OIL: Venezuela's PDVSA Resumes Swap With India's Reliance

Dec-19 17:52

Venezuela’s PDVSA and India’s Reliance have resumed an oil swap that was paused because of sanctions Reuters reports after seeing an internal document.

- It follows a U.S. license in July allowing the trade.

- A VLLC loaded with around 1.9 mn bbls of Venezuelan Merey heavy crude departed earlier this month for India's Sikka port.

- A unit of Reliance delivered a 500,000-barrel cargo of heavy naphtha to PDVSA this month in exchange. PDVSA typically uses naphtha to dilute its heavy barrels for export purposes.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

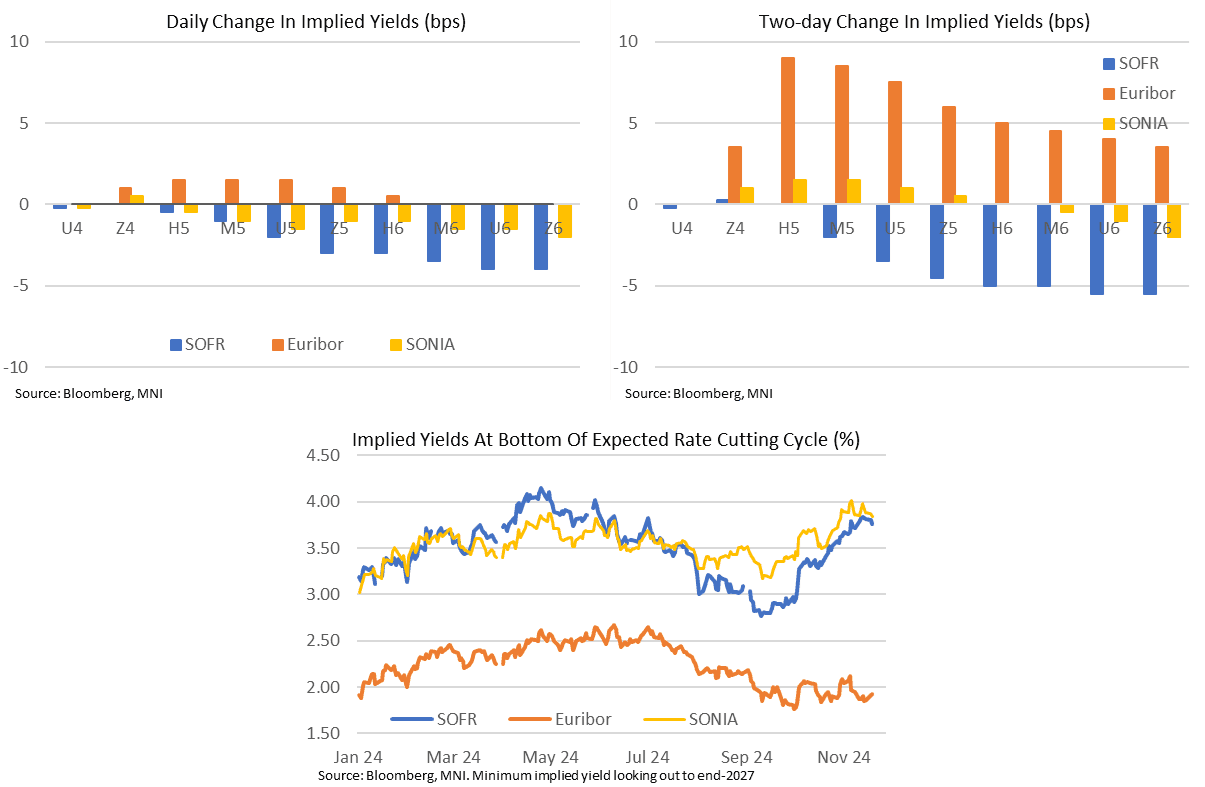

STIR: US Rates See Sizeable Outperformance, UK CPI Eyed Tomorrow

Nov-19 17:48

- US rates have seen reasonable outperformance to European counterparts today (SFRZ5 +0.03 vs ERZ5 -0.015 and SFIZ5 unch), holding onto more of the early geopolitics driven rally after the change in the Russia’s nuclear doctrine.

- US-specific factors have included Lutnick looking set for Commerce Sec. rather than Treasury Sec. (with Lutnick one of the most pro-tariff candidates). A secondary, more at the margin, factor has also been state-level payrolls data showing that whilst there were signs of weather disruption, October’s surprise weakness looks broader-based than just those hurricane- and strike-impacted states.

- The outperformance is clearer over a two-day window (see chart). Yesterday’s hawkish repricing in ECB expectations, with the terminal rate lifting off recent lows vs further rolling over from recent highs for both the Fed and BoE, continues to stand.

