category of real GDP was marginal despite sizeable planned deficits. This likely reflects measures skewed more toward investment than consumption. It could also be because the budget has yet to pass in Parliament ... the Bank left the output gap essentially unchanged from the October MPR, at -1.5% to -0.5%. This contrasts with our estimates and those of many others which show a narrower gap after substantial historical revisions to real GDP, implying less slack in the Canadian economy The Bank looks to have done its best to change as little as possible to support the case for keeping interest rates on hold."

- CIBC (Hold through 2026. 50bp hikes in 2027): "The Bank remains firmly neutral on where things go from here... But if there’s any slight leaning, it’s still toward some concerns on the growth front due to trade uncertainties, and slightly more comfort that underlying inflation is decelerating."

- RBC (Hold through 2026. 100bp hikes in 2027): "Overall, the case for further easing is weak, yet persistent trade uncertainty and gradually moderating inflation are also arguing against a near-term pivot to rate hikes."

- National (50bp hikes in Q4 2026, hold in 2027): "If forced to say whether the statement was hawkish or dovish, we’d lean toward the latter, though. We find the BoC’s growth outlook for 2026 a bit on the soft side and their description of and outlook for inflation is more benign than we anticipated. The BoC leaving its output gap estimate unchanged (rather than estimating less slack) is not totally unexpected, but we thought there was a good chance they’d signal a smaller output gap. You’ll also find an explicit reference to uncertainty and the coming USMCA review in the press release, though this doesn’t come as a surprise. While our assessment leans a bit dovish, it’s marginal."

- BMO (Hold through 2026): "On balance, there is little to move the needle here for markets. The Bank remains cautious amid heightened uncertainty."

GBPUSD TECHS: Overbought But Uptrend Remains Intact

- RES 4: 1.4021 1.236 proj of the Nov 4 - Jan 6 - Jan 19 price swing

- RES 3: 1.3913 High Sep 14 2021

- RES 2: 1.3889 1.00 proj of the Nov 4 - Jan 6 - Jan 19 price swing

- RES 1: 1.3868 High Jan 27

- PRICE: 1.3778 @ 17:11 GMT Jan 28

- SUP 1: 1.3726 High Sep 17 2025

- SUP 2: 1.3664 Low Jan 27

- SUP 3: 1.3568 High Jan 6

- SUP 4: 1.3513 20-day EMA

A strong uptrend in GBPUSD remains intact and Tuesday’s extension reinforces current conditions. The climb signals scope for a move towards 1.3889 next, a Fibonacci projection. Note that the trend is in an extreme overbought position and this highlights the near-term risk of a pullback that would unwind the overbought reading. Firm support to watch is at the 20-day EMA, at 1.3513.

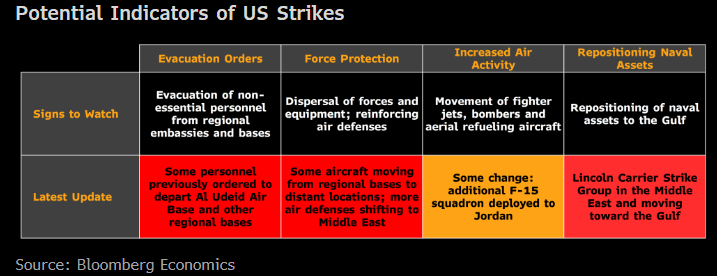

ENERGY SECURITY: US Building Out Options on Iran

The US is building out its options on Iran, with strikes a real possibility, according to Bloomberg.

- A US aircraft carrier strike group has arrived in the Middle East from the Pacific.

- The ships enable operations that don’t rely on politically sensitive regional bases and provide an air-defence umbrella to protect US personnel and partners, Bloomberg added.

- While the US has bases across the region, fears of an Iranian response may push some Gulf states to refuse US access to its airspace in any operations. This has already been confirmed by the UAE.

- An Iranian response would depend on several factors, including its scale.

- More extensive operations are most likely to jeopardise the security of energy infrastructure and the Straits of Hormuz.

- Despite the communications blackout, it appears the scale of violence used to crush protests in Iran likely crossed Trump’s red line.

- Trump has said he wants Iran to come to the negotiating table on a deal to assure Iran can never obtain nuclear weapons, a potential off ramp for Tehran.

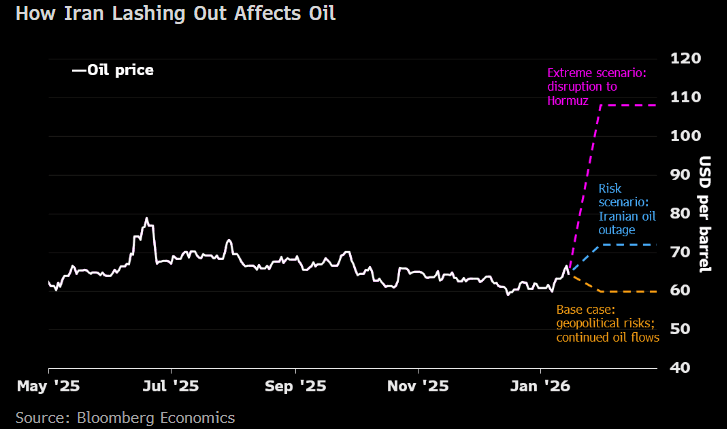

- Bloomberg forecast that in a worst-case scenario where Iran responds by disrupting the Straits of Hormuz, Brent prices could rise to $110/b. An Iranian oil outage without wider regional disruption could drive prices to around $75/b.

- Bloomberg’s base case is for continued oil flows but geopolitical risks premiums, keeping Brent around $60/b.