LNG: India LNG Consumption Fell 1.4% on Year in September

India’s LNG consumption in September fell 1.4% on the year to 5.642bcm and from 5.754bcm the previous month, according to data from the Petroleum Planning and Analysis Cell cited by Bloomberg.

- Imports were unchanged on the month at 2.819bcm with a rise of 1.2% on the year.

- Net production fell from 2.935bcm to 2.824bcm and down 3.8% on the year.

- India is seeing an uptick in spot LNG demand as prices dip amid buying interest from Gail India this week while GSPC and IOC were both active in the market last week, Bloomberg said.

- Earlier this month, Asian spot LNG prices fell to lowest in over a year, amid weak demand and ample supply, to stimulate some price sensitive demand, Reuters said, although prices have seen a slight recovery this week.

- The 30-day moving average of India’s daily LNG imports have risen towards the high of the year so far at 77.1k tons on Oct. 15 from a low around 55k tons in August, Bloomberg vessel tracking shows.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

EQUITIES: Updated Option Expiry Friday

Looking ahead at Triple Witching Friday, Option expiries in Notional terms:

- SPX: $2.89T vs $2.73T (Yesterday).

- NDX: $114.92bn vs $107.39bn.

- Amazon: $19.00bn vs $17.57bn.

- Apple: $21.67bn vs $20.65bn.

- SX5E: €197.62bn vs €198.35bn.

- SX7E: €18.50bn vs €18.69bn.

- DAX: €39.82bn vs €40.20bn.

- FTSE: £21.46bn vs £21.25bn.

- Lloyds: £5.38bn vs £5.38bn.

