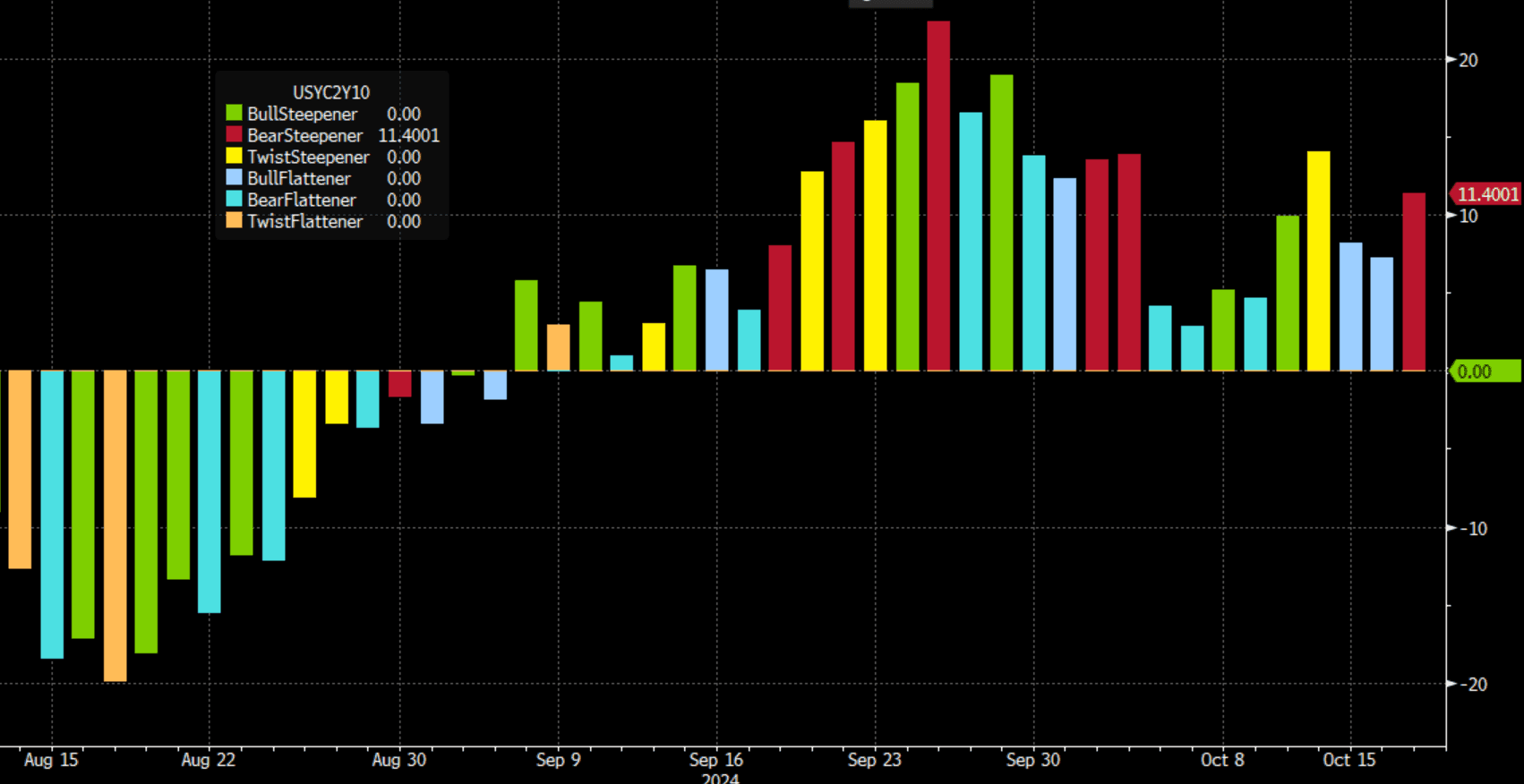

US TSYS: First Daily Bear Steepening Since Nonfarm Payrolls, More To Come?

Thursday's Treasury curve bear steepening (2s10s +4.2bp) on the back of strong retail sales data is set to be the first such move since October 3. That was the day before a strong September employment report began casting serious doubt over the narrative that the Fed's easing cycle could continue at a 50bp cut pace for another meeting (the curve bear flattened sharply that day). See chart below of the level of 2s10s, with daily moves color coded (Bear Steepener = red, etc).

- At current levels, 2s10s would close the month actually having flattened slightly vs end-September - but the balance of risks appear to lie toward more bear steepening in future. The short end of the curve appears to be anchored by FOMC insistence on dialing back what it considers restrictive policy for fear of further labor market cooling. Even as November and December cuts continue to be debated, the pricing since September payrolls that the Fed will get the Funds rate down to its end-2025 median Dot (3.4%) has been fairly unmoved.

