FED: US TSY 7Y AUCTION: NON-COMP BIDS $108 MLN FROM $44.000 BLN TOTAL

* US TSY 7Y AUCTION: NON-COMP BIDS $108 MLN FROM $44.000 BLN TOTAL...

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

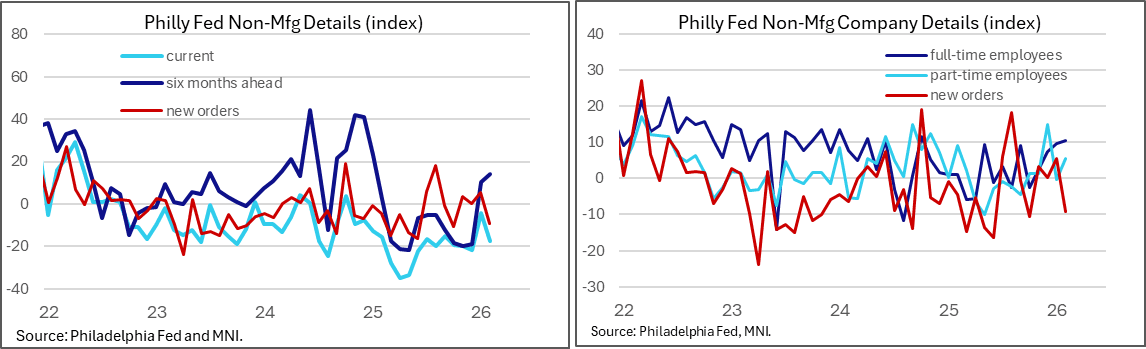

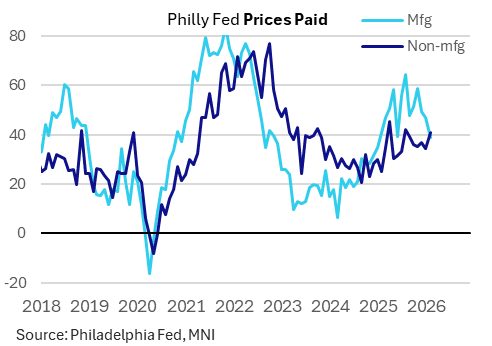

US DATA: Soft Philly Fed Services Activity Comes With Stubborn Price Pressures

The Philadelphia Fed's Nonmanufacturing Business Outlook Survey showed a sharp deterioration in activity in February, with some worrying developments on the inflation front.

- The regional general activity index dropped to -17.3 after a surprisingly high -4.2 in January (which had been a 15-month high). Firm-level activity was also weaker at 5.8 after 16.2.

- New orders fell sharply (-9.3 after 5.5 for the worst reading in 4 months) and sales/revenues dropped 17 points to 8.2, with the key positive development being on the employment front with full-time employees printing a 16-month best 10.6. Additionally, firms expected better activity in six months' time.

- We took particular note in the sharp rise in price gauges, with paid up to 40.7 for a 6-month high after January's 34.5 marked a 6-month low; prices received rose 9 points to 22 for the highest since May 2023.

- This was the first time the non-manufacturing prices paid gauge exceeded that of manufacturing since October 2024, and corresponded with regional Fed services surveys elsewhere which have shown stubborn prices paid in February (largely in contrast to manufacturing counterparts). The pickup in prices received also suggests services firms are feeling a little more confident in their pricing power.

US TSY FUTURES: Midday March'26-June'26 Roll Update: 2Y Near 75% Complete

Midday Tsy quarterly futures roll volumes from March'26 to June'26 outlined below. Heavy volumes this morning sees most between 60%-65% complete (2s lead at 73%) ahead of Friday's "First Notice" date where the June contract takes lead. Current roll details:

- TUH6/TUM6 appr 1,569,500 from -5.62 to -5.0, -5.12 last; 73% complete

- FVH6/FVM6 appr 2,604,000 from -2.0 to -1.5, -1.5 last; 66% complete

- TYH6/TYM6 appr 2,350,400 from 1.5 to 2.0, 2.0 last; 65% complete

- UXYH6/UXYM6 434,800 from 3.25 to 3.5, 3.5 last; 60% complete

- USH6/USM6 appr 356,000 from 13.0 to 13.75, 13.25 last; 59% complete

- WNH6/WNM6 appr 461,800 from 10.0 to 10.75, 10.0 last; 60% complete

- Reminder, Mar'26 futures don't expire until next month: 10s, 30s and Ultras on March 20, while 2s and 5s expire on March 31.

FED: Gov Cook Joins FOMC Debate On Potential NAIRU Issues From AI

Fed Governor Cook was the latest FOMC participant to highlight the potential for AI-related job losses as part of a transitional phase for the labor market, and the dilemma that could pose for Fed policy. She and other officials appear to fear a scenario in which monetary policy would be unable to address structural job losses under AI displacement if there is a rise in the natural rate of unemployment. The tone has been broadly hawkish on this front in the sense that policymakers could be more hesitant to ease policy in the event of a rising unemployment rate, for fear of stoking inflation.

- In a speech Tuesday Cook said “The AI transition I am contemplating could have profound implications for monetary policy. If AI continues to raise productivity, economic growth could remain strong, even as churn in the labor market leads to an increase in unemployment. In a productivity boom such as this, a rise in unemployment may not indicate increased slack. As such, our normal demand-side monetary policy may not be able to ameliorate an AI-caused unemployment spell without also increasing inflationary pressure. This means that monetary policymakers would face tradeoffs between unemployment and inflation. While there is a role for monetary policy, education, workforce, and other policy that is nonmonetary may be better suited to address these challenges in a more targeted way."

- This take on labor market dynamics under AI echoes comments this morning by Atlanta Fed President Bostic, who noted that if AI changes the way businesses employ people throughout the economy, "then all of our benchmarks are going to have to change -- how we think about what a good jobs number is, what unemployment rate that's reasonable should be. They're just going to be different. We will have to recalibrate our thinking about what appropriate policy is because the same number is sending a different signal."

- Earlier this month, Gov Barr also said similar: "If AI causes a large and long-lasting dislocation of workers, permanently reducing demand for many kinds of jobs, it could imply higher rates of unemployment, even when the economy is healthy and operating close to its potential. Monetary policy is able to address cyclical conditions, like a downturn in the business cycle, but it cannot address the structural factors that determine the long-run rates of employment."

- We should also note though that the risks aren't perceived as one-sided; Barr said last year for example "If AI shifts the workforce toward groups that have higher labor force attachment but lower unemployment rates (such as college graduates), the result could be downward pressure on u*."

- Gov Miran - the FOMC's biggest dove, and a proponent of rate cuts in part because higher productivity allows inflation to subside - is less concerned about the potential for AI result in structural job loss, saying last week in an interview with The Peg: "I don’t think that we can conclude that there’s going to be some structural increase in unemployment, that’s a long term increase in unemployment, because that hasn’t really happened for previous technological bouts. Why would we conclude that this, alone, in all of human history, is a technology that we will never recover from economically? That’s a bold claim that I don’t really see a lot of reason for accepting."

- And Gov Waller, also a dove, said Tuesday that he was skeptical that AI would produce widespread job losses.