EU AUTOMOTIVE: Volkswagen: 2Q25 Results

(VW; Baa1/BBB+/A-neg)

Tariffs hurt its better margin products, Audi and Porsche, compounding existing margin issues. Credit negative.

- Revenue 2% below BBG consensus, down 3% YoY.

- Adj. EBIT missed by 5%. Margin was 20bp shy at 4.7%, 210bp lower YoY. Progressive and luxury underperformed due to tariffs.

- 1H auto net cash flow deteriorated to -€1.4bn from +€0.4bn with better WC changes offsetting some of the earnings decline while it also made the €0.9bn payment to Rivian. Investments were steady.

- Auto net cash fell to €28.4bn from €33bn following dividend payments.

- US tariff related costs were €1.2bn. Cash impact was €0.7bn for 1H which would be almost entirely in 2Q.

- Guidance has been updated to include tariffs, which were previously excluded. The ranges are based on a 10-27.5% tariff range.

- Adj. EBIT margin was guided to 4-5%, ~150bp lower. Consensus had 4.9%.

- Revenue growth was revised to flat from up to +5%. Consensus was flat.

- Auto net cash flow €1-3bn from €2-5bn. Consensus saw €2.8bn.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

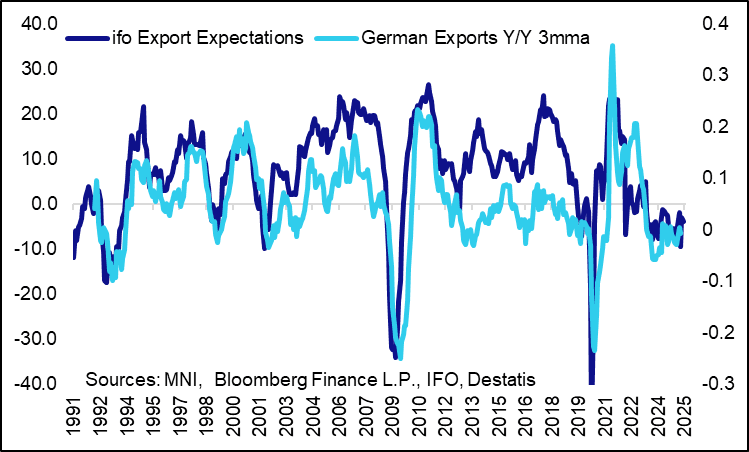

GERMAN DATA: IFO Export Expectations Fall In June

IFO export expectations fell slightly in June to -3.9 points, down from -3.0 points in May. “The tariff threats from the US are still on the table. An agreement between the EU and the US has yet to be reached. This uncertainty is lowering exporters’ expectations”, IFO comments.

- "Beverage manufacturers took a major hit: After a very positive export outlook in the previous months, they do not expect any further impetus from international business in the coming months. Expectations among food manufacturers also plunged – they anticipate a decline in exports."

- The situation is similar in the automotive industry: "There have been no positive export signals for quite some time. International business in mechanical engineering is treading water. The furniture industry and manufacturers of leather goods, on the other hand, are hoping for a growing export business. Electrical equipment manufacturers are also cautiously optimistic."