- US and UK terminal rate expectations may have rolled over but they remain particularly elevated (3.77% SOFR, 3.84% SONIA, 1.93% EURIBOR). The 3.77% for the US compares with the median FOMC participant eyeing a longer-run target range of 2.75-3% at the Sept SEP but with some notably more hawkish Fedspeak since then.

- On the BoE, today’s TSC showed a further wide array of views on the MPC. We earlier wrote that based on current conditions, February and May cuts seem likely (market is pricing a cumulative 42bp by May). But beyond then it really depends on your view on how inflation / wage growth evolves over the next 6-7 months or so.

- Tomorrow sees UK CPI in focus (MNI Preview: https://mni.marketnews.com/4fyCox8) along with ECB data on Eurozone negotiated wages. US macro is more centred around Fedspeak.

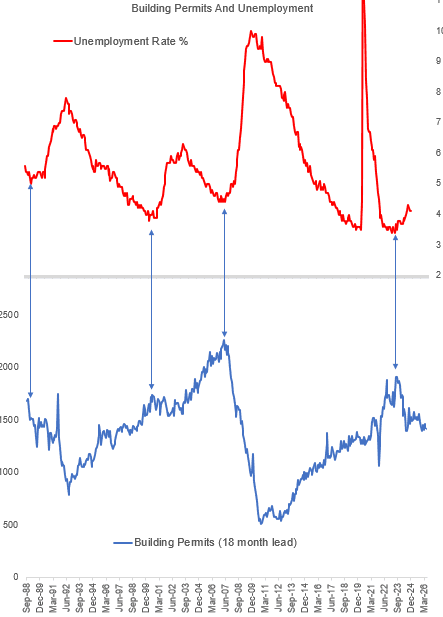

US OUTLOOK/OPINION: US DATA: Housing Data Continue To Point To Higher Unemployment (2/2)

Nov-19 17:30

Residential construction is one of the very few areas in the US economy that is demonstrating consistent weakness, and a rebound does not look likely for the next couple of quarters at least (the Atlanta Fed's GDPNow revision today pointed to a flat contribution to growth in Q4).

- Building permits are considered one of the most reliable leading economic indicators (and are one of the 10 components of the Conference Board's LEI Leading Economic Index), with large turning points in the unemployment rate historically coinciding with peaks in permits - with around an 18-month lag.

- The current episode is shaping up similarly: permits peaked in January 2022 (1915k) and have trended lower ever since. 15 months later, the unemployment rate bottomed out at 3.4% (April 2023).

- It's also similar to previous instances in that single-family permits (historically the bulk of total permits) peaked initially, while multi-family peaked around 6 months later.

- Nonfarm construction payrolls have grown resiliently, but with housing under construction clearly turning lower, this will not last - if history is a guide, the unemployment rate should continue to move higher over the coming months.

- Like the unemployment rate, the movement in permits has been more of a grind than a sudden shift, but the direction of travel remains clear.

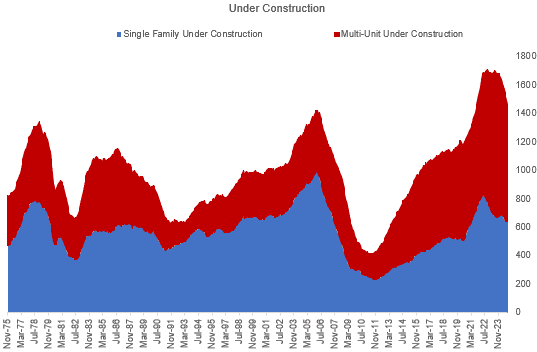

US DATA: Multi-Family Housing Activity Continues To Struggle (1/2)

Nov-19 17:21

New residential construction activity was softer than expected in October, with both housing starts (-3.1%) and permits (-0.6%) falling for the second consecutive month.

- As with other October economic data, here may be a hurricane element involved, as total starts in the South dropped 64k to 666k, offsetting rises in each of the other regions. But the broader trends of weakness remain broadly similar.

- The standout figures in the report were in the multi-family category. Multi-family (ie apartment building) permits saw a 14k decline, to 448k (all expressed in seasonally-adjusted, annualized rates) - only slightly above the 443k low for the year set in May, which was in turn the lowest since the start of the pandemic in 2020. This is a fairly standard pace (pre-pandemic multi-unit permits ranged between 400-500k), but well above the 813k peak seen in early 2023.

- Of greater concern is the sharp decline in multi-family buildings under construction: they fell 29k to 821k, a 31-month low. And since they make up the bulk of ongoing activity, the total units under construction fell by 29k to 1465k - a 36-month low.

- As these figures suggest, single-family activity remains fairly steady, reflecting mortgage market dynamics: higher funding rates make large-scale residential investment more costly vs rental yields, particularly with such large supply coming online, whereas high mortgage rates and low-rate lock-ins by homeowners have reduced existing home sales to multi-decade lows and encouraged homebuilders to cater to single-family building.

- With rates rising and mortgage applications pulling back again after the election, headwinds are likely to persist.