CNH: USD/CNH Probing 20-day EMA Resistance As Dollar Supported

Spot USD/CNH probed 20-day EMA resistance as Tuesday trade unfolded. We track near 6.8385 in early W...

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

JGB TECHS: (M6) Fresh Lows

- RES 3: 133.15 - High Feb 24 ‘26

- RES 2: 131.85 - 50-dma (cont)

- RES 1: 131.80 - 38.2% retracement of the Feb - Mar Bear Leg

- PRICE: 130.04 @ 16:53 GMT Mar 27

- SUP 1: 129.82 - Low Mar 26

- SUP 2: 129.57 - 1.0% 10-dma envelope

- SUP 3: 129.06 - 1.500 proj of the Aug 6 ‘24 - Mar 26 - Apr 7 ‘25

JGBs were pressured to fresh lows Friday, breaking below the 130.00 handle in the process. This keeps the price well through the 50-dma and reinforces the negative outlook. Clearance back above this level is needed to highlight a stronger short-term reversal and signal scope for any recovery. Interim supports rest at 129.57 and below at 129.06.

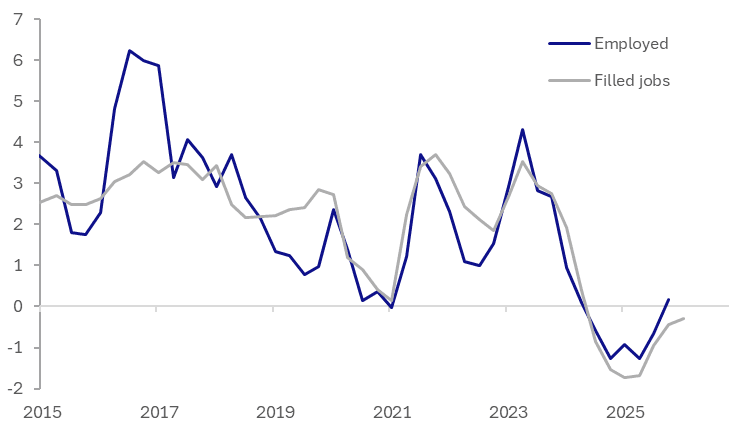

NEW ZEALAND: Labour Market Recovery May Have Stalled

The Q1 filled jobs data to date may be signalling that NZ’s labour market recovery stalled in the quarter, especially given elevated uncertainty from hostilities in the Middle East and its impact on fuel prices in March. February filled jobs rose 0.3% m/m but January was revised down to flat from 0.2%. If March is unchanged then they would be flat in Q1 after rising 0.2% q/q in Q4 but given geopolitical uncertainties and the tendency for this series to be revised lower, the risk is that it contracts over the quarter.

NZ filled jobs vs employment y/y%

Source: MNI - Market News/LSEG/Statistics NZ

*March filled jobs assumed to be flat m/m

- Last week RBNZ Governor Breman said that the MPC isn’t in a hurry to tighten and that currently the fuel price rise is temporary. Ongoing labour market softness adds to the case for ongoing stimulative monetary policy.

- All three major sectors posted gains in jobs in February but primary industries outperformed rising 1.6% m/m while services rose 0.3% (public admin +3.2%) and goods only 0.1% (manufacturing -1.6%). Construction jobs fell 2.1% m/m signalling ongoing weakness in the sector.

- After contracting on an annual basis since June 2024, filled jobs were flat on the year in February. There has been positive 3-month momentum since October but barely so and it slowed last month.

- Another sign of ongoing labour market weakness is the decline in employed youth with 15-19 year olds -4.4% m/m. Job growth was in the over 35s.

AUSSIE BONDS: Front End Futures Outperform On Risk Aversion, 3/10 Curve Steeper

Early Monday trends for bond futures are mixed, the back end softer, with 10yr (XM) down 1bps to 94.86, while 3yr (YM)) is 5bps higher to 95.205. This follows a similar US lead from Friday, where the short end futures rose amid sharp equity risk off, which likely helped reduce the correlation with surging oil prices. Back end US futures were volatile but the 10yr finished up from earlier lows. Early tones today have US futures positive, as US equity futures hold weaker in the first part of trade, while oil gains continue. Focus is likely to be on whether risk off in the equity space can keep US Tsy yields from breaking higher.

- For Aussie 10yr futures, an early dip sub 94.80 once again generated support. This keeps recent ranges intact for now. For the 3yr we are around 95.20, with recent lows at 95.035 intact for now.

- Cash ACGBs are 3-4bps weaker at the front end, the 3yr to 4.75%, while the 10yr is +1bps higher to 5.10%. Recent highs in the 10yr yield rest close to 5.18%.

- The 3/10s curve is slightly steeper at +35bps. Recent lows rest at +23bps.

- The local data calendar is empty today, with tomorrow delivering RBA Minutes from the March policy meeting, while Feb private sector credit is out.