FOREX: USD - BBDXY Reverses Back Toward 1205 Breakout Area

The BBDXY has had a range today of 1206.48 - 1208.20 in the Asia-Pac session; it is currently tradin...

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

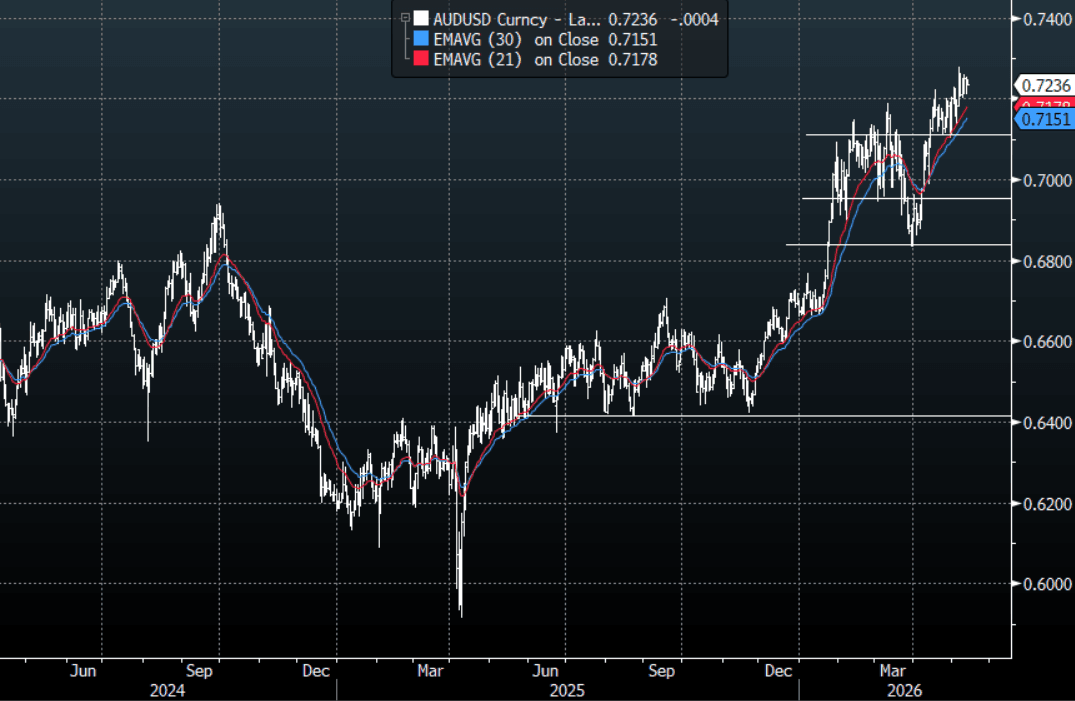

AUD: AUD/USD - Dips Toward 0.7200 Remain Supported As USD Tries To Bounce

The AUD/USD has had a range today of 0.7231-0.7248 in the Asia- Pac session, it is currently trading around 0.7235,-0.05%. The dip toward 0.7200 has proved again to be pretty well supported, this in the face of higher US yields and Oil. The market clearly prefers being short US Dollars and the AUD is a standout vehicle to express that, for the moment the USD continues to lag. Is this a signal of how weak the USD really is or does it play catch up at some point ? On the day, while this 0.7170-0.7200 area continues to provide strong support the AUD bulls will remain in control, looking for the move to build momentum. A move back below here though and the AUD bulls would have their conviction challenged.

- MNI AU - Australia Q1 Wage Growth Contained, Inflation Risk Over Coming Year: Q1 wages growth was in line with Q4 signalling no increase in pay pressures before the onset of the Iran War drove fuel prices sharply higher but the data are dated. The WPI rose 0.8% q/q, as expected, to be up 3.3% y/y after 0.8% & 3.4% in Q4. The Q2 & Q3 wage data released in August and November respectively are more likely to show any increased wage gains due to higher inflation. The size of the July 1 increase in minimum & some award wages due to be announced in June is also key information.

