FOREX: USD Consolidates Sharp Move Lower as Tariff Threats Weigh

- Tuesday’s APAC session was highlighted by the significant weakness in the long end of the JGB curve, prompting significant moves for European and US fixed income. The ongoing headwinds for U.S. Treasuries following the latest geopolitical developments have weighed heavily on the US dollar. The sell-America narrative appears very prominent across global markets, assisting precious metals to fresh record highs.

- Price action may have been exacerbated by the return of US markets following yesterday’s MLK holiday, with the USD index comfortably posting its weakest session of the year so far. This has translated to the DXY breaking cleanly back below 99.00, and lows of 98.24 briefly erased the entirety of this year’s advance. This refocuses the market’s attention on a cluster of daily lows just below the 98.00 handle, an area that continued to be well supported in December.

- A headline that said Danish pension operator AkademikerPension was exiting U.S. Treasuries over finance concerns tied to America's budget shortfall prompted the final spike lower for the dollar, before more stable price action then ensued.

- Owing to its weighting in the index, EUR is among the best performers in G10, helping EURUSD to consolidate back above 1.17. A well isolated NZD shrugged off the weakness for risk/equities and extended this week’s rally to around 1.7%, with NZDUSD matching the Dec 24 highs in the process, at 0.5853.

- However, as the potential insulation from European tariff threats and the domestic issues in Japan simmer, it’s the Swiss Franc that tops the G10 leaderboard today. Price action has substantially narrowed the gap to the December lows at 0.7862, and a break of 0.7829 would place the pair at the lowest level since the removal of the CHF peg, eleven years ago.

- All focus now will be on potential comments from President Trump, who is en route to Davos. UK CI headlines the data docket early Wednesday.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

AUSSIE 10-YEAR TECHS: (H6) Marked Lower

- RES 3: 95.982 - 76.4% retracement Sep’24 - Nov’24 downleg

- RES 2: 95.960 - High Apr 7 (cont.)

- RES 1: 95.900 - High Oct 17

- PRICE: 95.160 @ 15:32 GMT Dec 19

- SUP 1: 95.120 - Low Dec 10

- SUP 2: 95.087 - 2.0% Lower Bollinger Band

- SUP 3: 94.276 - 1.0% 10-dma envelope

Aussie 10-yr futures remain well toward the bottom of the recent range, having taken out all major support levels in the process. With 95.275 cleared, prices are pushing to new contract lows, opening vol-band support through 95.087 and into 94.276. Any recoveries need to break back above 95.900 to signal near-term bullish traction.

AUDUSD TECHS: Corrective Phase Still In Play

- RES 4: 0.6759 High Oct 11 ‘24

- RES 3: 0.6723 High Oct 21 ‘24

- RES 2: 0.6707 High Sep 17 and a key resistance

- RES 1: 0.6661/86 High Dec 16 / 10

- PRICE: 0.6608 @ 15:56 GMT Dec 19

- SUP 1: 0.6593 Low Dec 18

- SUP 2: 0.6566 50-day EMA

- SUP 3: 0.6517 Low Nov 27

- SUP 4: 0.6466/21 Low Nov 26 / 21

The trend condition in AUDUSD remains bullish and the latest pullback appears corrective. The move down is allowing a recent overbought condition to unwind. Support at the 20-day EMA, at 0.6598, has been pierced. The 50-day average is at 0.6566. The area between the two averages represents a key short-term support zone. A resumption of gains would refocus attention on key resistance at 0.6707, the Sep 17 high and bull trigger.