- Recall that markets have moved in the Fed's direction since September's Dot Plot was released, not the other way around, so short-end rates probably aren't far from what the FOMC had in mind at the September meeting despite some economic surprises in the meantime. They don't have much reason to signal to markets they are reconsidering the course ahead, which probably would require much more strong data, especially on the labor market side.

- Meanwhile long end yields have been mainly driven by higher inflation breakevens (up 27bp from the recent Sep 10 low) - but notably 10Y real yields (up 20bp over the same period) are set for their highest close since mid-August and could head higher if the Fed looks to remain higher for longer beyond its move to perceived neutral.

- The November elections could play a catalyst here as well if the results look to usher in an inflationary configuration.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US: Harris To Take Questions At NABJ Event Shortly

Vice President Kamala Harris is shortly due to take questions from three National Association of Black Journalists reporters in a press event hosted by the NABJ in Philadelphia, Pennsylvania. LIVESTREAM

- The event is a rare opportunity for voters to see Harris face unscripted media scrutiny, rather than the carefully choreographed stump events that have made up most of her campaign.

- The event is also an opportunity for Harris to connect with Black voters, a demographic bloc that is crucial to Harris' campaign. Recent polls suggest that while Harris has firmed up support with Black voters since assuming the Democratic nomination, her support remains below the level historically correlated with a Democratic presidential win.

- NBC notes: “Harris is expected to face tough questions about her record as attorney general of California and her vice presidency and on specific details about what her administration would do to benefit Black people.”

- Politico notes: "Younger Black men, in particular, have been straying from the Democratic party. The NAACP released a poll on Friday that found one in four younger Black men are backing her Republican opponent Trump."

FOREX: US Data & Profit Taking Dynamics Support Greenback Pre-FOMC

- Downside momentum for the US dollar lost steam on Tuesday, with the USD index unable to breach the previous lows seen in August. A firmer US advanced retail sales number and stronger-than-expected IP have supported a moderate correction higher for the DXY as we approach the pivotal FOMC decision on Wednesday.

- USDJPY (+0.95%) has had the most notable correction, with an impressive bounce from the 139.58 lows on Monday. Spot resides just below session highs of 142.00 as we approach the APAC crossover and firm resistance is not seen until 143.95, the 20-day EMA.

- GBP is underperforming on the session, declining 0.45% to trade back at 1.3160 against the dollar. We noted yesterday that overall, GBPUSD maintains a firmer tone having recovered from last week’s low around 1.3000. A stronger reversal higher would refocus attention on key short-term resistance ahead of the BOE decision this week. This resides at 1.3266, the Aug 27 high.

- A late dip lower for major equity benchmarks has also weighed on the likes of NZD and the Euro, although most G10 ranges remain relatively contained given the proximity to the Fed decision tomorrow.

- In emerging markets, the Mexican peso is rallying once more, assisted by an impressive 2.5% off the lows in MXNJPY, taking advantage of the higher yields and a calmer political backdrop in comparison to last week.

- UK Inflation data kicks off the docket on Wednesday ahead of Thursday’s BOE decision. However, all the focus will be on the highly anticipated FOMC decision and accompanying press conference.

BONDS: EGBs-GILTS CASH CLOSE: Intraday Reversal Sees Modest Bear Flattening

European curves flattened Tuesday, with relatively pronounced weakness at the short end of curves.

- Futures peaked in early trade, as Federal Reserve 50bp cut pricing ticked higher

- But Bunds and Gilts pulled back sharply after 1300UK as oil and equities picked up, while US retail sales data came in slightly stronger than expected on balance, helping keep pressure on the space.

- The main European data release was German ZEW which surprised to the downside, but it was not a market mover.

- Bunds underperformed Gilts, with both curves flattening on the day on a short-end yield backup as implied 2024 BoE and ECB cuts ticked up 2-3bp from intraday lows.

- Periphery EGB spreads closed basically unchanged, reversing early tightening.

- While the Fed decision after the European cash close takes top billing Wednesday, the early highlight is UK CPI which the BoE will have in hand ahead of its decision release Thursday. An uptick in services prices is expected, though the BoE will likely look through any surprises - MNI's preview is here (PDF).

Closing Yields / 10-Yr Periphery EGB Spreads To Germany

- Germany: The 2-Yr yield is up 4.4bps at 2.227%, 5-Yr is up 3.8bps at 2.033%, 10-Yr is up 2.1bps at 2.143%, and 30-Yr is down 0.2bps at 2.398%.

- UK: The 2-Yr yield is up 3.6bps at 3.824%, 5-Yr is up 2.4bps at 3.638%, 10-Yr is up 0.9bps at 3.768%, and 30-Yr is up 0.3bps at 4.353%.

- Italian BTP spread down 0.1bps at 135.5bps / Spanish up 0.2bps at 79.7bps