- “Budget-Driven Flattening to Spur Aussie Bonds’ Outperformance. Australian government bonds are set to benefit from improving fiscal dynamics and a potential reduction in the cash buffer held by the country’s funding arm. That supports the case for further curve flattening and Australian government bond outperformance against US Treasuries.” - BBG

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.7100(AUD1.18b), 0.7200(AUD948m). Upcoming Close Strikes : 0.7200(AUD802m May 14), 0.7320(AUD676m May 18), 0.7350(AUD1.69b May 14) - BBG

- The AUD/USD Average True Range for the last 10 Trading days: 49 Points

Fig 1: AUD/USD spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

CHINA: 10-Yr Yields Buck Global Trends

- Almost in defiance of global trends, CGB yields are lower again Wednesday as China auctions CNY170bn 1-Yr and CNY34b 20-Yr CGBs.

- The 10-Yr yield is down -1.5bps to 1.74%, just above the late April low of 1.728%

- Despite a higher than expected PPI and CPI this week and economic growth showing continued signs of improvement, bond yields have continued to grind lower.

- The 2-Yr is lower by -0.5bps at 1.27% and the 30-Yr flat at 2.27%

- Tomorrow China auctions CNY131bn of 7-Yr and CNY90bn of a 10-Yr

- Bond futures are up across all maturities with the 10-Yr up +.065 to reach 108.80 and push further above all major moving averages.

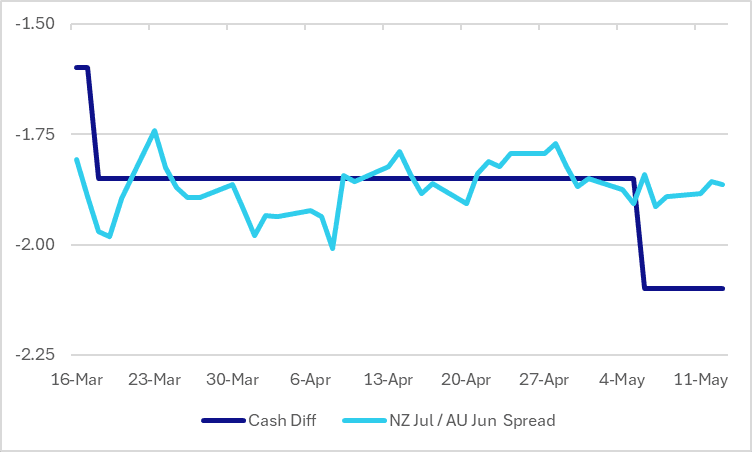

STIR: Front RBNZ Vs RBA OIS Mis-Pricing Remains After NZ Inf Exp Data

There was a jump in NZ inflation expectations for a year out but two years ahead were more contained, which should reassure the RBNZ as it focuses on the medium-term. In its survey of forecasters, economists and industry leaders, 1-year inflation is expected to rise to 3.4% up from Q1's 2.6%, while 2-years ahead is only 0.1pp higher at 2.5% and believed to be within the RBNZ's 1-3% target band on that time horizon. Both the 1- and 2-year measures are the highest since Q4 2023.

- As previously outlined, NZ front-end rates continue look too hawkish relative to the RBNZ’s guidance, especially versus Australia.

- One possible expression of this that we flagged previously had been to fade front-end RBNZ pricing versus the RBA by way of the meeting date contract spread. Receiving Jul-26 RBNZ OIS versus Jun-26 RBA spread had been flagged around levels (-188bps), with scope to gravitate towards -210bps possible if the above relative policy view unfolds.

- As it currently stands, the OIS spread remains around -186bps with the cash rate differential at -210bps.

Figure 1: NZ-AU – Cash Differential Vs. NZ July / AU Jun Contract Spread

Source: Bloomberg Finance LP / MNI