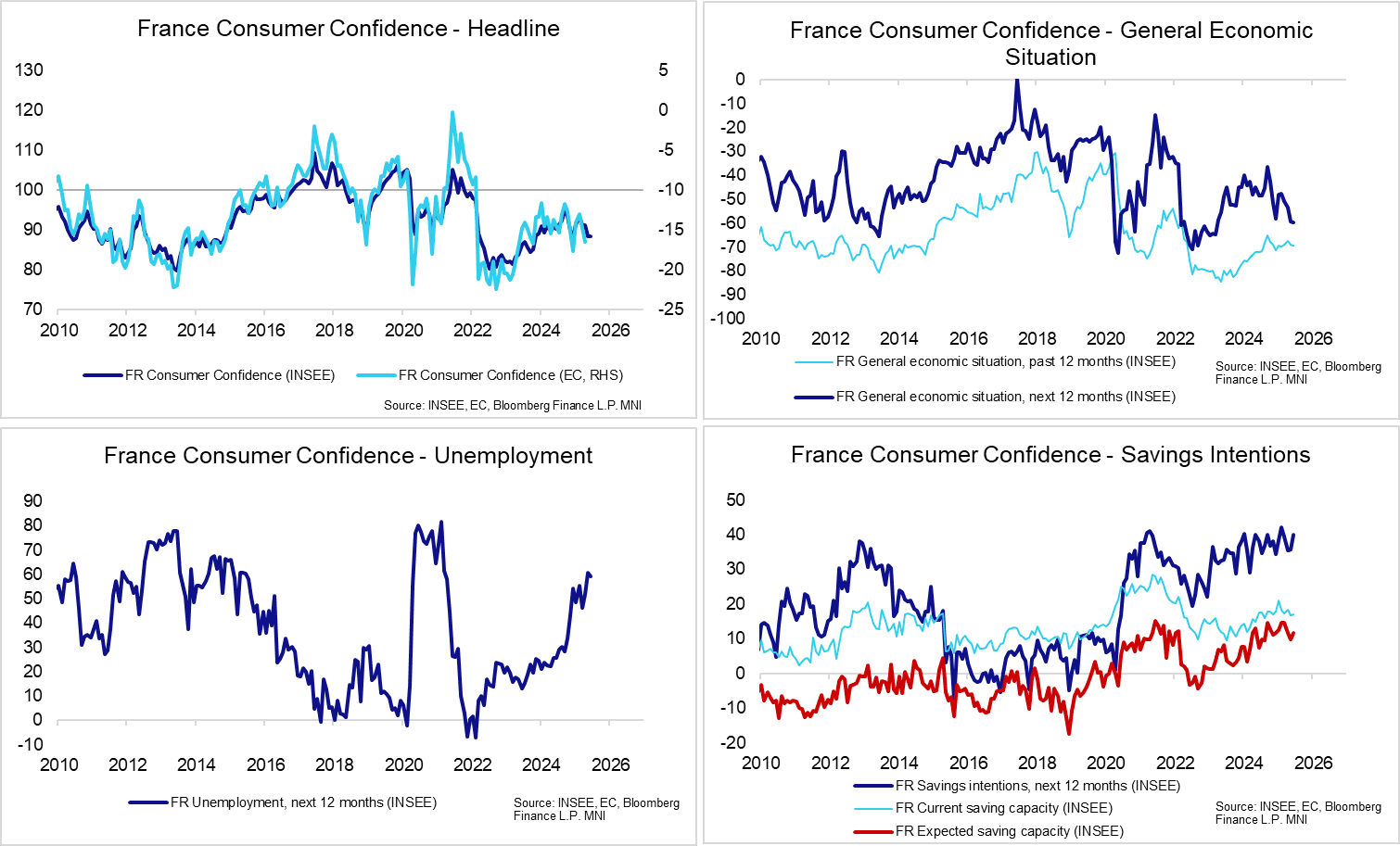

FRANCE DATA: French Consumer Sentiment Weak; Political Uncertainty In Focus

French June consumer confidence was steady at 88.4 (vs 88.3 prior), a touch below the 89.0 rounded consensus. There are likely downside risks to French sentiment ahead though, with political uncertainty set to ratchet higher again in the coming months. After the Bayrou government failed to reach an agreement on pension reforms with social partners yesterday, the Socialist party (supported by others on the left) have proposed a censure motion. While the far-right RN will not support censure at this stage, they have highlighted the 2026 budget as a key event to determine if they will continue to tacitly support (or at least, not bring down) Bayrou.

- In June, consumer’s perception of the general economic outlook worsened on both the backward- and forward-looking measures. Meanwhile, unemployment expectations remained elevated at 59.1 (vs 60.8 in May, 51.9 in April).

- Savings intentions also rose notably to 39.9 (vs 35.8 prior).

- The weak consumer outlook comes with Bayrou expected to propose further fiscal tightening measures in the 2026 budget proposal, provisionally due for next month.

BONDS: Firmer In Recent Trade

Some questions surrounding the bid in core global FI markets. Bund futures still within yesterday's range, while TY futures pierce yesterday's high.

- German curve bull flattens, U.S. paper and gilts see a parallel shift in yields.

- We can’t see a clear headline driver and the move has started to fade.

- News that the Iranian parliament has approved the legislation to suspend cooperation with the UN nuclear watchdog a potential factor, although it was expected, which could explain why the rally has faded a little.

- Also note that EGB spreads to Bunds are tighter, not wider here, suggesting a bit of a pull higher from the periphery.

- OATs manage to overcome the latest round of political uncertainty after the French Socialists filed a no-confidence measure against Prime Minister Bayrou following the collapse of the pension talks. Some suggest the motion is unlikely to pass at this stage, given the lack of support from the far-right. OAT/Bunds ~1.5bp tighter on the day, sub 69bp.

- E-minis consolidate near yesterday’s late NY highs, while the Q3 funding update out of Italy didn’t provide any material surprises.