CNH: USD/CNH Up From Fresh Lows, But Still Oversold RSI (14), PMIs Next Week

Spot USD/CNH tracks near 6.8440 in early Friday dealings, comfortably up from late Asia Pac Thursday...

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

BONDS: NZGBS: 10yr Breaks Above 4.60%, As Positive Yield Momentum Persists

NZGB yields are stronger across the benchmarks in the first part of Wednesday trade, up around 3bps. This follows a mixed US Tsy yield backdrop on Tuesday, with front end yields down but back end yields higher, amidst a steepening bias. Focus remains on the upcoming Fed announcement (steady hand expected), while government shutdown risks are also heightened. For NZGBs the 10yr yield has now breached through 4.60%, while the 2yr is around 3.33%.

- For the 10yr NZGB upside focus will rest on consolidating the move into the 4.60-4.80% region. Highs from last year were close to 4.85%, recorded in April. The 2/10s curve is little changed at +128bps, while the NZ-US 10yr spread is holding close to recent highs, around +38.5bps.

- The 2yr swap rate is little changed so far today, around 2.90%, upside focus will rest on the 3.00% level.

- Earlier data showed Dec jobs filled were flat, but this came after a +0.5% gain in Nov, the strongest monthly rise since Apr 2023.

- Tomorrow, we get Dec trade data and Jan ANZ business survey figures.

NEW ZEALAND: Jobs Filled Flat In Dec, After Strong Nov Rise, Y/Y Close To Flat

New Zealand filled jobs for Dec were flat after a revised 0.5%m/m gain for Nov (originally reported as a 0.3% rise). The Nov rise was the strongest outcome since April 2023. This leaves the y/y pace at -0.1%. The data show the improvement in the labour market slowed somewhat in Dec, but this came after a strong Nov outcome. We would expect further general improvements in these trends, given expectations NZ growth improved late 2025 and into early 2026. The outcome is unlikely to shift near term RBNZ thinking.

- Stats NZ notes, in y/y terms, that jobs filled were down 3.1% in construction, and -1.6% in manufacturing. Services related jobs filled was positive in y/y terms.

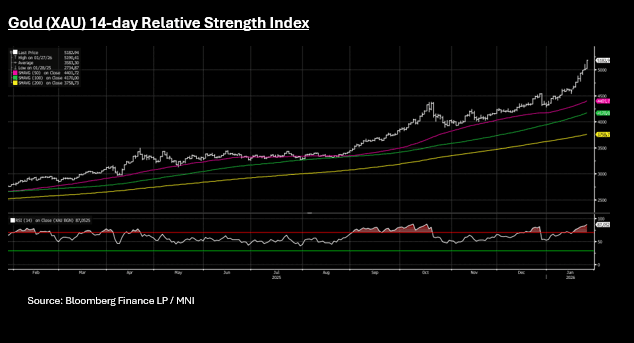

GOLD: Valuations Sidelined as the Bias to Rally Continues

- Gold's relentless rally continued overnight pushing higher, with momentum indicators suggesting extreme valuations.

- Since the beginning of the trading year, gold has rallied 14 out of the 18 trading days pushing bullion deeply into overbought on the 14-day relative strength index.

- Gold rose +3.4% by the close in the US overnight pushing to new all time highs of US$5,186.08 and the biggest one day gain in eight months.

- Early last year, the drivers for gold's ascent seemed clear - the US were ratcheting up their trade rhetoric through the threat of tariffs and gold's safe haven status underpinned demand.

- Successive Central Banks globally have upped their allocation to gold in what some market observers suggest is a 'debasement trade' where investors begin to shy away from treasuries or JGBs and even USD assets in general. Going further, some assess this as equal parts concerns as to the fiscal position in the US and Japan or a re-allocation away from USD assets in a global rebalance.

- Either way, gold's ascent has been astonishing. Gains of 66% in 2025 are being backed up with a year to date tally of almost 20%.

- Finding reasons for gold to fall in the current environment is difficult. Markets can ignore valuations for a long time, until they don't.