MYR: USD/MYR – Ringgit Weaker as USD Rises Ahead of CPI.

Dec-11 00:37

- USD/MYR is up at 4.4285 in Kuala Lumpur morning; versus yesterday's close of 4.4270.

- The Ringgit is now in touch with the 100-day EMA of 4.4279.

- Bloomberg Asia dollar spot index is up by +0.05% and the Bloomberg Dollar spot index is -0.02% higher.

- USD/MYR one-month implied volatility is up this morning to 5.680%, versus 5.640% yesterday.

- Malaysia's 10-year bond yield is at 3.789%

- Malaysia 5 yr USD CDS at 42bps (yesterday close 43bp, 5-year low 32bp in 2020).

Headlines

- Recent months have seen Malaysia’s economic data moderating, bringing into question the merits of a rate cut next year. Yesterday’s industrial production came in at +2.1%, down from September's result of +2.3%. (source:-Market News).

- October’s Manufacturing Sales rose +3.0% in October, up from +2.9% in September with the value in MYR up by +1.7%, and number of employees rising (source: MNI – Market News)

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

ASIA: BONDS: NZ-US 10Y Differential Bounces Off YTD Low

Nov-11 00:31

NZGBs are 1-2bps richer following a mixed close in US tsys on Friday, with a twist flattening across the yield curves.

- US cash tsys are closed today for the Veterans Day holiday, while Treasury futures (TYZ4) are trading at 110-03+, down 0-05+ from Friday's close.

- The NZ–US yield spread remains steady at +25bps, about 15bps above last week's post-election low of ~+10bps—the narrowest level since mid-2021.

- A simple regression analysis with the 3-month swap rate 1-year forward (1Y3M) spread over the past year suggests that the 10-year yield differential is approximately 7bps wider than its fair value of +18bps.

- The regression error has ranged within +/- 20bps over the past year, indicating some variability in the relationship.

- The 1Y3M differential is a proxy for the expected relative policy path over the next 12 months.

Figure 1: NZ-US 10-Year Yield Differential

Source: MNI – Market News / Bloomberg

AUSTRALIA: 2025 Election Outcome Looking More Uncertain According To Newspoll

Nov-11 00:26

The latest Newspoll from The Australian is showing that the next federal election, which has to be held by 17 May 2025, is looking closer than it has since the last vote in 2022. It still seems a minority Labor government is the most likely outcome but if current trends continue that view becomes more uncertain. The two-party preferred measure is at 51% to 49% in favour of the opposition Coalition.

- The Coalition’s primary vote increased 2pp to 40% in the latest poll taken between November 4 and 8, the first time since the election and above its 35.7% recorded then. According to The Australian, a share at 40% or more makes it “competitive” at the next vote. One Nation appears to be losing support to the Coalition with it polling down 2pp to 5%, consistent with its result at the last election.

- Labor’s primary vote rose 2pp to 33% in the poll, in line with its share in the 2022 election. It seems to have made gains from the Greens and Others who both fell 1pp. The Greens are now down 1pp on its election outcome of 12.2%, while others & independents are 3.5pp lower.

- PM Albanese has been consistently seen as the better PM and while he still is, the gap with opposition leader Dutton has halved from 8pp in October to 4pp this month, narrowest since last election. Albanese was steady on 45% while Dutton rose 4pp to 41%.

- In terms of approval, Albanese’s net rating fell 1pp to -15, his worst since the election, while Dutton’s rose 3pp to -11 to be ahead. In general, respondents are not satisfied with either leader though.

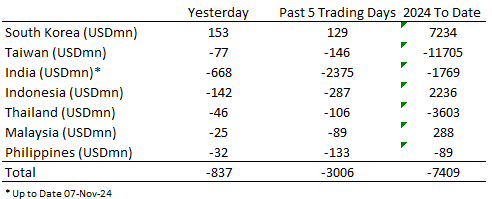

EQUITIES: Asian Equities See Outflow Post US Election

Nov-11 00:12