INR: USD/INR Back Under 20-day EMA, Amid Trade Optimism/RBI Intervention

USD/INR sits just up from session lows, last near 88.45. We are sub the 20-day EMA (last around 88.55), but since late May, dips under this zone have ultimately proven to be buying opportunities in the pair. Upside focus remains firmly on recent record highs just above 88.80, but this looks to be a short term resistance area from an RBI intervention stand point. We may see these levels capped until we get greater clarity around any US-India trade deal (particularly in terms of new tariff levels India may face).

- Local equities look poised to push higher, although the NIFTY hasn't been to sustain +26000 levels recently. If we break higher and this induces offshore inflows (which still sit at -$16bn for 2025 to date), this may aid INR sentiment in the near term.

- However, a sustained INR rally may still be difficult to achieve with pull backs likely supported given some risks of pent up USD demand.

Also via BBG: "A matter of concern for the INR is the RBI’s short forward book, which will put pressure on the domestic currency each time the central bank’s forward contracts mature." (quoting onshore analysts in India).

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

UK FISCAL: Weekend headlines focus on energy VAT removal: Costs and CPI impacts

- The main fiscal headlines from the weekend have suggested that VAT may be removed from energy bills (which was in line with rhetoric last week from Reeves). This was "hinted" at by Energy Secretary Milliband when he refused to rule it out in an interview.

- This would cost somewhere in the region of around GBP1.75-2.0bln (although this is dependent upon wholesale prices).

- The energy "price cap" (the default tariff if people do not fix) is currently GBP1,755/year - so removing the 5% VAT would reduce this to GBP1,671 (roughly GBP84/year savings or a little under GBP7/month).

- In terms of an impact on CPI, "electricity, gas and misc energy" has a 3.2642% weighting. So removing VAT from energy bills would reduce CPI by about 0.16ppt.

- There is much more that the government could do on this if it really wanted to. Other policy costs (social and environmental schemes) add GBP217 to the average annual energy bill. As a rule of thumb about 70% of this is on electricity bills (which is cited by some as slowing the incentive to transition from gas to electricity).

- If all of the costs from electricity bills were also passed to general taxation that would cost somewhere in the region of GBP3.5bln (a bit north of GBP5bln if combined with VAT). We think this unlikely but it would reduce energy bills by GBP236/year (close to GBP20 per month for the average household).

- The CPI impact of this would be a little over 0.4ppt.

- However, we think it unlikely that all of these measures would be implemented - and it would probably be more likely either VAT was removed or the policy measures were removed from electricity bills - not both measures due to the high costs involved.

GOLD TECHS: Impulsive Bull Wave Intact

- RES 4: $4443.8 - 3.618 proj of the May 15 - Jun 16 - 30 price swing

- RES 3: $4404.9 - 3.500 proj of the May 15 - Jun 16 - 30 price swing

- RES 2: $4400.0 - Round number resistance

- RES 1: $4379.9 - High Oct 17

- PRICE: $4234.7 @ 07:26 BST Oct 20

- SUP 1: $4140.8 - Low Oct 15

- SUP 2: $3886.3 - 20-day EMA

- SUP 3: $3819.6 - Low Oct 2

- SUP 4: $3759.9 - 50-day EMA

A bull cycle in Gold remains intact and last week’s extension reinforces current conditions. The move higher maintains the price sequence of higher highs and higher lows. Sights are on the $4400.00 handle next, and $4404.9, a Fibonacci projection point. Note that the trend is in overbought territory. A move down - a correction - and would allow the overbought set-up to unwind. Support to watch lies at $3986.3, 20-day EMA.

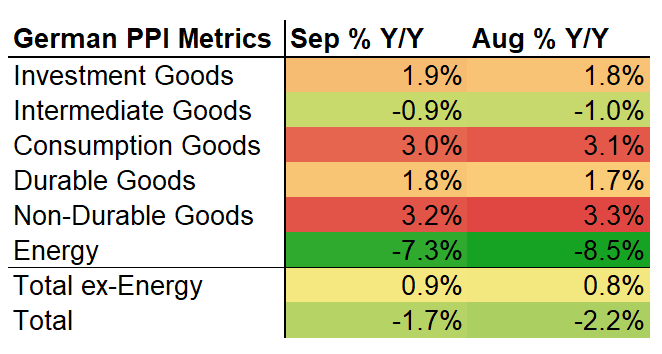

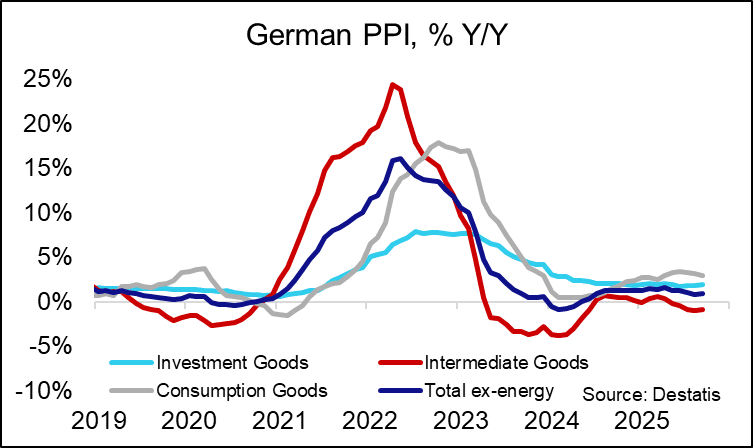

GERMAN DATA: Energy Main Driver In September PPI

German September PPI was slightly softer-than-expected at -1.7% Y/Y, below the -1.5% consensus but above the -2.2% prior reading. The pullback was driven by the energy component, with PPI ex-energy rising marginally to 0.9% Y/Y (0.8% prior according to the Destatis database, note that the press statement mentions an unchanged rate at 0.9%).

- Moves were limited across the main categories, with all of investment, intermediate, consumption, durable and non-durable goods seeing deviations of +-0.1pp maximum vs their August rates.

- EC industry selling price expectations have fallen below their long-term average recently, at 7.0 points in September (7.7 August, 9.4 July, 8.0 l/t average), suggesting limited pipeline pressures ahead.

- Until the impulse from higher fiscal spending starts to feed through, German inflationary pressures appear to be contained by weaker commodity prices, the stronger Euro, continued disinflationary Chinese trade diversion and soft (but improving) domestic demand.