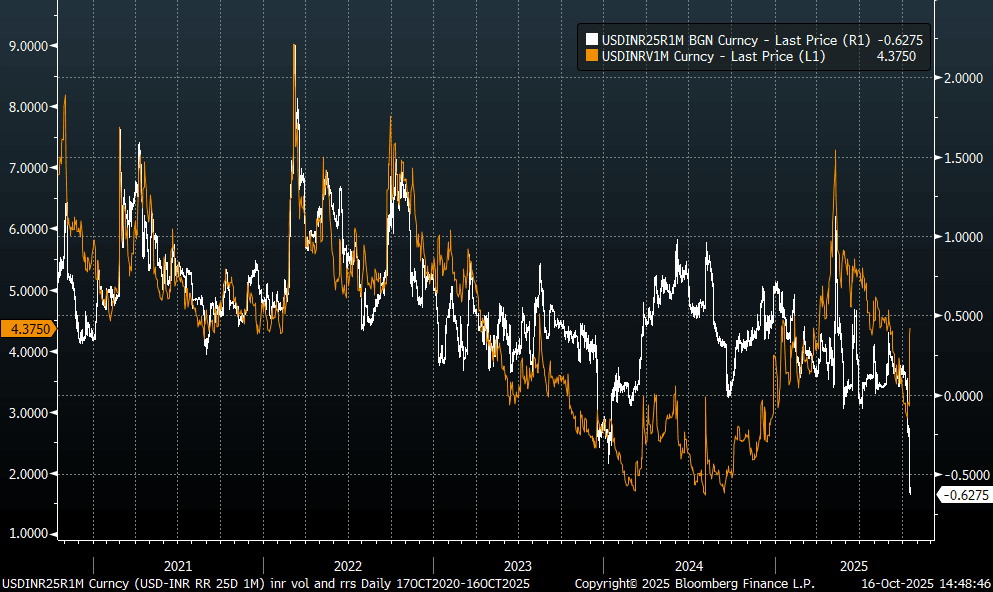

INR: USD/INR Holding Sub 50-day EMA, 1mth Risk Reversal Plunging

USD/INR is largely holding onto its opening losses, with a number of rupee positives in play, while risk reversals are sharply lower. We were last near 87.80/25, down around 0.3% versus end Wednesday levels (earlier lows were at 87.70). We are sub both the 20-day and 50-day (88.03) support points. We haven't been sub the 50 day since July of this year. Further south is the 100-day at 87.39 in terms of potential further downside targets. Recent record highs are around 88.80.

- A number of positives are in play for INR. Earlier remarks from US President Trump that India will stop Russian oil purchases is raising hopes of improved trade relations with the US.

- Indian equities are back close to mid Sep highs, while there is ample scope for further offshore investor inflows. YTD outflows are over $16.5bn.

- RBI intervention risks are also a headwind to USD/INR rebounding. Yesterday's sharp move lower may have caught the market off guard. Indeed, the USD/INR 1 mth risk reversal has plunged into negative territory, see the chart below (where it is overlaid against 1 month implied vol).

Fig 1: USD/INR 1month Risk Reversal Sharply Lower

Source: Bloomberg Finance L.P./MNI

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

FOREX: Asia FX Wrap-BBDXY Breaks Below 1195 In Asia, Can It Extend Ahead Of FOMC

The BBDXY has had a range of 1193.03 - 1195.49 in the Asia-Pac session; it is currently trading around 1193, -0.10%. The USD continues to grind slowly lower, pressing and probing its recent support. A sustained break below 1195 is needed to regain the momentum lower and retest the year's lows towards 1180 where demand should return initially. A break sub 1180 would be extremely bearish, should the USD start another leg lower it would have big implications for FX and potentially see a lot of the recent ranges in G10 broken. The USD is trying to break its recent support ahead of the FOMC with the market pricing in a dovish outcome, there are obvious risks to this buy the rumour strategy. I would prefer to have optionality around FOMC and trade the event than going in naked short with a low bar to disappoint.

- EUR/USD - Asian range 1.1757 - 1.1787, Asia is currently trading 1.1775. The pair consolidated has drifted higher into the FOMC as the USD breaks down. EUR is still within its wider 1.1350-1.1850 range with a bias to the topside.

- GBP/USD - Asian range 1.3598 - 1.3625, Asia is currently dealing around 1.3615. The pair is probing the top-end of its recent 1.3350-1.3650 range, price action suggests it may be looking to break these highs and reassert its momentum higher. A sustained break above 1.3650 will initially target the year's highs just below 1.3800, though here it would open a move back to the 1.4200/1.4300 area.

- USD/CNH - Asian range 7.1119 - 7.1198, the USD/CNY fix printed 7.1134, Asia is currently dealing around 7.1130. Sellers should be around on bounces while price holds below the 7.2200/2500 area and the PBOC manages the fix lower. Above 7.2500 and we could see a test of the USD Shorts.

- Cross asset : SPX +0.10%, Gold $3682, US 10-Year 4.034%, BBDXY 1193, Crude Oil $63.46

- Data/Events : Germany ZEW Survey Expectations, Italy CPI, EZ ZEW Survey Expectations/ Labour Costs/ Industrial Production

Fig 1: BBDXY Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

BONDS: NZGBS: Closed Richer, Monthly CPI Series Supportive

NZGBs closed 3-4bps richer across benchmarks.

