FOREX: USDJPY Retreat Drives Broader Dollar Weakness

Mar-19 17:15

* Despite recent bouts of risk off and higher energy prices producing supportive price action for ...

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

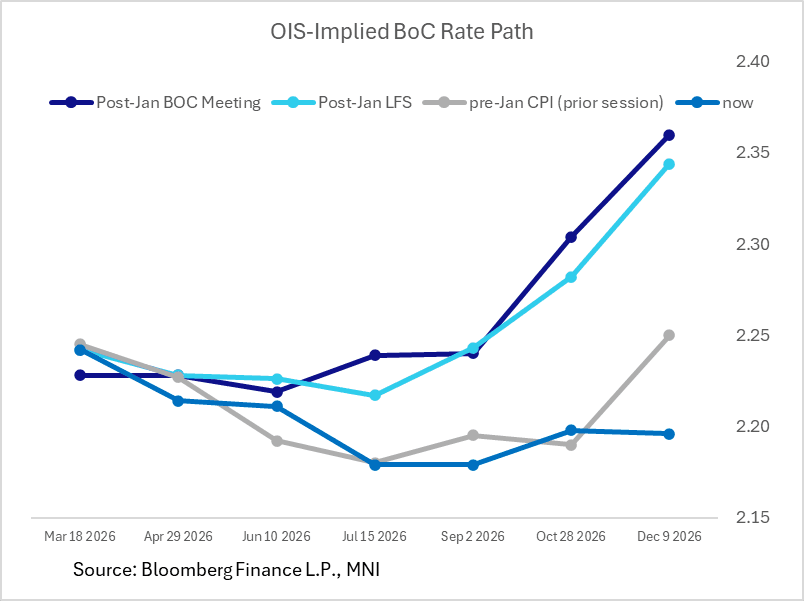

CANADA: Jan CPI Data Seen Giving BOC More Flexibility To Ease

Feb-17 17:14

Analysts see the softer-than-expected January CPI report as giving the BOC more flexibility to ease should policymakers be unexpectedly compelled to shore up economic activity - however the consensus remains firmly for no rate moves in 2026, with 2027 eyed for a modest tightening. Certainly, the OIS-implied rate path has flattened out since the January BOC meeting, currently pricing in slightly more probability of a cut by year-end than a hike, vs a more pronounced tightening bias a couple of weeks ago.

- Scotiabank is the only major Canadian institution that is still looking for BOC rate hikes this year (50bp), and they ask, "why such a mild [market] reaction [to the data]? One reason is that the market has been trained to understand that the BoC is on a prolonged hold as it evaluates upside and downside risks and the combination of cyclical and structural drivers alongside potential changes to fiscal policy and trade policy. That’s a patient debate and reacting in overly hasty fashion could be disastrous....Another reason is that the numbers are of no clear surprise to the BOC. The January MPR had 2.0% y/y for headline CPI and the first month of the quarter was 2.3%. There are a lot of transitory factors from a year-ago that will be working through...There is also the important issue of requiring much more data to avoid being fooled by a potentially temporary soft patch. Something similar was witnessed in early 2024, for instance, after which the m/m SAAR measures of core inflation all took off higher. Short-sighted markets react to short-term data. Central banks should not."

- BMO: " Overall, this is an encouraging result for the Bank of Canada... There's still some wood to chop on core inflation, but the shorter term metrics are moderating noticeably. Still, the Bank has made it abundantly clear that the bar to cut rates again is quite high, and it continues to stress that monetary policy cannot fix supply shocks. Even so, if inflation continues to decelerate, the Bank could be in position to support the economy should growth truly struggle as it undergoes a structural shift."

- Desjardins: "The broad-based slowing in Canadian inflation in January was good news for consumers and policymakers alike. Still, the economy remains in a fragile position, and the forthcoming CUSMA review may mark a pivotal turning point... the Bank signalled in its previous decision that interest rates are already at levels adequate to help the economy navigate through this period of uncertainty. The January CPI data isn’t likely to change that assessment, although a further deterioration in the economic data just might."

- National: "Even assuming an inflation rebound at an annualized rate of 2.0% in the last two months of the quarter, annual core inflation would be one-tenth lower than the 2.5% expected for Q1 by the Bank of Canada in its recently published forecast. Overall, the report ... is not expected to radically change the central bank's view that current interest rates are appropriate to keep inflation close to 2.0%. Due to the current uncertainty, the labour market has a surplus of workers on the sidelines, which is reflected in a significant moderation in wage pressures. The good news from the last two months of CPI data is that, should the economy unexpectedly deteriorate amid heightened trade tensions, the central bank will have the flexibility to provide additional support."

- RBC: "Lower inflation reading leave the BoC with more flexibility to respond to weakening economic conditions with lower interest rates if necessary, although we do not expect as a base-case that additional reductions will be needed. Pockets of price growth are still high (grocery prices in particular.) Year-over-year growth in the trim and median measures have still been above the 2% inflation target for almost five years. And there have been signs that (per worker) labour markets have started to improve at current levels of interest rates."

- TD: "3m core inflation rates had already decelerated sharply in the December CPI report, but we do not think the Bank of Canada needs to lean into this deceleration with core inflation still running near 2.5% y/y (near the Bank's assessment of underlying inflation), and the BoC has previously downplayed 3m core inflation rates as volatile. Today's data will not be enough to pull the Bank of Canada off the sidelines, but it should lower the threshold for the Bank to respond to new growth headwinds should they emerge over 2026."

SOFR OPTIONS: Sep'26 SOFR Midcurve Calls

Feb-17 17:08

- +20,000 0QU6 98.00 calls, 6.0 vs. 96.935/0.13%

FED: US TSY TO SELL $69.000 BLN 17W BILL FEB 18, SETTLE FEB 24

Feb-17 17:05

- US TSY TO SELL $69.000 BLN 17W BILL FEB 18, SETTLE FEB 24