FOREX: USD - BBDXY Extends Move Lower

The BBDXY has had a range today of 1220.29 - 1223.11 in the Asia-Pac session; it is currently trading around 1221, -0.20%. This week the standout has been the huge bounce in global risk together with a repricing of a potential US December rate cut. After initially ignoring this the USD has played catch up to this move. The break back below 1224 overnight reinforces the stalling price action back toward the 1230 resistance again. On the day I suspect rallies back toward 1223-1225 will now be capped as we move back toward the middle or lower end of the 1210-1230 Range, first support seen toward 1218 and then the 1210-1214 area.

- EUR/USD - Asian range 1.1563 - 1.1592, Asia is currently trading 1.1585. The pair broke above the 1.1545-65 area overnight and extended. The focus will now turn to the 1.1650-1.1750 area of resistance. On the day I suspect dips toward 1.1545/65 could now be supported first up.

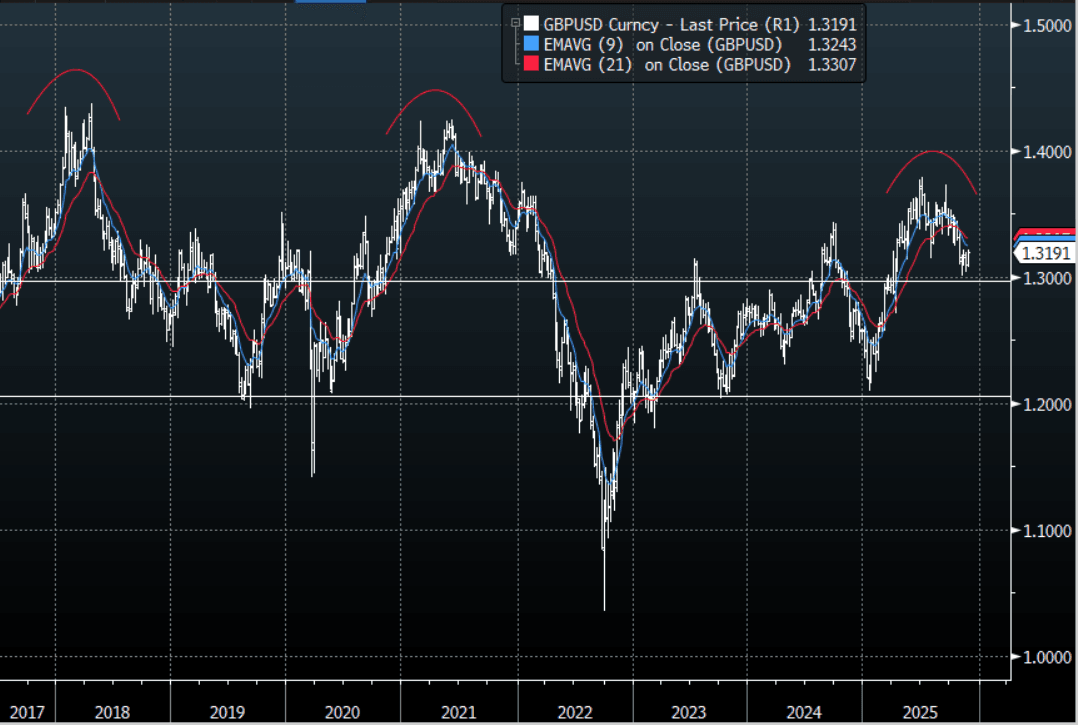

- GBP/USD - Asian range 1.3158 - 1.3197, Asia is currently dealing around 1.3190. The pair broke above the 1.3130-60 area overnight and extended higher. I remain skewed toward shorts but I feel this move does signal the need to be patient as it could first move a little higher. I will be watching the price action back toward 1.3300 for signs of a top should we get back up there. Lots of event risk today with the budget being presented.

- Cross asset : SPX +0.25%, Gold $4160, US 10-Year 4.0075%, BBDXY 1226, Crude Oil $58.18