- The August monthly CPI series generally showed a slowdown in increases, with food inflation up 0.3% m/m after 0.7% stabilising the annual rate at 5%. The RBNZ forecast Q3 headline inflation at 3.0% y/y in August, the top of its band, with the risk it could temporarily be above. It remains focused on the medium-term outlook, though, as it says, it can do little to impact the near term. However, the stabilisation or moderation in August is likely to be welcomed.

- The monthly price data account for around 46.5% of the quarterly CPI.

- Swap rates closed 4-5bps lower.

- RBNZ dated OIS pricing closed softer across meetings. 22bps of easing is priced for October, with a cumulative 40bps by November 2025.

- Tomorrow, the local calendar will see Q3 current account data and Westpac Q3 consumer confidence.

- The focus of the week will be on Thursday’s Q2 GDP data release. Bloomberg consensus is in line with the RBNZ’s August forecast of -0.3% q/q, bringing the annual rate to flat after declining 0.7% y/y in Q2. 25bp rate cuts are expected at both the October 8 and 26 November meetings.

- On Thursday, the NZ Treasury plans to sell NZ$225mn of the 4.50% May-30 bond and NZ$225mn of the 4.25% May-34 bond.

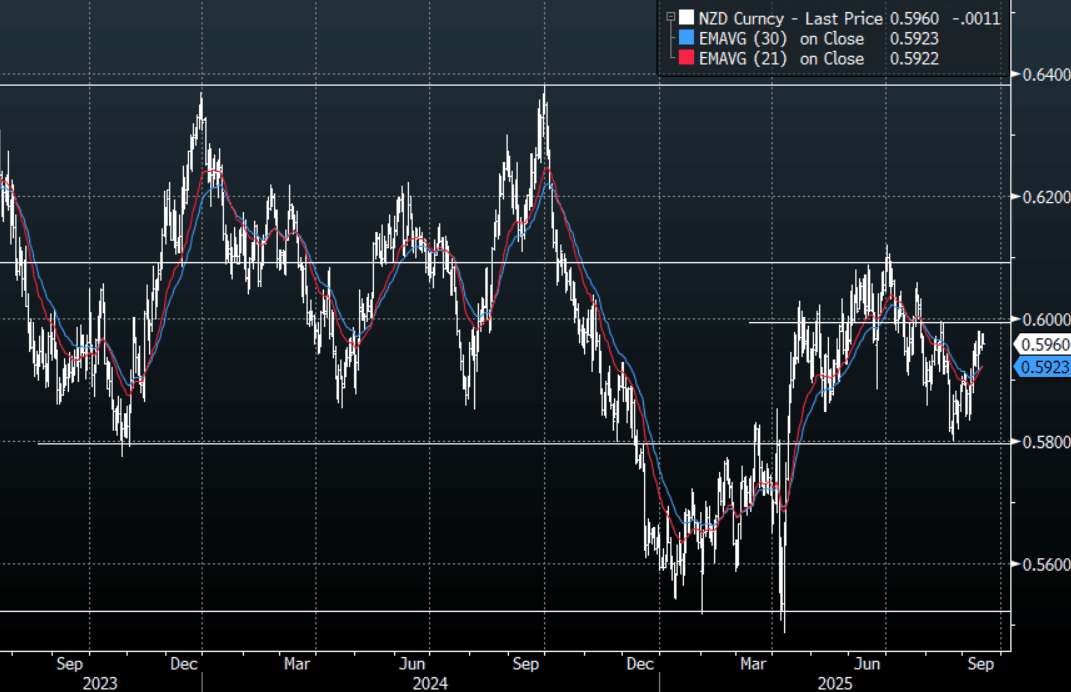

NZD: Asia Wrap - NZD/USD Stalls Towards 0.6000

The NZD/USD had a range of 0.5956 - 0.5975 in the Asia-Pac session, going into the London open trading around 0.5960, -0.18%. US stocks continue to push higher, the risk is the market is getting ahead of itself looking for a potential positive outcome from the FOMC, so the bar for disappointment is being lowered. The USD continues to look vulnerable, which continues to support the NZD. A close back above 0.6000 would negate any semblance of the downward pressure it was exhibiting, but for those that have a bearish view this remains a decent entry point to express that.

- August Price Rises Moderate: The August monthly CPI series generally showed a slowdown in increases with food inflation up 0.3% m/m after 0.7% stabilising the annual rate at 5%. The RBNZ forecast Q3 headline inflation at 3.0% y/y in August, the top of its band, with the risk it could temporarily be above. It remains focussed on the medium-term outlook though as it says it can do little to impact the near term. However, the stabilisation or moderation in August is likely to be welcomed

- Westpac Expects Inflation To Be Below 3% By End 2025. NZ food inflation stabilised at 5.0% y/y in August, its highest since November 2023, while increases for existing rents moderated 0.3pp to 2.1% y/y, the lowest since 2011. The stabilisation or moderation, especially travel-related prices, in August is likely to be welcomed by the RBNZ as it sees a risk that Q3 could print above 3%, the top of the band. Westpac believes that it will be below this level by year end.

- “NZ AUG. GOVT. BONDS HELD BY FOREIGNERS FALL TO 61.5%" - BBG

- Options : Closest significant option expiries for NY cut, based on DTCC data: none. Upcoming Close Strikes : 0.5825(NZD1.01b Sept 17), 0.5900(NZD860m Sept 17), 0.5935(NZD537m Sept 18) - BBG

- AUD/NZD range for the session has been 1.1158 - 1.1191, currently trading 1.1175. The Cross is consolidating above 1.1100, dips back towards 1.1000/1.1050 should be supported now. A break above the multiple highs towards the 1.1200 area is needed to regain the momentum higher.

Fig 1: NZD/USD Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P