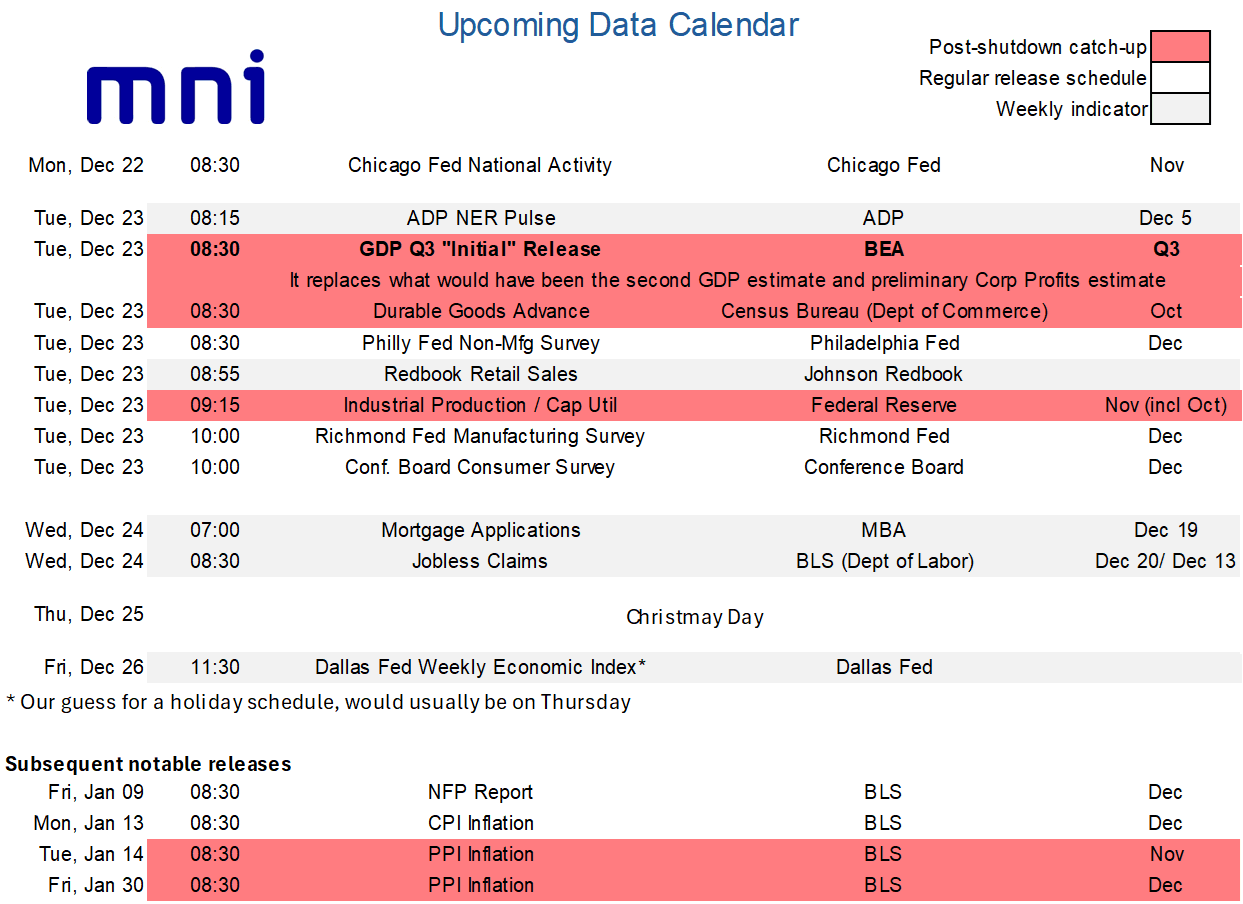

LOOK AHEAD: US Macro Week Ahead: Long-Awaited Q3 GDP Plus Labor Updates

- The week ahead sees a slimmed down data schedule after a particularly busy few weeks, including distorted NFP and CPI reports in the week just gone. There are still some important releases though, with the highlight being the long-awaited “initial” Q3 GDP release on Tuesday.

- This report will replace what would have been the second GDP and the preliminary corporate profits estimates, with the extended tracking window of the Atlanta Fed’s GDPNow pointing to strong real GDP growth of 3.5% annualized after an average 1.6% in 1H25 (-0.65% in Q1 before 3.84% in Q2).

- Expect continued close attention on private demand, best seen by Powell’s preferred PDFP category, which is currently tracking at ~2.4% annualized for similar to the 2.4% averaged in 1H25 (1.9% Q1 before 2.9% in Q2).

- Tuesday also sees updates for the weekly ADP tracker in the four weeks up to Dec 5, getting closer to the reference period for the monthly report, after last week’s further improvement. It’s followed by useful updates for Q4 GDP tracking with durable goods for October and industrial production for both October and November, before the Conference Board consumer survey for December with its closely watched labor differential having stalled at subdued levels but not deteriorated further since September.

- Note as well that Wednesday then sees weekly jobless claims a day early ahead of Christmas Day, with continuing claims capturing the December payrolls reference period. There is currently minimal Fedspeak scheduled and we suspect this will remain the case ahead of Christmas, likely confined to media appearances if any.