Fig 1: GBP/USD Spot weekly Chart

Source: MNI - Market News/Bloomberg Finance L.P

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

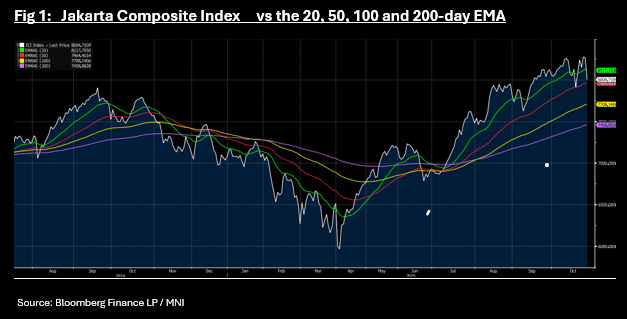

ASIA STOCKS: NIKKEI and KOSPI Hit New Highs as JCI Breaks Below Key Technicals

Japan's NIKKEI traded above 50,000 and the KOSPI through 4,000 as US - China tensions appear to be easing. The discussions between US and China ahead of the leaders meeting this week has seen some positive outcomes with an initial consensus reached on various bilateral issues including agriculture, according to a statement from the Chinese Ministry of Commerce. Chinese officials said the two sides reached a preliminary consensus on further topics including export controls, fentanyl and shipping levies, while US Treasury Secretary Scott Bessent said Trump's threat of 100% tariffs on Chinese goods "is effectively off the table". This comes ahead of the Thursday meeting with US President Trump and China President Xi in South Korea, on the sidelines of APEC summit. The weekend talks are expected to pave the way for a deal/agreement at the Thursday meeting between the two leaders and Trump expressed confidence in such an outcome. Tech stocks like Samsung in Korea surged by almost 2.9% and Taiwan's TSMC +2.7% whilst some regional defense and ship builders saw gains.

- The NIKKEI hit 2025 lows in April of 31,136 as the trade war kicked off in earnest, yet since then has rallied over 60% to 50,340.

- The KOSPI over that same period is up 75% with the added kicker of tax reform on dividends.

- China's major bourses are up only modestly today with the Hang Seng +1.05%, CSI 300 +1.05%, Shanghai Comp +1.1% and Shenzhen +0.95%. The major China bourses have appeared less correlated to tariff headlines of late as the ongoing surge in new retail equity accounts underpins strong fundamental demand for stocks, amidst growing belief in the economy.

- The outlier today is the Jakarta Composite which is down -3.2% for its biggest one day fall since early September, breaking below the 20-day EMA of 8,117 and below 8,000. At 7,993 is is near to the 50-day EMA of 7,963 which it last traded below in July.

- The NIFTY 50 is up +0.55% in morning trade hitting a new all time high of 25,935.

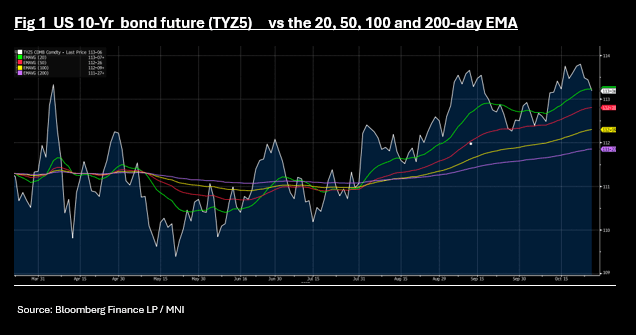

US TSYS: 10-Yr Bond Future Breaks Below Key Technical

The morning's sell off moderated into the afternoon, but the damage was done with bond futures all lower. TYZ5 is down -08 at 113-05+, breaking below the 20-day EMA of 113-07+

Cash bonds remain weak with yields across the curve 2-3bps higher.

- The US 2-Yr is at 3.51% (+2.5bps today)

- The US 5-Yr is at 3.63% (+3bps today)

- The 10-Yr is at 4.03% (+3bps today)

- The 30-Yr is at 4.62% (+3bps) today.

Tonight sees multiple bill issuance, 2-Yr notes, 5-Yr notes as the key auctions for markets.

Key focus for data tonight is Durable Goods, Dallas Fed Mfg, and Capital Goods orders.

JGBS: Risk On Pauses Long End Yield Slide, 30yr JGB Yield Around 100-day EMA

JGB futures are holding negative, but downside sub 136.00 has been limited so far. We were last 135.96, -.18 versus settlement levels. We are still above key support levels (135.61 from Oct 8). Near term focus will be on global bond futures weakness, as markets digest positive weekend news around de-escalating US-China trade tensions. US 10yr futures are down 8 ticks to 113-06, sub its 20-day EMA support point.

- JGB yields are a touch higher, led by the belly of the curve. 5-10yr tenors up a 1bps or more. The 10yr outright yield was last near 1.67%. 20-40yr tenors are close to flat, but the recent downtrend has stalled today. The 30yr yield holding at 3.07%, which is around the 100-day EMA support point. The 2/30s JGB curve is steady at +213bps.

- We had the PPI services earlier, which ticked up to 3.0% y/y, from 2.7% prior, implying some headline CPI upside risks. Still, while some hawkish BoJ board members feel the price target has been achieved, this doesn't appear to be a core board viewpoint yet. The meeting outcome is due Thursday, with no change expected and focus on hike risks for Dec or Q1 next year.

- The local data calendar is empty tomorrow, with debt supply not returning until Friday when a 2y sale is due.