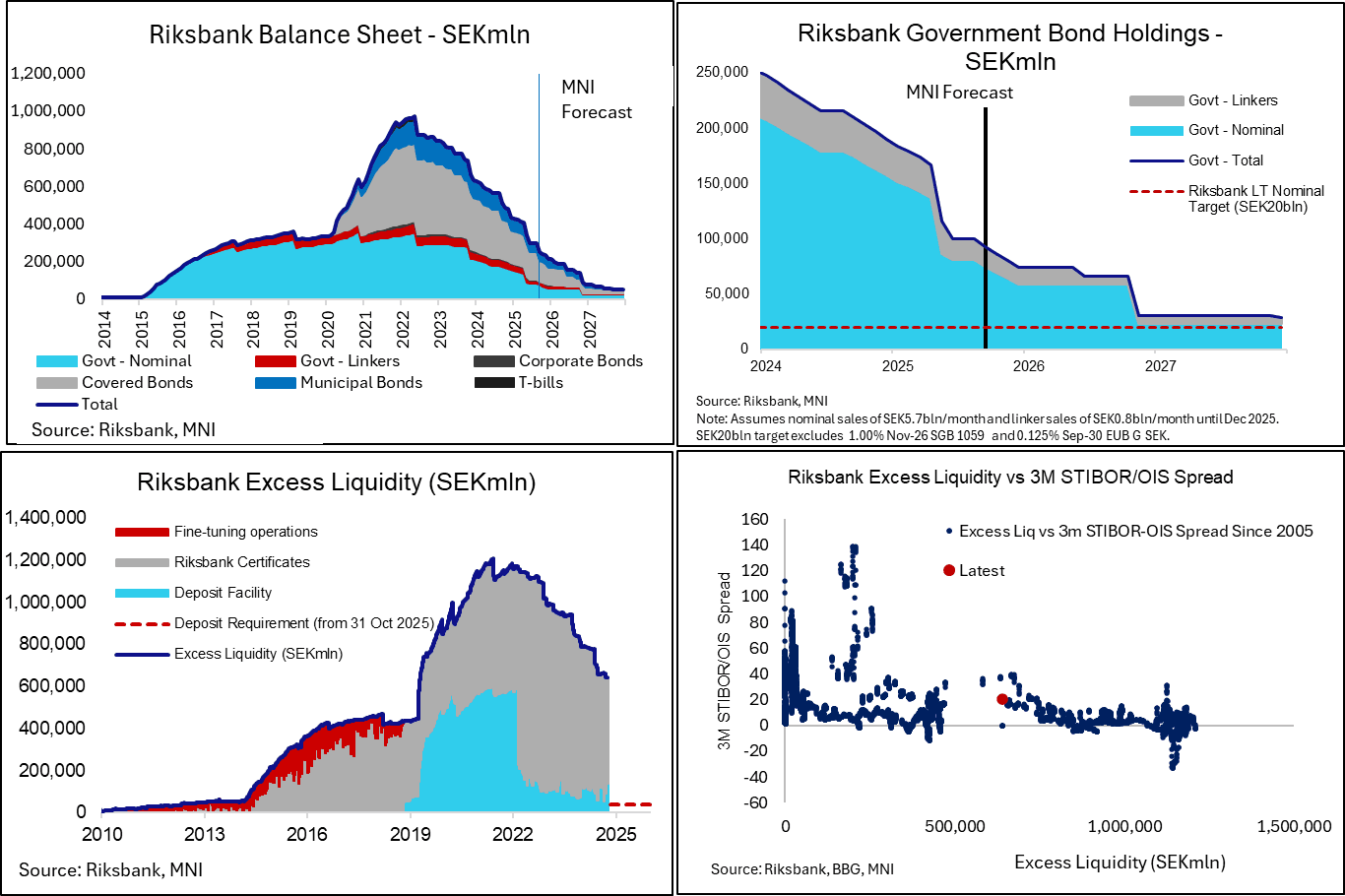

RIKSBANK: Active QT Progressing With Modest Market Impact (2/2)

Riksbank QT has been progressing steadily over the past few years, with the current active sales pace of SEK5.7bln/month of nominal SGBs and SEK0.8bln/month of linkers set to continue until year-end.

- This balance sheet rundown has seen excess liquidity fall from a high of SEK1.2trln SEK in May 2022 to SEK642bln SEK today. According to Governor Thedéen, liquidity is expected to reach SEK400bln by 2030.

- So far, the reduction in excess liquidity has been reflected in a slightly wider 3M STIBOR/OIS spread. The 5d average spread is currently 21bps, up from ~10bps around the start of this year. Those levels are comfortably in the range you’d expect when plotting the spread against excess liquidity going back to 2005.

- Note that as of October 31, the Riksbank will implement a SEK40bln (interest free) deposit requirement. This change is meant to help the Riksbank continue to fund itself, and avoid the need for a capital injection from the Government as was seen in 2024.

- Following the conclusion of active bond sales, the Riksbank’s portfolio of nominal SGBs will be on track to passively reach the long-term target of SEK20bln by late 2026.

- The Riksbank is expected to continue to passively run down its holdings of covered, corporate and municipal bonds during this period.

RIKSBANK: Thedeen Speech Sets The Stage For Rate Tweaks Later This Year (1/2)

An interesting and important speech from Riksbank Governor Thedeen last week set the stage for a number of secondary rate tweaks later this year. While the policy rate is unsurprisingly the primary point of interest for most Riksbank watchers (particularly with next week’s decision a very close call between a hold and a 25bp cut), these proposed tweaks concern the lending rate, deposit rate and supplementary liquidity facility (SLF) rate. The speech is here .

- The deposit rate is currently set 10bps below the policy rate, with the lending rate set 10bps above (creating a 20bp wide corridor within which the monetary stance is managed). The SLF rate, which allows banks to borrow funds using lower grade collateral than required by the lending rate, is set at 75bps above the policy rate.

- With excess liquidity continuing to decrease, the Riksbank wants to promote more active liquidity management in the interbank market without stigmatizing the use of its liquidity facilities when banks require.

- To facilitate such a shift, Thedéen suggested the Riksbank is considering (i) widening the deposit/lending rate corridor (to support more interbank activity) and (ii) lowering the interest rate premium for use of the SLF (to make sure banks are not afraid to access CB liquidity if needed).

- SEB believe the proposed policy changes could “could lead to more short-end volatility, higher demand for short-dated SGBs/T-bills and [a] wider Stibor/OIS spread”.

- These changes certainly won’t be made at the September decision. Thedéen notes that “if we decide to proceed with one or more of these points, we will first send the proposal out for consultation to the relevant market participants”. However, we wouldn’t rule out such tweaks at the November or December meetings.